ByAiden

ByAiden

Medicare Advantage Is Costing Taxpayers $84 Billion a Year More Than Traditional Medicare — While Denying More Care

Share your love

Medicare Advantage is the private insurance alternative to traditional Medicare, now covering 54% of all Medicare beneficiaries — 34.1 million Americans. Private insurers receive a fixed capitated payment from the federal government for each enrollee, adjusted for health risk. In 2025, the Medicare Payment Advisory Commission (MedPAC) estimates Medicare paid MA plans a total of $84 billion more than it would have spent if those same enrollees had remained in traditional Medicare. That’s not a rounding error. That’s the annual price tag of a federal program designed to save money that instead costs more, denies more care, commits more billing fraud per dollar, and is now exiting rural markets after extracting decades of subsidy payments.

Key Takeaways:

- Medicare Advantage now covers 54% of Medicare beneficiaries (34.1 million) in 2025, up from roughly 15% when the 2003 Medicare Modernization Act re-engineered the subsidy structure to favor private insurers.

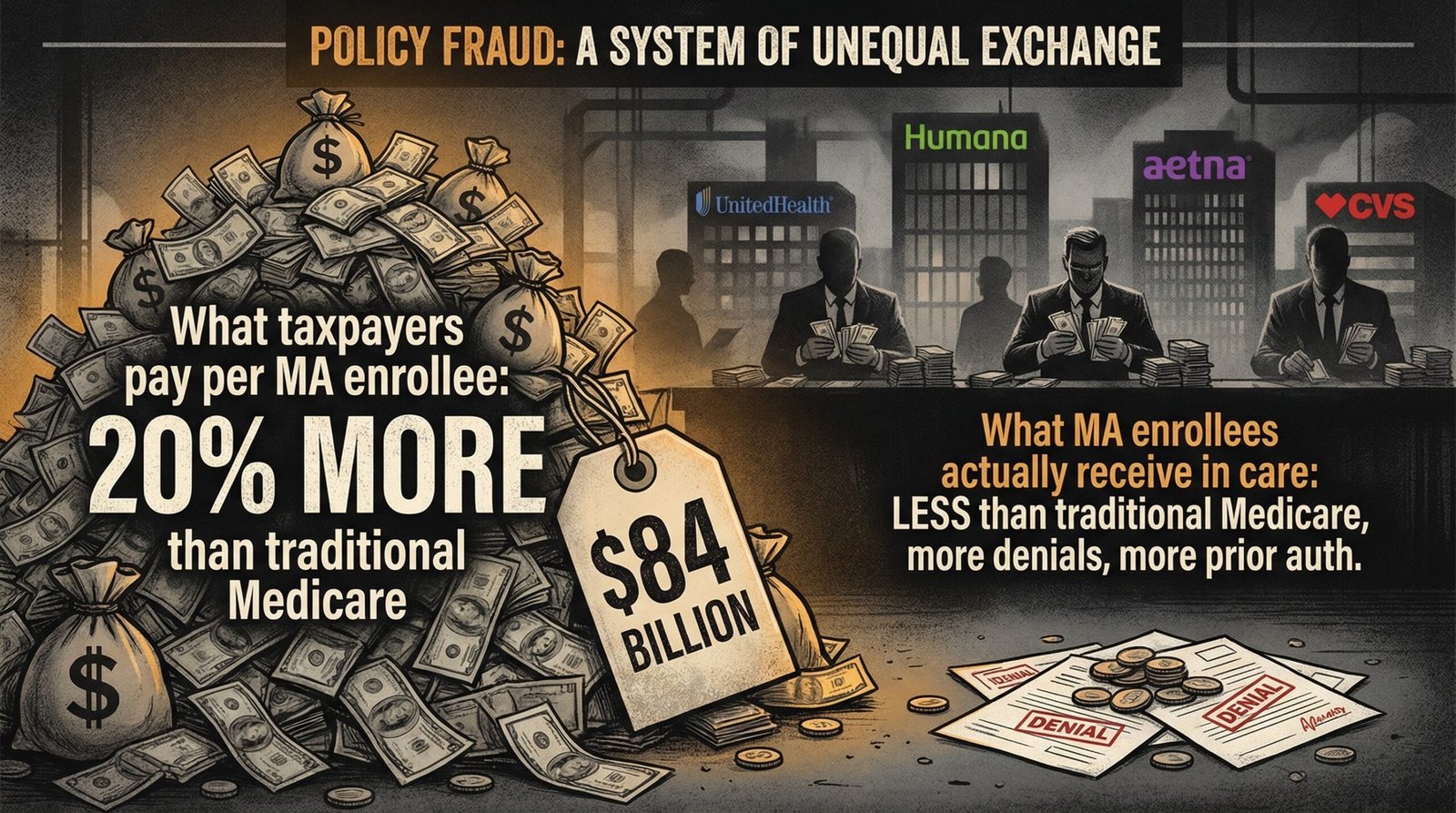

- MedPAC’s March 2025 report estimates taxpayers overpay Medicare Advantage plans by $84 billion in 2025 — approximately 20% more per enrollee than traditional Medicare would cost for the same beneficiaries.

