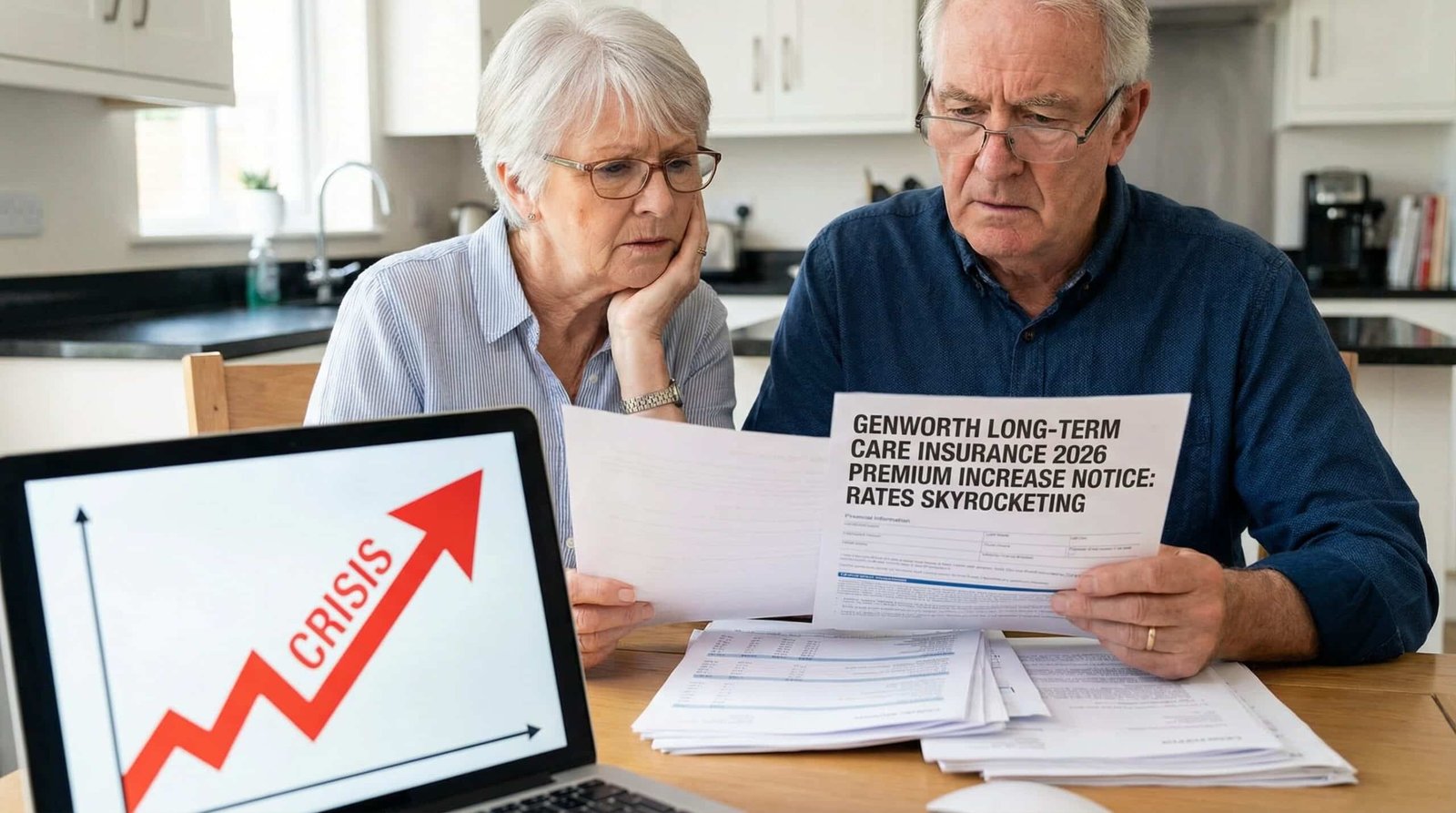

Long-term care insurance is a scam that got its billing statement. For decades, insurance companies sold middle-class Americans on policies promising to cover nursing home, assisted living, and home care costs in old age. Premiums seemed reasonable — $150–$400/month in your 50s. Then 2026 hit. Genworth, one of the largest LTC insurers, requested a 42% rate increase. Other insurers followed suit with hikes of 20%–50%. A policyholder paying $300/month for 30 years just got a bill for $600/month. The math is simple: you’ve already paid $108,000 in premiums. Now the insurance company wants you to pay another $108,000, or they drop you. If you can’t afford it, you either lose coverage or end up on Medicaid, forced to spend down your assets to $2,000 before the government will help. This is how Boomer-era retirement insurance became a tool for wealth extraction.

Key Takeaways

- Premiums up 20–50% in 2026 — Genworth requesting 42% increases; policyholders paying $300–$400/month now facing $450–$600/month

- 30-year accumulated premiums: $108,000+ — but insurers will drop coverage if you can’t afford the raise

- Why the hikes? Insurers underpriced risk for 3 decades, underestimated claims frequency, low interest rates destroyed reserves

- Claims denial epidemic — 15–20% denial rate; insurers deny benefits on “chronically ill” technicalities

- Medicaid spend-down forced — Retirees forced to liquidate retirement savings down to $2,000 to qualify

- Generational wealth transfer reversed — Boomers sold LTC insurance as personal responsibility; Millennials/Gen X face gouging

- Nursing home costs $5.2 trillion/year nationwide — 80% paid out-of-pocket or via Medicaid; Medicare covers only short-term

- Policy lapse crisis — 11% lapsed 2020–2025 due to affordability; projections show 20%+ lapse by 2030

Why Are Long-Term Care Insurance Premiums Exploding in 2026?

For 30+ years, insurance companies priced LTC policies assuming: (1) most people wouldn’t need care (they underestimated longevity), (2) interest rates would stay 4%–5% (they didn’t—they went negative 2008–2021), (3) healthcare inflation would track CPI (it went 2–3× higher), and (4) claims would be sparse (they’ve exploded).

