Hidden 401(k) fees are quietly draining American retirement accounts at a rate of $50 billion or more per year — siphoned through expense ratios, 12b-1 marketing fees, recordkeeping charges, and advisor commissions that most workers never see on their statements. A median-income two-earner family will lose nearly $155,000 over a lifetime to these charges. The 401(k) was sold as the democratization of investing. It turned out to be the financialization of retirement — and Wall Street wrote every clause of the contract.

Key Takeaways: Hidden 401(k) fees cost the median two-earner household up to $155,000 over a lifetime. A 1% fee difference can cut your final balance by nearly 25% — and force you to work 5–7 extra years. There are at least six distinct fee layers most workers can’t see. The fiduciary rule that would have forced advisors to act in your interest was killed in court and abandoned by the Trump DOL in 2025. Congress has never passed a fee cap. Millennials — who already have catastrophically low retirement balances — are the generation most exposed to a lifetime of compounding fee extraction.

What Are Hidden 401(k) Fees?

The word “hidden” isn’t an exaggeration. The fees embedded in your 401(k) plan are disclosed — technically — but in a way specifically designed to minimize your chances of understanding them. They’re scattered across prospectuses, Form 5500 filings, and 408(b)(2) disclosures that less than 5% of participants ever read. Nearly 41% of Americans don’t even know they’re paying 401(k) fees at all, according to a survey by TNS. Of those who do know, most dramatically underestimate how much.

There are at least six distinct fee categories:

- Expense ratios — The annual percentage charged by the mutual fund itself, covering management, operations, and sometimes marketing. The average for equity mutual funds in 401(k)s is 0.26% (2024), but small-plan participants often pay 0.75%–1.5%+ in actively managed funds.

- 12b-1 fees — A legally sanctioned kickback buried inside your mutual fund’s expense ratio. Named after an obscure 1980 SEC rule, these fees — typically 0.25%–1% annually — are paid by the fund company to the broker who sold the fund into your plan. You pay the broker; you get nothing.

- Recordkeeping fees — The plan administrator charges $45–$80 per participant per year to track your balance and generate statements. Often “revenue-shared” from fund companies, meaning your fund choices determine who gets paid.

- Advisor/plan consultant fees — If your plan uses a financial advisor, expect 0.16%–0.64% of assets per year. On a $500,000 plan, that’s $800–$3,200 annually — on top of everything else.

- Trading costs — Hidden inside the fund, estimated at approximately 1.2% annually for actively managed funds, representing the bid-ask spread and market impact of buying and selling securities.

- Individual service fees — $50–$100 for a loan. Processing fees for withdrawals and rollovers. Minor in isolation; death by a thousand cuts over 30 years.

The truly insidious part? The 401(k) system was never designed with your interests as the primary objective. It was designed as a tax shelter for executives. The expansion to rank-and-file workers was a political accident — and the financial industry spent four decades engineering every loophole before most workers even knew the game existed.

How Much Do 401(k) Fees Cost Over a Lifetime?

The most comprehensive analysis comes from Demos, a policy research organization that modeled the lifetime cost of hidden 401(k) fees for median-income two-earner households. Their findings are brutal:

- A median-income two-earner household loses approximately $154,794 over a lifetime to 401(k) fees and lost compounded returns.

- A higher-income household may lose up to $277,969.

- The total fees consumed nearly one-third of their potential investment returns.