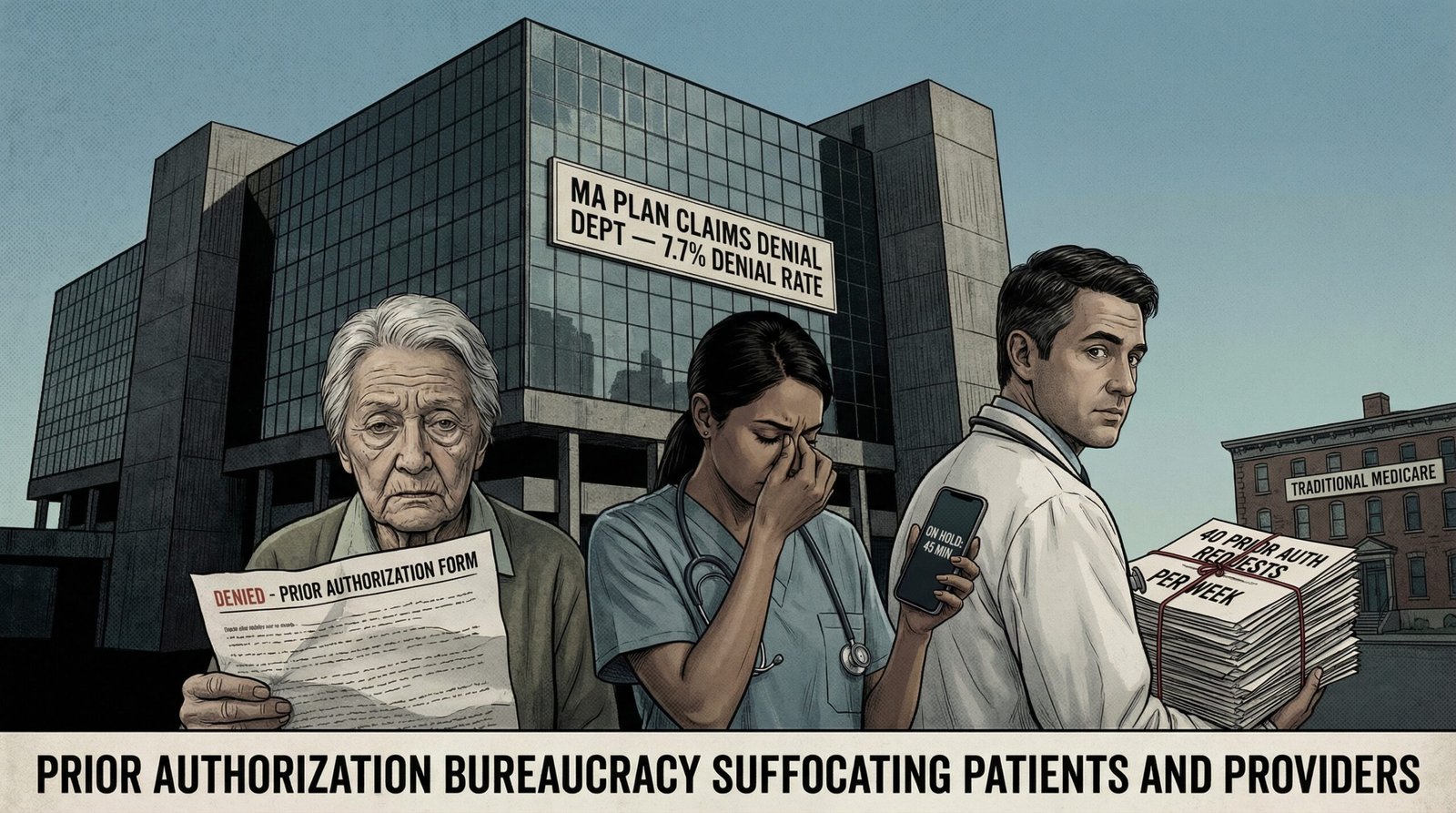

- Medicare Advantage plans issued 53 million prior authorization requests in 2024, denying 4.1 million (7.7%) — up from 6.4% in 2023. Of contested denials, more than 80% were overturned on appeal, suggesting routine denial of legitimate care.