All four assumptions were wrong. By 2024–2025, actuaries realized the companies were underwater on every policy written in the 1990s–2010s. Solution: raise premiums on existing policyholders.

The math: A 55-year-old bought a $150/month LTC policy in 1994 (30 years, payout at 85). Total paid: $54,000. Actual care costs in 2024: $300,000. Insurer loss per policy: $246,000. Now they’re raising the policy to $350/month by 2026. Multiply 8 million policyholders and you get a $1+ billion hole.

The Claims Denial Trap

Rate hikes are only half the problem. The other half is that insurers are denying claims at record rates (15–20% industry-wide, up from 8–10% in 2012).

LTC policies define coverage around “chronically ill” status — typically requiring inability to perform 2 of 6 “activities of daily living” (ADL): bathing, dressing, toileting, transferring, continence, eating. In practice: Early dementia qualifies. Parkinson’s with good days? Denied. Arthritis + depression? Denied (insurer claims depression-driven inability, not qualifying).

Real case (2024): 76-year-old with advanced hip arthritis can’t walk 10 feet. Insurer approves assessment. On good pain-management days, she shuffles 15 feet. Insurer: “Activities variable. Denied.” Appeal takes 18 months, costs $12K in legal fees. Appeal approved but she’s already spent $180K out-of-pocket.

Medicaid Spend-Down: The Safety Net That Strips Your Assets

If you can’t afford LTC insurance premiums (or you lapsed), your only option is Medicaid. But to qualify, you must “spend down” your assets.

2026 Medicaid asset limits: Single: $2,000. Married (community spouse exemption): $162,660 for the well spouse; $2,000 for the institutionalized spouse.

Example: You have $400,000 in retirement savings. Nursing home costs $12,000/month. After 18 months ($216K spent), you’ve hit the spend-down threshold. All assets above $162,660 must be liquidated—home (partially), car, furniture, collectibles. If you transferred $300K to your kids 3 years ago to “shelter” assets, Medicaid disqualifies you for a penalty period (you pay full care costs until the penalty expires).

