A 403(b) plan is a tax-deferred retirement account available to employees of public schools, nonprofits, and certain tax-exempt organizations — covering 14.5 million American workers, most of them teachers, nurses, and hospital staff. Unlike the 401(k) plans that for-profit company employees use, the majority of 403(b) plans are exempt from ERISA’s fiduciary protection requirements, which means the people selling them are not legally required to act in your interest. The result: decades of variable annuity products loaded with fees of 1–3% per year, surrender charges that lock you in for 7–10 years, and a vendor selection system built around kickbacks to school districts and union affiliates — all affecting workers who are already among the lowest-paid college-educated professionals in America.

Key Takeaways:

- 403(b) plans cover approximately 14.5 million American workers — primarily teachers, nurses, hospital staff, and nonprofit employees — who collectively hold roughly $1 trillion in 403(b) assets.

- Most government-sponsored 403(b) plans, including those covering K-12 public school teachers, are explicitly exempt from ERISA — the federal law that requires fiduciary accountability, fee transparency, and prudent investment selection in private-sector 401(k) plans.

- The typical 403(b) variable annuity charges 1–2.5% per year in total fees, compared to 0.03–0.10% for equivalent low-cost index fund options. The DOL estimates that each 1% in additional annual fees reduces a worker’s final retirement balance by approximately 17% over a 20-year period.