- The HHS Inspector General found that diagnoses added only through health risk assessments — with no corresponding medical care — resulted in $7.5 billion in improper overpayments in 2023 alone. Just 20 companies drove 80% of those questionable payments.

- Kaiser Permanente paid a $556 million DOJ settlement in January 2026 — the largest Medicare Advantage fraud settlement to date — for allegedly billing for conditions patients didn’t have. CVS/Aetna settled for $117.7 million in 2024 for the same conduct.

- MA overpayments raised Part B premiums by $212 per person in 2025 ($13.4 billion total), according to a March 2026 congressional report — meaning even seniors in traditional Medicare paid more because of Medicare Advantage fraud.

- Quality bonus payments to MA plans totaled at least $12.7 billion in 2025 — $74 billion since 2015 — based on star ratings that insurers have systematically gamed, and which the Trump administration now proposes to inflate further.

- By 2026, 10% of MA enrollees were forced to switch plans as insurers exited markets, up from just 1% as recently as 2018–2024. Since 2024, exits have left 52 counties with no MA plans at all. In seven states, over 40% of MA enrollees were stranded.

- Enrollees who disenroll from Medicare Advantage and return to traditional Medicare have spending 27% higher ($2,585 more) in the following year than comparable enrollees who stayed in traditional Medicare — a pattern consistent with access-to-care suppression under MA.

What Is Medicare Advantage — and How Did It Take Over Half of Medicare?

Medicare Advantage — officially Part C — is a private insurance alternative to Original Medicare (Parts A and B). Instead of the government paying providers directly for each covered service, the government pays a private insurer a fixed monthly amount per enrolled beneficiary, adjusted upward based on the beneficiary’s health risk scores. The insurer then manages the care, sets the network, and decides what requires prior authorization. In theory, competition and efficiency were supposed to make care better and costs lower than traditional fee-for-service Medicare. In practice, the opposite happened.