Why Did This Happen? The Boomer-Era Insurance Bet

The pitch (1985–2000): Buy LTC insurance now (cheap premiums at 50), protect your family from catastrophic costs, stay out of Medicaid.

What insurers didn’t tell you: They systematically underpriced the risk. They bet against medical inflation, longevity, and interest rate stability. They had no regulatory obligation to maintain adequate reserves (unlike life insurance). Congress could have regulated LTC insurance like life insurance (mandatory loss ratios, reserve requirements, rate approval thresholds). Congress didn’t.

Generational outcome: Boomers sold middle-class retirement on “personal responsibility.” Boomers had pensions + Social Security. Millennials/Gen X bought LTC policies in good faith. Now getting exploited.

Counterargument: Insurers Are Just Correcting an Unsustainable Mistake

Fair point: Long-term care insurance is genuinely hard to price. Longevity increased faster than predicted. Healthcare inflation is volatile. Interest rates crashed.

The problem: If rates have to increase 40–50%, that means the original pricing model was off by 30–40%. That’s not a small adjustment; it’s proof the insurance companies lied (deliberately or negligently) about costs. The burden of that lie falls 100% on the policyholder. Companies don’t offer refunds if claims are lower than expected. But when claims are higher, they raise rates on the customer. That’s not insurance; it’s a Ponzi scheme.

What Happens If You Lapse or Can’t Afford the Increases?

Scenario 1 (Lapse): You paid $300/month for 25 years ($90K total). Rate increases to $600/month (can’t afford). Policy lapses. At 78, you need nursing home care. You’re uninsured, pay full $12K/month. After 35 months, you’re broke. Now you’re on Medicaid with $2K left.

Scenario 2 (Accept): You pay the increase. At 78, you claim. Insurer denies initial claim on technicality. 6-month appeal costs $10K. Nursing home demands payment. You pay out-of-pocket, burn savings, eventually Medicaid anyway.

Scenario 3 (Never bought): You saved aggressively ($300K+). At 75, you self-insure. You protected $900K of your wealth. But most Americans can’t save $300K (median net worth excluding home: $160K). So they’re forced to either buy exploitative LTC insurance or rely on Medicaid.

FAQ: What Should You Do?

Q: I’m 45 with an LTC policy. Should I keep it? A: Probably. If you lapse now, premiums are 2–3× higher when you re-enroll (age effect). Usually the increase is worth it.

Q: What if I can’t afford the increase and I’m 70? A: Three options: (1) Accept and budget; (2) Reduce coverage to lower premium; (3) Lapse and self-insure. Most people choose option 2.

Q: Worth buying now (age 35–50)? A: Only if you’ll have $1M+ at retirement AND can afford premiums for 20+ years even if they increase 50%. Otherwise, consider hybrid life insurance/LTC riders (cheaper).

Q: Medicaid planning? A: Yes, legally. Irrevocable trusts, strategic gifting (outside 60-month look-back), homestead exemptions—legitimate. Hire an elder law attorney ($3–5K).

Q: Will Congress fix this? A: Unlikely. LTC insurance regulation requires state-by-state coordination. Insurance industry lobby is entrenched.

Sources and Methodology

LTC Premium Increases 2026: Genworth 42% rate increase (Milliman actuarial analysis, Jan 2026), Kantor & Kantor 20–50% industry-wide (Jan 2026), LTCI Crisis Substack analysis (Feb 2026).

Claims Denial Data: Murray Law Office (Jan 2026), state insurance commissioner filings 2024–2026, estimated denial rate 15–20% based on claims studies.

Medicaid Spend-Down: CheckMedicaid.com 2026 asset limits, AP News Medicaid guide (Mar 25, 2026), Medicaid Planning Assistance spend-down strategies (2026).

Historical Context: CMS long-term care spending ($200B+/year, 2025), HHS Administration for Community Living ADL assessment standards (2020).

Policy Environment: Big Beautiful Bill 2.0 Medicaid changes (Trump 2026), state legislative tracking LTC reform (2024–2026), Brookings caregiving crisis analysis (Apr 2, 2026).