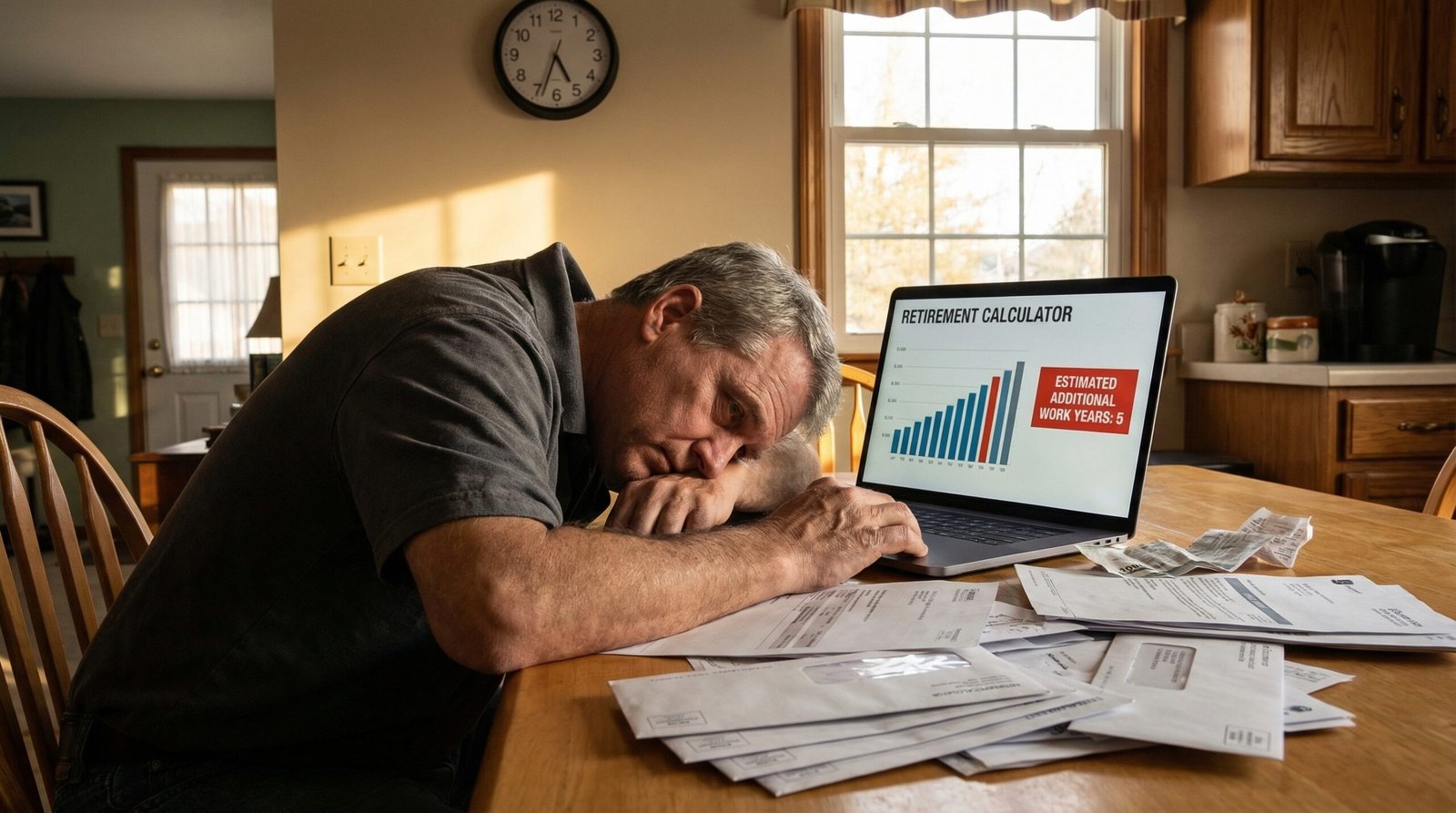

The compounding math is where the real theft happens. At 8% annual returns, a 1% fee difference reduces your terminal balance by nearly 25% over 30 years. If you invest $10,000 per year for 30 years in a plan charging 0.87% versus one charging 3.56%, you end up with approximately $1,035,000 versus $630,000 — a difference of $405,000.

That $405,000 didn’t vanish. It transferred — as predictably as clockwork — from your retirement account to the financial services industry. And a 1% fee difference forcing a worker to delay retirement by 4–7 years means years of labor extracted from someone who already can’t afford to retire. That intersection with Social Security timing has its own brutal math.