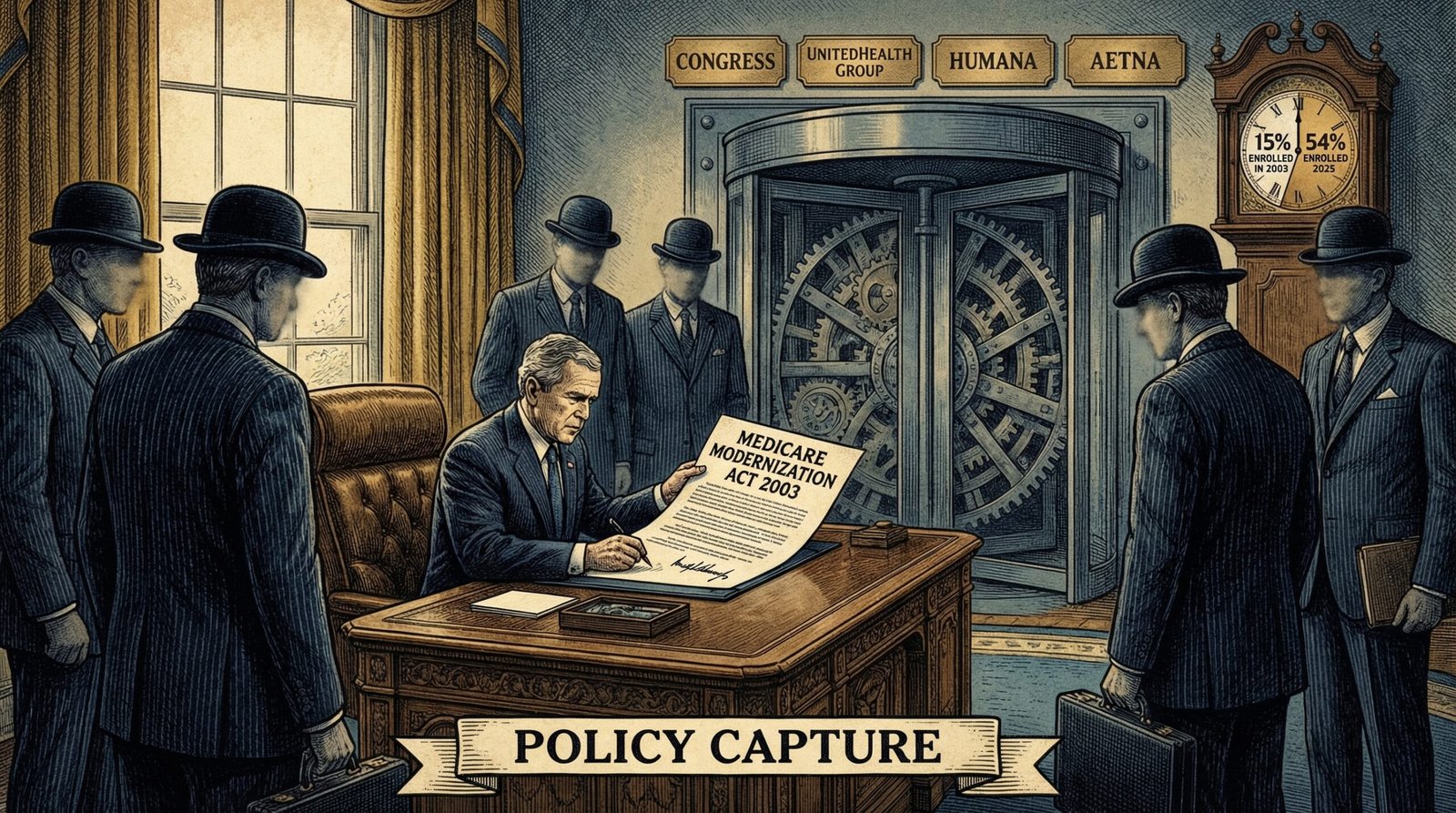

Medicare Advantage enrollment in 2025 stands at approximately 34.1 million — 54% of all Medicare-eligible Americans, according to KFF’s enrollment tracker. This is a dramatic transformation from what the program looked like in 2003, when roughly 5.3 million beneficiaries (about 13%) were enrolled in private Medicare plans. The growth wasn’t organic. It was engineered.

The history of private Medicare plans is a story of repeated federal rescues. An earlier version called Medicare+Choice, created in the Balanced Budget Act of 1997, collapsed after 2000 when insurers began exiting markets, citing inadequate payments. In 2001–2002, enrollment fell to under 5 million as plan exits accelerated. The insurance industry lobbied intensively for higher payments, and they got them: the Medicare Modernization Act of 2003 explicitly restructured payments to make MA plans more profitable, paying them significantly above traditional Medicare rates. Enrollment rebounded immediately. By 2007, it had reached 8.3 million. By 2014, 15.7 million. By 2025, 34.1 million.

That growth was accelerated by marketing: celebrity-endorsed TV commercials promising free dental, free vision, free gym memberships, and $0 premiums — benefits traditional Medicare doesn’t cover. What the commercials don’t mention: the prior authorization requirements, the narrow networks, the coding fraud, and the $84 billion annual taxpayer subsidy making those “free” benefits possible. Related: why US healthcare costs $5.3 trillion per year, how private equity looted American hospitals, Medicare costs in 2026, and how AARP’s $1.85 billion insurance business creates conflicts in the Medicare debate.

The 2003 Medicare Modernization Act: How the Drug Industry and Insurers Wrote Themselves a $84 Billion Annual Check

The Medicare Modernization Act of 2003 is best known for creating the Medicare Part D prescription drug benefit — a landmark addition that nonetheless contained a prohibition on the federal government negotiating drug prices directly, a gift to the pharmaceutical industry that cost taxpayers hundreds of billions over the next two decades. Less discussed but equally consequential was what the MMA did to the payment structure for private Medicare plans.

The MMA set benchmark payments for MA plans at 107% of traditional Medicare costs in most counties — a floor deliberately above what it cost to cover beneficiaries in the government program. The stated rationale was that the higher payments would attract more insurers and drive competition. The unstated reality was that insurers had been threatening to exit unless they got paid more, and Congress — whose members had received extensive insurance and pharmaceutical industry campaign contributions — complied. The law was written partly by pharmaceutical industry lobbyists, including at least one who crossed the revolving door to become a congressman and then a drug company executive in the same legislative cycle.

The Affordable Care Act of 2010 attempted to claw back some of the overpayment, beginning a gradual reduction in MA benchmark payments toward parity with traditional Medicare. Insurers threatened market exits, enrollment growth slowed, and Congress largely preserved supplemental bonus payments through the star ratings quality bonus program that effectively offset the ACA-mandated reductions. The revolving door lobbying machine between the insurance industry and Congress has ensured that every attempt to rationalize MA payments encounters determined resistance.