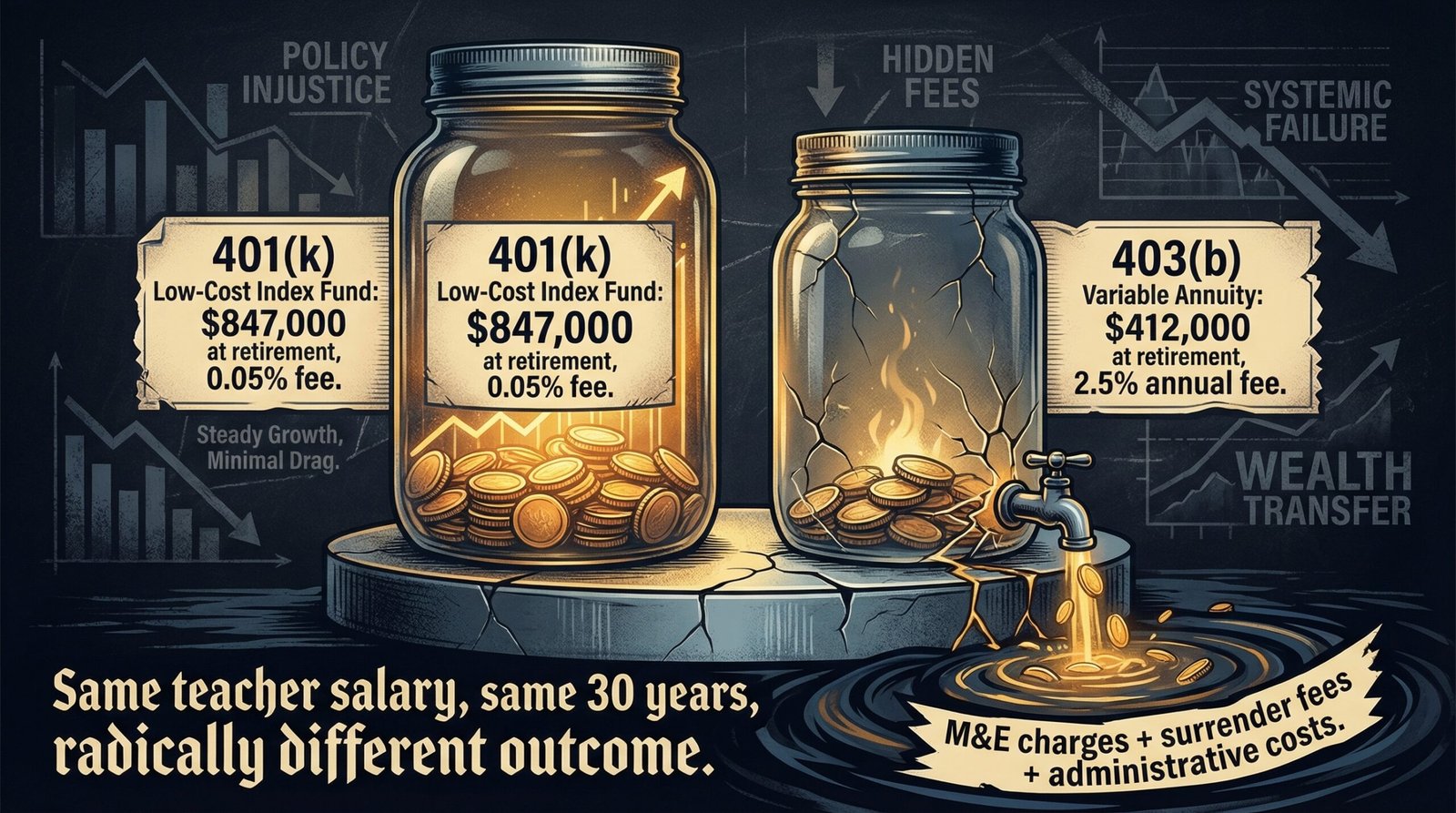

- A teacher saving $400/month for 30 years at 7% returns in a 2.5% fee plan retires with roughly $412,000. The same teacher in a 0.05% fee plan retires with $847,000. The $435,000 difference was extracted by insurance companies — legally.

- In July 2022, the SEC charged Equitable Financial Life Insurance Company with fraud for providing misleading account statements to approximately 1.4 million variable annuity holders, most of them teachers, and ordered a $50 million settlement.

- In August 2020, the SEC charged VALIC Financial Advisors with failing to disclose undisclosed conflicts of interest when advising teachers on 403(b) plans — including payments received for steering participants toward higher-fee products.

- The DOL found violations in 70% of ERISA 403(b) enforcement investigations between 2010 and 2021 — and non-ERISA plans, which cover most K-12 teachers, received essentially no federal enforcement scrutiny.

- Variable annuity surrender charges typically start at 8% of account value, declining over 7–10 years — creating a financial lock-in that prevents teachers from switching to better plans even after they identify the problem.

- The Biden administration’s 2024 DOL Retirement Security Rule would have extended fiduciary duty to most 403(b) advisors. The Trump administration removed it from the Code of Federal Regulations in 2025. The 403(b) INVEST Act, which would allow lower-cost collective investment trust options in 403(b) plans, passed the House but stalled in the Senate.

- An estimated 85.1% of eligible 403(b) participants were actively contributing in 2024 — suggesting most affected workers are saving diligently into plans designed to extract maximum fees from that diligence.

What Is a 403(b) Plan — and Who Is Stuck With One?

The 403(b) plan was created in 1958 under Section 403(b) of the Internal Revenue Code, originally as a tax-sheltered annuity (TSA) program for public school teachers and employees of 501(c)(3) nonprofit organizations. Unlike the 401(k), which was created by accident in 1978 (as we detailed in our analysis of how the 401(k) replaced pensions), the 403(b) was deliberately designed as an annuity vehicle — which is why insurance companies have dominated the market since inception and why the fee structures that would be unacceptable in a 401(k) environment have persisted for decades in the 403(b) world.

Today, 403(b) plans cover approximately 14.5 million American workers, according to the American Retirement Association. The IRS description is deceptively simple: a tax-deferred retirement plan offered by public schools and 501(c)(3) organizations. The reality is considerably more complex and considerably worse for participants. The plan types span three categories: annuity contracts issued by insurance companies (the majority, historically), mutual fund accounts held through custodial arrangements, and retirement income accounts for church employees. For most K-12 public school teachers, the default enrollment option is a variable annuity through one of several insurance company vendors approved by their school district — and the problems start there.

The workers covered include public school teachers (the largest group), nurses and hospital staff at nonprofit health systems, university employees, social workers, employees of charitable organizations, and staff at religious institutions. These are not high earners gaming the tax code with sophisticated financial instruments. The median teacher salary in the United States was approximately $66,000 in 2024. The median nonprofit worker earns less. These are people who chose careers in education, healthcare, and public service — and they have been systematically placed in retirement vehicles designed to extract the maximum possible fees from the minimum possible financial sophistication. Related: the broader Millennial retirement savings crisis, how Wall Street extracts $50 billion per year from 401(k) plans, and why pensions disappeared in the first place.

The Fee Math Nobody Shows You: How 1–2.5% a Year Destroys Half Your Retirement

The compounding damage of high annual fees is one of finance’s most underappreciated mathematical realities, and the 403(b) market has exploited that comprehension gap for 65 years. Here is the core math. Start with a teacher who contributes $400 per month to a 403(b) plan over a 30-year career, assumes a 7% gross annual market return, and retires at 65.