There are currently $10.0 trillion in 401(k) assets (Q3 2025, ICI). At a conservative 0.5% average annual drag from excess fees beyond what an all-index-fund plan would cost, the industry is extracting roughly $50 billion per year. At the ICI’s own broader estimate of average plan costs, the number is higher. The financial industry has built a perpetual annuity out of your retirement savings — and Congress blessed every line of it.

Why Are Index Funds Better Than Actively Managed Funds?

The financial industry’s core sales pitch for actively managed funds is that professional stock pickers can beat the market. The data says otherwise — and has for decades. In 2025, only 38% of actively managed mutual funds beat their passive counterparts, down from 42% in 2024. Over 15-year periods, roughly 85–90% of active funds underperform their benchmark index.

The fee comparison is damning:

- S&P 500 index fund average expense ratio: 0.05%

- Actively managed equity mutual fund average: 0.64%

- 75th percentile of actively managed domestic equity funds: 0.74%, versus 0.15% for index equivalents

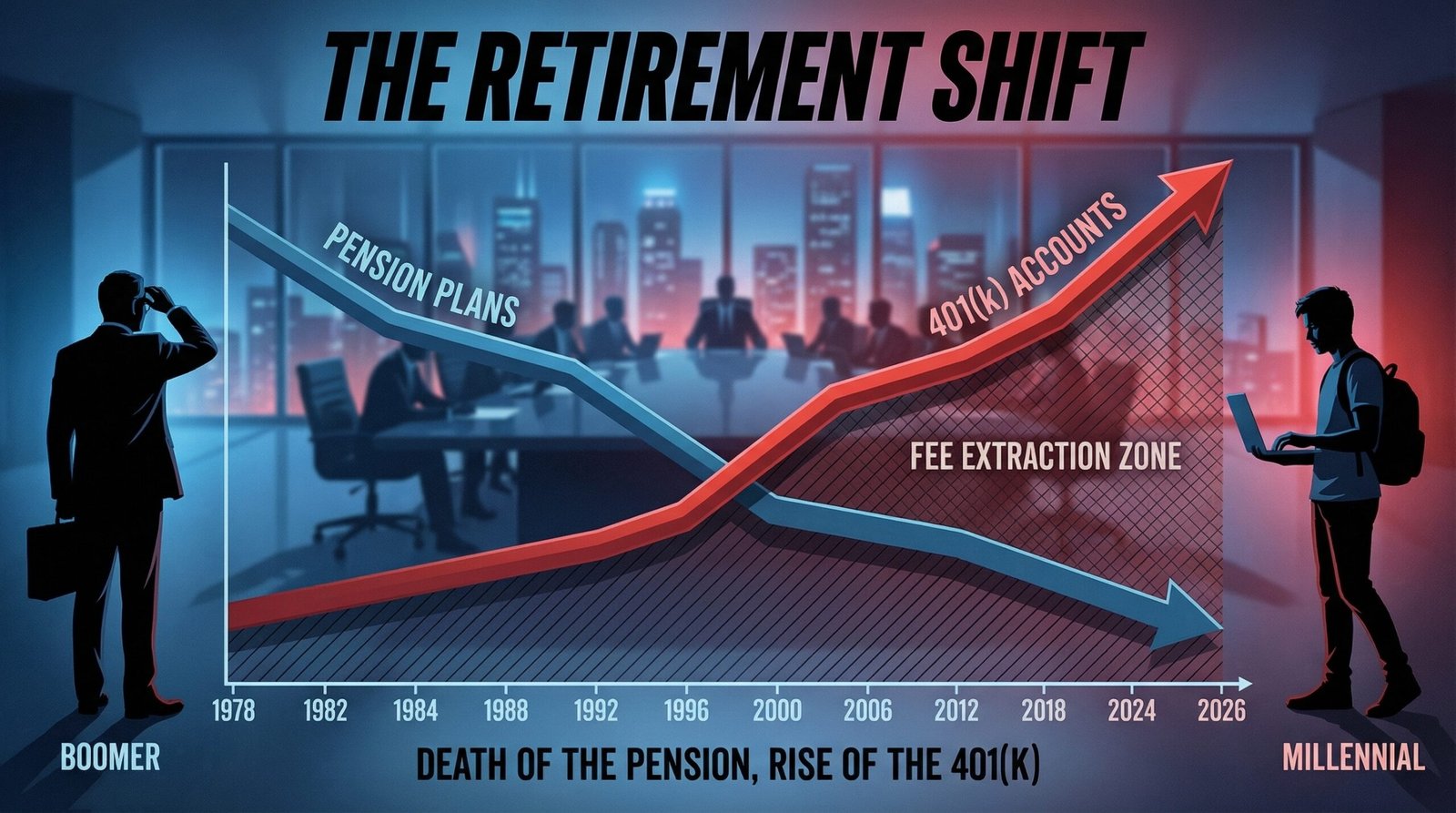

So the average actively managed fund charges 13 times more than an index fund — and loses to it 85–90% of the time over long horizons. The shift from pensions to 401(k)s transferred not just investment risk to workers, but also the cost of inferior investment products. Your grandfather’s pension fund had professional managers negotiating institutional rates. Your 401(k) charges you retail prices for performance that trails a computer running an index.

Why are actively managed funds still in most 401(k) plans? Because the plan sponsor (your employer) often selects them based on relationships with financial advisors who receive 12b-1 kickbacks from the fund companies. The fund that pays the advisor the most is the fund that ends up in your plan. That’s not a conspiracy theory — it’s the disclosed structure of the system, operating legally, every day.

How Did the Fiduciary Rule Get Killed?