By the time MedPAC issued its March 2025 status report on Medicare Advantage, the cumulative effect of two decades of overpayment was stark: Medicare will pay MA plans a total of $84 billion more in 2025 than the program would have spent if enrollees had been in traditional Medicare. A decade earlier, when only about a third of beneficiaries were in MA, the overpayment was $18 billion. The scale of the overpayment has grown faster than enrollment because risk score inflation has compounded the per-enrollee excess every year.

The 2003 MMA paid private insurers 107% of what traditional Medicare cost, to attract competition. Twenty-two years later, they’re billing 120% — and using the extra 13% to run commercials promising free dental and gym memberships while denying your claims.

The $84 Billion Overpayment: How Medicare Advantage Costs Taxpayers 20% More Per Enrollee Than Traditional Medicare

The overpayment problem in Medicare Advantage operates through a mechanism called risk adjustment. The government pays MA plans a fixed monthly amount per enrollee, adjusted upward for sicker beneficiaries based on documented diagnoses. The theory is actuarially sound: patients with diabetes, heart disease, or cancer cost more to treat, so insurers should be compensated accordingly. The practice has been systematically exploited.

Research published in peer-reviewed journals finds that MA enrollees generate 6–16% higher diagnosis-based risk scores than comparable beneficiaries in traditional Medicare — not because they’re sicker, but because MA plans have powerful financial incentives to document as many diagnoses as possible, including through in-home health risk assessments that add codes to a beneficiary’s record without any accompanying medical care or treatment. More codes mean higher risk scores. Higher risk scores mean more federal dollars per enrollee. It’s a billing optimization system disguised as a health assessment program.

The downstream effect on Medicare spending is massive. MedPAC’s March 2025 report estimates the $84 billion annual overpayment, and the Joint Economic Committee found in March 2026 that MA overpayments drove up Part B premiums by $212 per person in 2025 — a $13.4 billion total impact on every Medicare beneficiary, whether or not they chose a private plan. You didn’t enroll in Medicare Advantage. You still paid for its overbilling.

The care access problem runs parallel to the cost problem. A study of beneficiaries who disenroll from Medicare Advantage and return to traditional Medicare found they had spending 27% higher ($2,585 more per year) in the following year than comparable people who stayed in traditional Medicare continuously. This spending gap is the signature of care suppression: people who were in MA plans had needs that weren’t being met, which became evident once they were in a system that didn’t require prior authorization for every procedure. Related: how insurers collected long-term care premiums for decades and then fled the market, and private equity’s gutting of nursing home staffing.

More Premiums, More Denials: Why Medicare Advantage Refuses More Care Than the Program It Replaced

Traditional Medicare is not a model of flawless coverage. It has cost-sharing requirements, coverage gaps (most famously the absence of dental, vision, and hearing coverage), and administrative complexity that confuses many beneficiaries. Medicare Advantage was designed to address these gaps through supplemental benefits, funded by the payment efficiencies that competition was supposed to generate. It has mostly generated a different problem: a massive prior authorization apparatus that requires physicians to obtain insurer permission for procedures, referrals, post-acute care placements, and medications before care can proceed.

The 2024 data on Medicare Advantage prior authorization is sobering. Becker’s Payer analysis of KFF data found that MA plans issued 53 million prior authorization requests in 2024 and fully or partially denied 4.1 million (7.7%) — up from 6.4% in 2023. Health Affairs found initial claim denial rates in MA settings at approximately 17% — more than double traditional Medicare rates. Health Care Dive’s analysis found that enrollees appealed only about 12% of denied authorization requests — but of those appeals, more than 80% were partially or fully overturned.

The math embedded in that 80% appeal overturn rate is important. If 4.1 million requests were denied, and 12% were appealed (roughly 492,000), and 80% of those were overturned (roughly 393,600 reversals), that means approximately 3.7 million denied requests went unappealed — the vast majority of them from patients who likely didn’t know they could appeal, couldn’t navigate the process, or were too sick to fight their insurer while simultaneously trying to access care. The MedPAC 2024 report to Congress documented these prior authorization access barriers in depth, noting that the complexity disproportionately harms lower-income and less-educated beneficiaries.

The Senate Finance Committee has separately documented deceptive marketing practices in Medicare Advantage: beneficiaries enrolled through TV commercials featuring celebrities (Joe Namath, Jimmy JJ Walker, William Shatner) promising benefits that turn out to require copays, prior authorizations, or narrow networks that don’t include their current providers. The Senate Finance Committee report on deceptive MA marketing documented hundreds of instances of false and misleading advertising. CMS has issued new marketing rules, but enforcement remains limited.