In a low-cost index fund with a 0.05% annual expense ratio (achievable today through Vanguard, Fidelity, or Schwab in any ERISA-covered plan), that teacher retires with approximately $847,000. In a typical 403(b) variable annuity with a 2.5% total annual cost — combining the mortality and expense (M&E) fee of ~1.25%, the underlying fund expense ratio of ~0.75%, and the administrative charge of ~0.50% — the same teacher retires with approximately $412,000. The $435,000 difference is the fee drag, compounded over 30 years. It is not a performance difference. It is not market timing. It is purely the cost of being enrolled in an insurance-company product that the teacher’s employer selected, possibly in exchange for a referral payment, without any legal obligation to consider whether it was appropriate.

The DOL’s general guidance on fee impact states that each additional 1% in annual fees reduces a worker’s final balance by roughly 17% over a 20-year period. Over 30 years, the compounding impact is more severe. A teacher paying 2.5% annually instead of 0.05% is losing approximately 51% of their final balance to fees — in a career that will never be compensated by high salaries, stock options, or private equity returns. This is what makes the 403(b) fee problem qualitatively different from the hidden 401(k) fee problem we’ve covered previously: 401(k) participants at least have ERISA fiduciaries legally obligated to monitor and minimize costs. Most 403(b) participants have no such protection.

The average teacher pays 10–50x more in annual retirement account fees than the average corporate employee. Not because insurance is more expensive to provide. Because nobody is legally required to stop it.

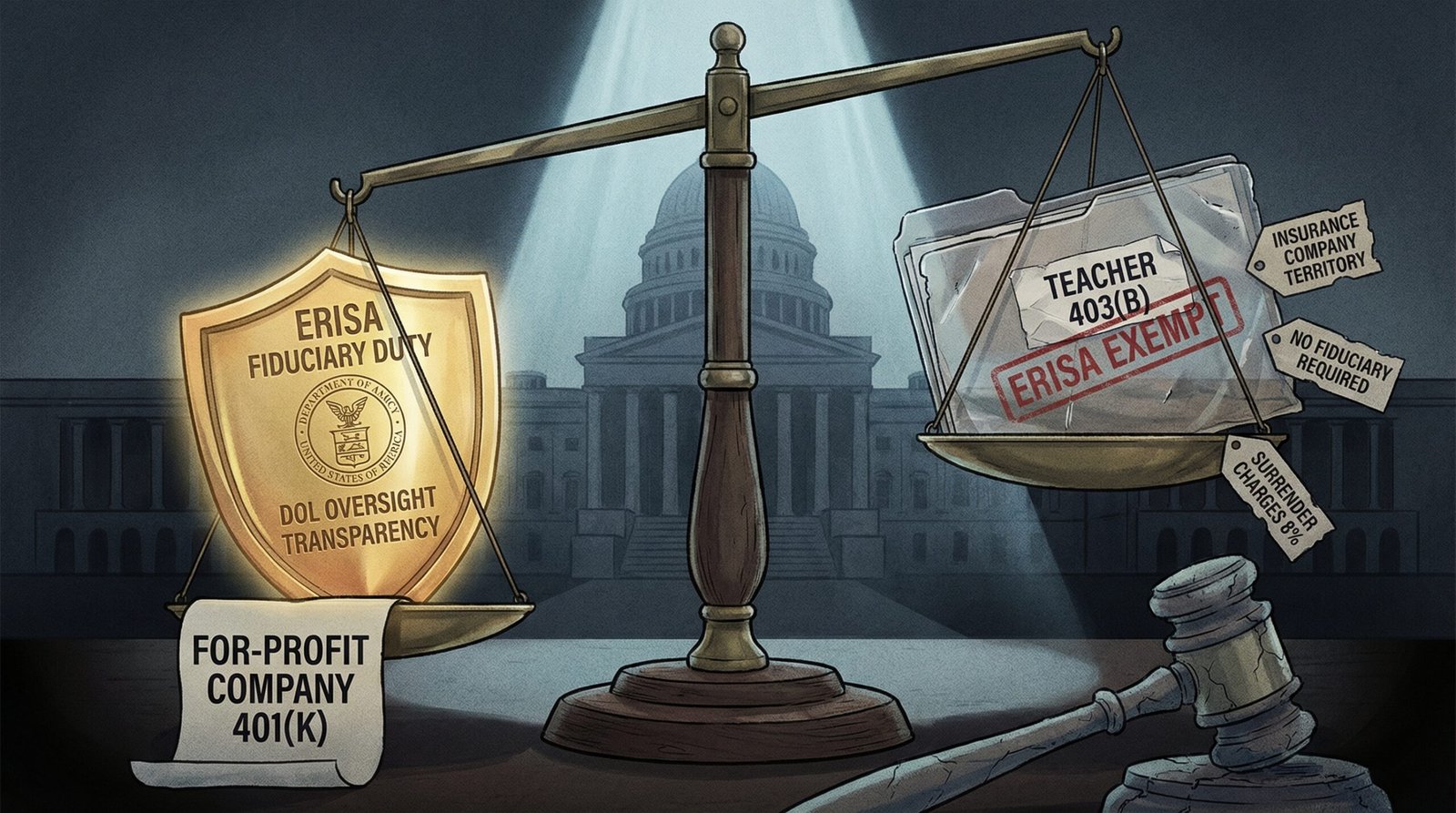

The ERISA Exemption: Why the Law That Protects Private Sector Workers Explicitly Excludes Most Teachers