For most of its history, the 401(k) system operated without any legal requirement that financial advisors act in their clients’ best interest. Advisors were held to a “suitability” standard — meaning they only had to recommend products that were “suitable,” not necessarily the best or lowest-cost option. This allowed advisors to legally steer clients into higher-fee products that paid larger commissions.

The Obama administration’s DOL fiduciary rule (2016) would have changed this — requiring any advisor giving retirement account advice to act as a fiduciary. The financial services industry mobilized immediately. Lobbying, lawsuits, and a Fifth Circuit ruling in 2018 killed it before it fully took effect.

The Biden administration tried again in 2024, finalizing a new “Retirement Security Rule” in April 2024 that expanded fiduciary status to cover rollover advice — the single most lucrative moment for advisors steering workers from low-fee 401(k)s into higher-fee IRAs. The financial industry sued again. Courts issued stays. And in January 2025, the Trump DOL dropped the government’s defense of the rule entirely. It is now dead.

The result: advisors remain legally free to recommend the highest-commission product in the room when you roll over your 401(k) at retirement — the moment you’re most vulnerable, with the most money to move, and the least expertise to evaluate the advice. The revolving door between the financial industry and the agencies that regulate it has never stopped spinning. The fiduciary rule was killed twice in eight years by the same industry it would have constrained.

Who Built This System — and Why?

The 401(k) was created by a single paragraph in the Revenue Act of 1978 — a provision so obscure its author, Rep. Herbert Harris, didn’t fully grasp its implications. It was intended as a supplement to pensions for highly compensated employees. Within a decade, corporate America had weaponized it to eliminate defined-benefit pensions entirely.

The shift saved corporations billions in guaranteed pension obligations and transferred investment risk entirely to workers. The pension-to-401(k) transition is one of the most consequential wealth transfers in American history — and the workers who bear the risk of bad markets also bear the cost of a fee structure that guarantees someone else profits regardless of market performance.

Who benefits from this system?