The $7.5 Billion Phantom Diagnosis Scam: How Insurers Rigged the Risk Score System

The billing fraud at the center of Medicare Advantage isn’t a fringe phenomenon. It is structural and systematic, built into the incentive architecture of risk-adjusted capitated payments. When insurers get paid more for sicker patients, they have an obvious financial motive to make patients look sicker — not by falsifying records outright (which is prosecutable fraud) but by maximizing the number of diagnosis codes attached to each patient’s record through processes that are difficult for CMS to audit.

The mechanism that has attracted the most OIG scrutiny is the in-home health risk assessment (HRA). MA plans send nurses, paramedics, or contracted health workers to enrolled beneficiaries’ homes to conduct health screenings. These visits serve a legitimate purpose — they can identify unmet health needs. But they’ve also become vehicles for adding diagnosis codes to a beneficiary’s record that would never be documented by the beneficiary’s actual treating physician, because they don’t reflect active, treated medical conditions. The OIG found that in many cases, diagnoses added through HRAs had no corresponding medical services, no treatment plan, and no mention in subsequent clinical documentation.

In October 2024, the HHS Office of Inspector General issued a landmark report estimating that HRA-linked diagnoses with no additional spending resulted in $7.5 billion in questionable Medicare Advantage payments in 2023 alone. Critically: just 20 Medicare Advantage companies were responsible for 80% of those questionable payments — a concentration that the OIG said warrants targeted enforcement action. The report recommended that CMS strengthen its Risk Adjustment Data Validation audit program, limit the use of HRA-only diagnoses in risk calculations, and require that diagnosis codes be supported by evidence of active treatment.

The DOJ has also been pursuing fraud settlements. In January 2026, Kaiser Permanente agreed to a $556 million settlement — the largest Medicare Advantage fraud settlement on record — for allegedly using data mining and medical record addenda to bill for conditions patients didn’t have. CVS/Aetna settled for $117.7 million in 2024 for submitting incorrect diagnoses to inflate risk scores. These are not rogue actors: they are the first and third largest Medicare Advantage insurers in the country.

The RADV (Risk Adjustment Data Validation) audit system that CMS uses to recover overpayments has been, until recently, largely toothless. The last significant recovery occurred after 2007 audits that recouped $13.7 million — a rounding error against billions in identified overpayments. Courts limited CMS’s ability to extrapolate audit findings to non-audited plans. The Biden administration proposed stronger RADV rules in 2023; the Trump administration accelerated them in early 2026, announcing plans to audit all eligible MA contracts for every payment year — a significant escalation, though critics note the enforcement agency is simultaneously being staffed down through DOGE cuts.

Star Ratings, Gaming, and the $12.7 Billion Bonus System Nobody Asked For

On top of the base capitated payment and risk adjustment, Medicare Advantage plans receive additional quality bonus payments based on a 1–5 star rating system administered by CMS. Plans rated 4 stars or above receive bonus payments — extra federal money added to their per-enrollee capitation rate. The stated purpose is to incentivize quality. The actual effect has been to create a second billing optimization game layered on top of the first one.

According to KFF’s analysis, estimated bonus payments to Medicare Advantage plans will total at least $12.7 billion in 2025 — and since 2015, the program has paid out approximately $74 billion in quality bonuses. The bonus program is not budget-neutral; it is an additional expenditure on top of the base overpayment. And unlike most quality programs in healthcare, there is no requirement that the bonuses be spent on patient care — they flow to the insurer’s bottom line.

The star ratings themselves have been extensively gamed. Plans have focused resources on measures that move star ratings upward — medication adherence surveys, member satisfaction scores, preventive screening rates — while the underlying care access, denial rates, and patient outcome measures receive less attention. CMS recalculated star ratings in 2024 after finding methodological problems, and the Trump administration in November 2025 proposed scrapping a dozen quality measures entirely and reversing prior Biden-era modifications. The result: STAT News estimated the changes would cost taxpayers an additional $13.2 billion between 2028 and 2036 as more insurers qualify for higher star ratings and the associated bonus payments — money that flows to the same insurers that have been cited for overbilling, claim denials, and deceptive marketing.

When the Plan Leaves Town: Medicare Advantage Exits Are Stranding Seniors Across Rural America

The final piece of the Medicare Advantage accountability picture is the market exit problem. Insurers entered Medicare Advantage markets aggressively during the years of generous benchmark payments. When CMS began tightening rates and enforcement in 2024–2025, many of those same insurers began contracting — exiting counties, reducing plan offerings, and forcing enrolled beneficiaries to find new coverage with little notice.