The Employee Retirement Income Security Act of 1974 is the federal law that governs most private-sector retirement plans. It requires plan sponsors to act as fiduciaries — meaning they must act in the exclusive interest of plan participants, diversify investments to minimize risk, pay only reasonable fees, and follow the plan document. It mandates disclosure of plan fees, requires annual reporting, and gives participants the right to sue for fiduciary breaches. It is, imperfectly but meaningfully, a floor of accountability for retirement savings.

The 403(b) plans covering most K-12 public school teachers are explicitly exempt from ERISA Title I. The exemption exists because government employers — states, counties, and school districts — are excluded from ERISA’s coverage as a matter of constitutional federalism. Church plans received a separate exemption through decades of lobbying by religious organizations. The practical result: approximately half of the roughly $1 trillion in 403(b) assets is covered by ERISA. The other half — primarily the plans serving public school teachers, the largest single group of 403(b) participants — is not.

What does the absence of ERISA protection actually mean? It means the school district that selects the plan vendor is not legally required to conduct a prudent search for the best options. It means the financial advisors who enroll teachers in variable annuities are not legally required to recommend the product that is best for the teacher — only a product that is “suitable,” a much weaker standard that historically has meant “a product that is arguably appropriate for someone in this general situation.” It means fee disclosures are governed by state insurance law rather than federal retirement law, and state insurance regulators have historically been far less aggressive than the DOL in pursuing fee abuse. And it means there is no federal private right of action: a teacher who has been steered into an inappropriate high-fee annuity cannot sue under ERISA. Their only remedy is state consumer protection law, which is vastly less powerful.

The DOL’s Employee Benefits Security Administration, which enforces ERISA, conducted 454 enforcement investigations of 403(b) plans between 2010 and 2021 — the plans that are covered by ERISA. It found violations in 70% of those investigations. This is the enforcement rate for plans that are supposed to have mandatory protections. The non-ERISA plans — most teachers’ plans — receive essentially no equivalent federal oversight. The regulatory void is not a bug. It was built in.

The Vendor Selection Racket: How School Districts and Unions Sold Out Teachers to Insurance Companies

The 403(b) vendor ecosystem has a structural conflict of interest baked into its design. In a typical 401(k) plan, the plan sponsor (the employer) selects a limited menu of investment options and is legally required under ERISA to conduct a prudent selection process, monitor fees, and remove options that are not in participants’ interests. In a non-ERISA 403(b) plan, the school district often maintains an “open” vendor arrangement — allowing any insurance company or financial services firm that meets minimal administrative criteria to participate as an approved provider. Teachers then select from the approved list, frequently guided by vendor representatives who show up at schools, call teachers during planning periods, or partner with union affiliates.

This open-vendor model creates the conditions for the referral kickback problem. Insurance companies pay school districts, teacher organizations, or affiliated entities for the right to be listed as a preferred or approved vendor — fees that are rarely disclosed to participants as conflicts of interest. The SEC’s 2019–2022 enforcement sweep of the K-12 403(b) market documented this pattern systematically. In multiple cases, union-affiliated entities presented themselves as independent endorsers of specific 403(b) vendors while receiving undisclosed compensation from those same vendors for participant referrals. Teachers were selecting financial advisors they believed had been independently vetted on their behalf, when in fact the “vetting” was a paid referral arrangement.

States have handled the vendor multiplicity problem differently and inconsistently. California and Texas — the two largest states by teacher population — require school districts to allow any vendor an employee requests, creating lists of dozens or even hundreds of approved providers with no quality curation. Other states have moved toward consolidated vendor lists with some due diligence requirements. The result is a fragmented landscape where a teacher in one state might have access to a well-curated plan with low-cost index fund options, while a teacher in the neighboring state’s district is funneled into a variable annuity with a 3% total expense ratio and an 8% surrender charge. The retirement outcome difference between those two teachers, all else equal, can exceed $400,000 over a career — determined entirely by geography and employer administrative practices, not by the teacher’s financial choices or contributions.