- Mutual fund companies collecting expense ratios on $10 trillion in assets

- Financial advisors earning 12b-1 kickbacks and rollover commissions

- Recordkeepers (Fidelity, Vanguard, Empower) charging per-head fees on 70+ million plan participants

- Corporations that eliminated pension liabilities while appearing to offer generous benefits

- Congress — which has collected decades of campaign contributions from the financial services industry and produced zero fee caps

The Boomer generation largely built this system during their peak political years — the 1970s through 1990s. They also largely escaped its worst consequences: many had defined-benefit pensions from earlier careers, accumulated 401(k)s in a 40-year bull market, and now hold 51% of America’s wealth as they draw down. Millennials, by contrast, entered the workforce in 2008, have a median 401(k) balance of $83,700, and face 30–40 more years of fee extraction on whatever they manage to save.

Isn’t the Market Just Fixing Itself?

The financial industry’s favorite counter-argument is that fees have fallen dramatically — and that’s true. Average equity mutual fund expense ratios dropped from 0.76% in 2000 to 0.26% in 2024, driven largely by Vanguard’s index fund expansion and the rise of ETFs. The index fund revolution is real, and it has saved ordinary investors billions.

But “improving” and “fixed” are not the same thing. Consider:

- Nearly 80% of corporate 401(k) plans with 100+ employees are still overpaying on administrative fees, per Form 5500 analysis.

- Small-plan participants (companies under 100 employees) still routinely pay total plan costs of 1.5%–3.5%, because their small asset base gives them no negotiating leverage.

- 31.9 million abandoned 401(k) accounts representing $2.1 trillion in assets (up 30% since 2023) are quietly being charged fees with no active oversight from their owners.

- The fiduciary standard is still dead — fee reductions on the investment side haven’t changed the advisor compensation structure that steers money into higher-fee products at rollover.

- The DOL’s 2025 guidance opened the door to private equity and alternative assets in 401(k)s — products that typically carry 2%+ fees and severe liquidity restrictions.

Market competition works when consumers can compare prices and switch providers. In most 401(k) plans, you cannot choose your recordkeeper, cannot negotiate your expense ratios, and cannot fire the advisor your employer selected. The market is not fixing itself — it is adjusting the most visible number while maintaining the structural fee extraction that makes the industry profitable.

FAQ: Hidden 401(k) Fees

How do I find out what fees I’m paying on my 401(k)?

Request your plan’s 408(b)(2) disclosure from your HR department or plan administrator — federal law requires this document be available to participants. Look for the “total plan cost” and “participant-level fee” sections. The fund expense ratios are in the fund prospectus. Add them all together; the number will likely surprise you.

What is a good 401(k) expense ratio in 2026?

Under 0.15% for index funds. Under 0.75% for actively managed funds, though you should question why you’re in an actively managed fund at all given their long-run performance record. Total all-in plan costs (investment + administrative + advisor) under 0.5% annually is the target for a well-run plan.

Can I sue my employer over high 401(k) fees?

Yes — ERISA requires plan sponsors to act as fiduciaries and select prudent, reasonably priced investment options. There has been a wave of successful class action lawsuits against employers for selecting high-fee funds when cheaper alternatives were available. The Supreme Court has agreed to hear cases on the evidentiary standard in 2026.

Should I max out my 401(k) even if the fees are high?

Generally yes, up to the employer match — that’s free money and the tax deferral still helps. Beyond the match, if your plan has only high-fee options (total costs above 1%), a Roth IRA with low-cost index funds may be a better next dollar. Compare the tax benefit of the 401(k) deduction against the fee drag before contributing above the match.

Sources & Methodology

Fee data and statistics sourced from: Demos — The Retirement Savings Drain; Investment Company Institute 2025 expense ratio report; DOL — A Look at 401(k) Plan Fees; ICI Q3 2025 Retirement Market Data ($10.0T in 401k assets); Kiplinger fee comparison analysis; 401k Specialist — Fees Remain a Black Box; Mercer — DOL drops fiduciary rule appeal; Capitalize — 31.9M abandoned accounts; 401k Specialist — 80% of plans overpaying. 401(k) balance averages from Vanguard How America Saves 2025 and Fidelity 2025 data. Active vs. passive performance from CNBC/Morningstar February 2026. Internal links reference related boomersbrokeamerica.com coverage.