The scale of disruption is significant and accelerating. A study published in JAMA and reported by MedPage Today found that the mean forced disenrollment rate for Medicare Advantage beneficiaries jumped from just 1% in 2018–2024 to 6.9% in 2025 and 10% in 2026. Reuters reported in February 2026 that in seven states, more than 40% of Medicare Advantage enrollees were left scrambling as plans exited — with Vermont facing an extraordinary 92% forced disenrollment rate. Since 2024, insurer exits have left 52 counties with no Medicare Advantage plans available at all, according to Modern Healthcare.

For seniors in these counties — many of them rural, elderly, and with limited technological literacy or transportation — finding new coverage is not a frictionless consumer experience. It requires comparing complex plan designs, understanding drug formularies, checking whether their physicians are in-network, and navigating an open enrollment window. Many beneficiaries, particularly those with cognitive decline, rely on family members or insurance brokers to navigate the process. When the plan exits abruptly, the practical consequences include interrupted care, lost specialist relationships, and medication disruptions.

The exits are also geographically concentrated in exactly the rural, lower-income markets where Medicare Advantage marketing has been most aggressive — and where traditional Medicare infrastructure (supplemental Medigap coverage) is most expensive relative to local incomes. Beneficiaries who were lured into MA by zero-premium promises may now face the stark reality that returning to traditional Medicare requires purchasing a Medigap supplement policy — at prices that reflect their current age and health status — or accepting the cost exposure of uncovered Medicare gaps.

The Counter-Argument: Medicare Advantage Has Real Benefits — and Reform Is More Complicated Than It Looks

The problems with Medicare Advantage are real and documented. The counterarguments deserve fair treatment, because not everything about the program is a straightforward fraud story.

Supplemental benefits matter: Traditional Medicare’s coverage gaps are genuine. The absence of dental, vision, and hearing coverage leaves millions of seniors with substantial out-of-pocket costs that have real health consequences — untreated dental disease worsens diabetes and cardiovascular disease; untreated hearing loss accelerates cognitive decline. Medicare Advantage’s supplemental benefits, even if partially funded by overbilling, provide real value to real enrollees, particularly lower-income beneficiaries who can’t afford Medigap supplements.

Some MA plans perform well: The program is not uniformly bad. Some regional HMOs and integrated health systems operating MA plans — Kaiser Permanente (pre-settlement), Geisinger, UPMC — have demonstrated better care coordination, higher preventive care rates, and lower total cost of care than their fee-for-service Medicare counterparts in certain markets. The problem is that these high-performing plans represent a minority of enrollment, and the broad overpayment flows to every plan, including the ones committing fraud.

Administrative fixes are available: The overpayment problem does not require eliminating private Medicare. It requires accurate risk adjustment that can’t be gamed through phantom diagnoses, stronger RADV audit enforcement with real extrapolation authority, HRA-linked code restrictions, and star ratings that measure actual patient outcomes rather than process metrics. The Trump administration’s accelerated RADV audit push — whatever its partisan motivations — is directionally correct if actually implemented. The challenge is that the same administration is simultaneously proposing to inflate star ratings and add $13 billion in bonus payments.

Medicare solvency is real: As we covered in our analysis of Social Security’s 2033 funding cliff, entitlement program financing is under genuine long-term pressure. Reducing $84 billion in annual MA overpayments would materially extend Medicare’s solvency horizon — not solve it, but meaningfully delay it. The political obstacles to doing so are formidable: the insurance industry spent heavily to maintain the current payment structure, and Medicare Advantage beneficiaries — now a majority of Medicare enrollees — would resist any change that threatened their supplemental benefits, even if the underlying cost to taxpayers was reduced.

FAQ: Medicare Advantage

Is Medicare Advantage better than traditional Medicare?

It depends on the plan, the beneficiary’s health needs, and location. Medicare Advantage can offer lower premiums and supplemental benefits (dental, vision, hearing) that traditional Medicare doesn’t cover. But MA plans require prior authorizations that traditional Medicare does not, have narrower networks, and may restrict access to specialized care. Research shows that people who disenroll from MA and return to traditional Medicare show 27% higher spending in the following year, suggesting suppressed care access under MA. For healthy, lower-income beneficiaries in areas with strong MA plan options, the supplemental benefits can be genuinely valuable. For those with complex chronic conditions, traditional Medicare plus a Medigap supplement typically provides more reliable, unrestricted access to care.

How much does Medicare Advantage cost taxpayers compared to traditional Medicare?