SEC Enforcement: $50 Million, 1.4 Million Teachers Harmed, and the Fraud Just Kept Going

The SEC’s multi-year enforcement sweep of the K-12 403(b) market, launched in 2019, produced some of the most damning evidence of systematic retirement savings exploitation in recent regulatory history — and demonstrated how little enforcement changes structural incentives when the underlying regulatory framework remains intact.

The landmark action came in July 2022, when the SEC charged Equitable Financial Life Insurance Company — formerly AXA Equitable Life — with providing misleading account statements to approximately 1.4 million variable annuity account holders, the majority of them public school teachers and support staff. According to the SEC’s order, Equitable’s statements materially understated the fees being charged, creating a false impression of investment performance and making it impossible for participants to accurately assess the cost of remaining in their plans. Equitable agreed to pay $50 million to harmed investors and to take remedial measures to improve its disclosures.

Two years earlier, in August 2020, the SEC charged VALIC Financial Advisors — then a subsidiary of AIG — in two separate enforcement actions for failing to disclose to teachers that it received compensation from affiliated mutual funds it recommended, and for maintaining an arrangement with a Florida school district that paid VALIC for exclusive access to school premises in exchange for steering teachers toward VALIC products. Neither compensation arrangement was disclosed to participants. VALIC settled for approximately $40 million total across the two actions.

These enforcement actions were significant — but they were also illustrative of the limits of securities regulation as a remedy for a structural problem. The SEC can fine companies for misleading disclosures. It cannot require school districts to offer better plans. It cannot extend ERISA’s fiduciary standard to government employers. It cannot prohibit the sale of high-fee variable annuities to teachers — only require that the fees be disclosed accurately, a standard that was apparently too high for at least two of the market’s largest operators. The revolving door between the insurance industry and federal financial regulators has historically limited the aggressiveness of enforcement in this space.

Surrender Charges: The Lock-In Penalty That Prevents Escape From a Bad Plan

Even when a teacher becomes aware that their 403(b) variable annuity is extracting 2–3% per year in fees — through a financial literacy workshop, a conversation with a fee-only financial planner, or a family member who works in finance — they often discover they cannot simply transfer their account to a better option. The variable annuity product they enrolled in almost certainly includes a surrender charge provision: a penalty for withdrawing or transferring funds before a specified holding period expires.

Surrender charges in variable annuities are typically structured as a declining schedule — 8% in year one, declining by approximately 1% per year, reaching zero after 7–10 years. This means a teacher who has been in a plan for three years and wants to transfer $100,000 to a lower-cost option faces a penalty of approximately $5,000–6,000 out of pocket for the privilege of making a better financial decision. The teacher who has been in the plan for eight years can leave free, but has spent the intervening years paying 2–3% annually on a growing account balance — potentially tens of thousands of dollars in excess fees during the lock-in period alone.

Surrender charges serve no legitimate retirement savings purpose. They do not protect the participant. They do not fund any guaranteed benefit. They exist to ensure that once an insurance company has enrolled a participant, that participant cannot defect to a competitor without paying a significant financial penalty — a penalty that goes directly to the insurer’s bottom line. The surrender charge is, in economic terms, an exit tax on rational behavior. The teacher who recognizes they are in a bad plan and tries to leave is punished. The teacher who stays and pays 2.5% for 30 years is not. The product is engineered to extract maximum revenue from financial inertia, which is one of the most reliable features of human behavior with respect to retirement savings.

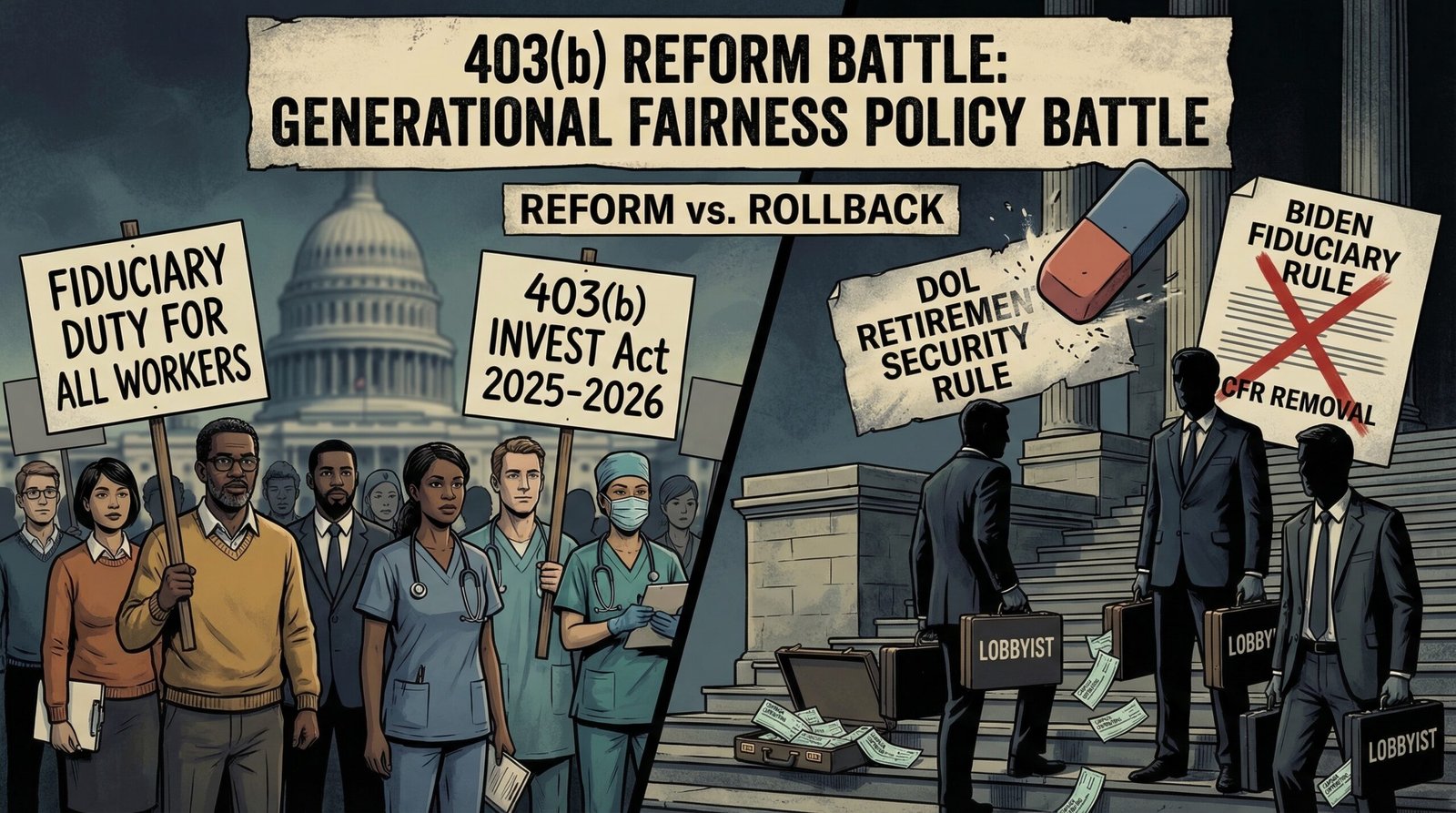

Reform Attempted, Reform Killed: The DOL Fiduciary Rule, the 403(b) INVEST Act, and the Lobby That Beat Them Both

The political history of 403(b) reform is a case study in how the insurance industry has used its lobbying infrastructure to defeat every meaningful attempt to extend fiduciary accountability to the plans covering 14.5 million workers. Each reform attempt follows a pattern: a regulatory agency or Congress identifies the problem, proposes a fix, faces a coordinated industry campaign emphasizing compliance costs and disruption to existing relationships, and ultimately produces a watered-down or abandoned reform. The participants whose interests were supposed to be protected receive no change in outcome.

The most recent example is the Biden administration’s 2024 Retirement Security Rule, issued by the DOL. The rule would have significantly expanded the definition of “investment advice fiduciary” under ERISA, requiring anyone providing rollover recommendations, plan selection advice, or investment recommendations to retirement accounts — including 403(b) advisors — to act in the client’s best interest rather than their own. Industry groups representing insurance companies and broker-dealers challenged the rule in court and lobbied Congress aggressively. The Trump administration, following through on campaign commitments to the financial services industry, removed the 2024 Retirement Security Rule from the Code of Federal Regulations in 2025, reverting to the pre-Biden “investment advice” standard.

On the legislative side, the 403(b) INVEST Act would address a specific structural disadvantage: 403(b) plans are currently prohibited from investing in collective investment trusts (CITs) — pooled investment vehicles that offer lower costs than retail mutual funds and are available in virtually every 401(k) plan. CITs exist at lower cost because they don’t carry the marketing, distribution, and 12b-1 fee structures of retail mutual funds. The 403(b) INVEST Act would allow 403(b) plans to use CITs, potentially reducing fees for millions of participants. The bill passed the House as part of broader legislative packages but has repeatedly stalled in the Senate. The insurance industry, which profits from retail mutual fund fees within 403(b) plans, has lobbied against the bill. The mutual fund industry has been ambivalent. The workers whose fees would be reduced are not a significant campaign finance constituency.