The Medicare Payment Advisory Commission (MedPAC) estimates that in 2025, Medicare will pay MA plans $84 billion more than it would have paid for the same beneficiaries in traditional Medicare — approximately 20% more per enrollee. This overpayment is driven by a combination of above-parity benchmark payments, risk score inflation through diagnosis upcoding, and quality bonus payments. A March 2026 congressional report found that MA overpayments drove up Part B premiums by $212 per person in 2025 ($13.4 billion total), affecting all Medicare beneficiaries, including those in traditional Medicare who did not choose a private plan.

What is Medicare Advantage risk score fraud?

Medicare Advantage plans receive higher payments from the federal government for sicker enrollees, based on documented diagnoses (risk scores). Insurers have exploited this system by adding diagnosis codes to beneficiaries’ records through in-home health risk assessments, often without any accompanying medical care or treatment. The HHS Inspector General estimated in October 2024 that HRA-linked diagnoses with no additional medical services resulted in $7.5 billion in improper Medicare Advantage payments in 2023 alone. Major settlements include Kaiser Permanente ($556 million, January 2026) and CVS/Aetna ($117.7 million, 2024), both for risk score manipulation. CMS’s RADV audit program is designed to recover these overpayments, but enforcement has historically been inadequate relative to the scale of overbilling.

Can Medicare Advantage plans exit the market and leave beneficiaries without coverage?

Yes. Medicare Advantage plans can exit individual counties or entire markets at the end of a contract year, forcing enrolled beneficiaries to find new coverage. By 2026, 10% of MA enrollees were forced to switch plans due to insurer exits — up from just 1% during 2018–2024. In seven states, more than 40% of MA enrollees were affected. Since 2024, exits have left 52 counties nationwide with no Medicare Advantage options at all. Beneficiaries in plans that exit can generally either enroll in a new MA plan (if available in their area) or return to traditional Medicare, though they may face Medigap premium increases reflecting their current age and health if they do the latter.

Sources & Methodology

Data sources used in this article:

- MedPAC — March 2025 Medicare Advantage Status Report to Congress — $84 billion overpayment estimate; 20% per-enrollee excess over traditional Medicare; 27% higher spending among MA disenrollees

- KFF — Medicare Advantage Enrollment Update and Key Trends, 2025 — 34.1 million enrolled; 54% of Medicare beneficiaries; enrollment growth 2007–2025

- HHS OIG — Questionable Use of Health Risk Assessments, October 2024 — $7.5 billion improper overpayments 2023; 20 companies = 80% of questionable payments

- Medicare Rights Center / Joint Economic Committee — MA Overpayments and Part B Premiums, March 2026 — $212 per person premium increase; $13.4 billion total 2025 impact

- Becker’s Payer — 53 million MA prior authorization requests 2024, KFF data — 4.1 million denials; 7.7% denial rate; up from 6.4% in 2023

- Health Care Dive — MA prior authorization rise 2024 — 12% appeal rate; 80%+ of appeals overturned

- Aptarro / Health Affairs — 17% initial denial rate MA vs traditional Medicare

- KFF — Medicare Advantage Quality Bonus Payments — $12.7 billion bonus payments 2025; $74 billion since 2015

- STAT News — Trump admin MA star ratings changes, $13.2 billion additional cost 2028–2036

- Axios — Trump proposes scrapping dozen MA quality measures, November 2025

- MedPage Today / JAMA — Forced disenrollment rate 1% → 6.9% (2025) → 10% (2026)

- Reuters — 40%+ forced disenrollment in 7 states; 92% Vermont; February 2026

- Modern Healthcare — 52 counties with no MA plans available since 2024

- Medicare Rights Center — Medicare Advantage Legislative Milestones — MMA 2003 payment structure; Medicare+Choice collapse; history

- Senate Finance Committee — Deceptive Marketing Practices in Medicare Advantage

- KFF Health News — Federal government killed plan to curb MA overbilling after industry lobbying

- Groom Law — Trump administration accelerated MA RADV audits, 2026 — CMS to audit all eligible MA contracts; Payment Year 2020 audits beginning February 2026

Methodology: Enrollment and overpayment figures from MedPAC March 2025 Medicare Advantage status report to Congress. Prior authorization denial statistics from KFF analysis of CMS MA data, via Becker’s Payer and Health Care Dive. Risk score overpayment figures from HHS OIG October 2024 HRA report. DOJ settlement figures from DOJ press releases and reporting. Part B premium impact from Joint Economic Committee March 2026 report via Medicare Rights Center. Quality bonus payment totals from KFF. Forced disenrollment statistics from JAMA study reported by MedPage Today and Reuters, February 2026. Star ratings bonus cost estimate from STAT News analysis of CMS proposed rule, November 2025.