SECURE 2.0 (2022) did make some incremental improvements to 403(b) plans — including allowing hardship withdrawals of earnings, improving automatic enrollment provisions for ERISA 403(b) plans, and expanding catch-up contribution provisions. But SECURE 2.0 left the ERISA exemption for government 403(b) plans untouched, did not address the vendor selection problem, and made no structural change to the variable annuity fee extraction that represents the core of the problem. As we detailed in our analysis of AARP’s lobbying conflicts in retirement policy and the broader revolving door lobbying machine, incremental improvements to retirement savings law consistently stop well short of structural change when insurance industry revenue is at stake.

The Counter-Argument: Not Every 403(b) Is a Trap — and Annuities Are Not Always the Enemy

The 403(b) fee problem is real and well-documented. The counterarguments also deserve fair treatment.

Many ERISA 403(b) plans are well-run: Large universities, major hospital systems, and substantial nonprofits often maintain ERISA-covered 403(b) plans with employer matches, fiduciary oversight, and investment menus that include low-cost index fund options comparable to the best 401(k) plans. A teacher at a major private university is likely in a plan that is qualitatively different from a teacher at a small rural school district. The problem is not the 403(b) tax structure — it is the regulatory two-tier system that leaves most government employers without fiduciary accountability.

Annuities can provide legitimate value: The core product at the center of the fee problem — the variable annuity — is not inherently fraudulent. For a teacher who lacks a defined benefit pension, who may live to 90, and who fears outliving their savings, a guaranteed lifetime income product has genuine value. The problem is that the fee structures historically embedded in 403(b) annuity products are far higher than necessary to provide that guarantee, and the fee drag they impose over a 30-year accumulation phase often exceeds any income guarantee benefit received in retirement. A low-cost annuity — the kind increasingly available through direct-to-consumer platforms — can be a legitimate retirement planning tool. A 2.5% total annual fee variable annuity with an 8% surrender charge is not.

The landscape is improving at the margin: The SEC enforcement actions of 2019–2022 have produced more careful disclosure practices from the largest providers. Some school districts have moved to consolidated vendor lists with genuine quality screening. The 403bwise advocacy community founded by Dan Otter has significantly increased teacher financial literacy about plan fees. SECURE 2.0’s incremental improvements have helped some plan participants. These changes do not fix the structural problem, but they represent genuine if insufficient progress.

What Can Teachers and Nonprofit Workers Actually Do Right Now?

Given that structural reform has been repeatedly blocked, the practical question is what an individual teacher or nonprofit worker can do today. Several steps can meaningfully reduce the fee extraction from their existing plan.

1. Find out your actual total annual fees. Request a prospectus or fee disclosure from your plan provider and calculate the total expense ratio including the M&E fee, fund expenses, and administrative charges. The 403bwise database (403bwise.org) and the ASPPA’s plan data resources can help compare your plan’s costs against alternatives available in your district.

2. Check whether your district has a low-cost vendor option. Many districts with multi-vendor arrangements include at least one lower-cost option — often a credit union, Fidelity, or TIAA mutual fund option — buried in the approved vendor list alongside insurance company products. TIAA, which serves many higher education and nonprofit employees, offers both annuity and mutual fund options, with the mutual fund options being significantly less expensive than variable annuities.

3. If you have a pension, consider 403(b) contributions strategically. Many K-12 teachers have defined benefit pension plans as their primary retirement vehicle. If your pension provides adequate retirement income, accumulating retirement savings in a 457(b) plan (if your district offers one) may be preferable to a 403(b) with high fees — 457(b) plans have different early withdrawal rules and are often administered by the same vendors, but can be worth comparing.

4. After surrender charges expire, transfer to low-cost options. If you are in a variable annuity with surrender charges, calculate when the surrender period ends and plan an exchange or transfer at that point. A 1035 exchange allows transfer of annuity contracts without triggering immediate taxation, potentially allowing migration to a lower-cost annuity or a mutual fund custodial account.

5. Contact your union about vendor practices. If your teachers union affiliate receives referral compensation from 403(b) vendors and does not disclose this, that is a conflict of interest that members can raise through union governance processes. Several state NEA and AFT affiliates have faced internal pressure on this issue and have changed their vendor arrangement disclosures as a result.

FAQ: 403(b) Retirement Plans

What is the difference between a 403(b) and a 401(k)?

Both are tax-deferred employer-sponsored retirement savings accounts with the same annual contribution limits ($23,500 in 2025, $31,000 for those 50 and older). The key differences: 403(b) plans are available only to employees of public schools, nonprofits, and certain tax-exempt organizations, while 401(k) plans are for private-sector companies. Most government-employer 403(b) plans (covering K-12 teachers) are exempt from ERISA’s fiduciary duty requirements, which means plan sponsors are not legally required to minimize fees or act in participants’ best interest. 401(k) plans are subject to ERISA and must have a fiduciary who bears legal responsibility for investment selection and fee monitoring. This regulatory difference is the primary reason 403(b) plans have historically been loaded with higher-cost variable annuity products.

Are 403(b) plans bad for teachers?

Not inherently — the tax deferral benefit is real and the ability to save for retirement through payroll deduction is valuable. The problem is that many 403(b) plans, particularly those offered through school districts without ERISA oversight, are dominated by variable annuity products with total fees of 1–3% per year. At that fee level, a teacher can lose $200,000–$400,000 in lifetime retirement wealth compared to an equivalent low-cost index fund option. Teachers in ERISA-covered 403(b) plans at large universities and nonprofits often have access to well-curated, low-cost investment menus and are generally not subject to the same fee exploitation. The quality of your 403(b) depends heavily on your employer’s plan administration and the applicable regulatory framework.

What is a 403(b) surrender charge, and how does it work?

A surrender charge is a penalty assessed when you withdraw or transfer funds from a variable annuity contract before a specified holding period expires. Surrender charges in 403(b) variable annuities typically start at 7–8% of the account value in year one and decline by roughly 1% per year, reaching zero after 7–10 years. A teacher with $100,000 in a variable annuity in year three who wants to transfer to a lower-cost option faces a surrender charge of approximately $5,000–6,000. The surrender charge serves no participant-protective purpose — it exists to deter participants from leaving expensive products and flows directly to the insurance company as revenue.

What should I look for in a 403(b) plan?

Prioritize plans with total annual expense ratios below 0.50%, with 0.10% or below achievable in the best plans. Look for access to index funds tracking the S&P 500, total bond market, and international equity markets. Avoid variable annuity contracts with mortality and expense fees, unless you have a specific need for guaranteed lifetime income and have exhausted lower-cost guaranteed income options. Check whether surrender charges apply and how long the surrender period runs. If your district offers multiple vendor options, compare them using resources like 403bwise.org before enrolling. If your district offers a 457(b) plan alongside the 403(b), compare the fee structures of both before defaulting to the 403(b).

Sources & Methodology

Data sources used in this article:

- IRS — IRC 403(b) Tax-Sheltered Annuity Plans — plan definition, eligible employers, basic structure

- Empower / American Retirement Association — 14.5 million American workers in nonprofit sector use 403(b) plans; average balance growth 15% 2022–2024

- SEC — Equitable Financial $50 Million Settlement, July 2022 — 1.4 million account holders, misleading fee statements, public school teachers and staff

- SEC — VALIC Financial Advisors Enforcement Action, August 2020 — undisclosed conflicts of interest, teacher 403(b) plans, exclusive access arrangement

- ASPPA — Equitable $50 Million Penalty Analysis

- 401(k) Specialist — 403(b) Plan Participation Jumps to 85.1% in 2024

- PLANSPONSOR — 2025 403(b) Market Survey — plan size distribution, assets under management

- Great Gray Trust — 403(b) INVEST Act Passes House — CIT access, legislative history, Senate stall

- Ascensus — DOL Removes 2024 Retirement Security Rule from CFR, 2025

- DOL Employee Benefits Security Administration — 454 enforcement investigations of ERISA 403(b) plans 2010–2021; 70% violation rate

- DOL guidance — each 1% additional annual fee reduces final retirement balance by approximately 17% over 20 years

- Department of Education / BLS — median teacher salary ~$66,000, 2024

- Variable annuity fee structure analysis: M&E fees 1.25%, fund expense ratio 0.75%, administrative charge 0.50% = 2.50% total annual cost (industry average range)

- Fee drag modeling: $400/month contributions, 7% gross return, 30-year career — 0.05% fee = $847,000 terminal value; 2.50% fee = $412,000 terminal value; $435,000 fee drag (author calculation)

Methodology: Enrollment and participation statistics from American Retirement Association and Empower research. SEC enforcement data from SEC EDGAR press releases. Fee impact calculations model a $400/month contribution over 360 months at 7% gross annual return compounded monthly, reduced by the applicable fee drag annually, using a standard compound interest formula. The DOL’s 17% per 1% fee rule-of-thumb is approximate and based on a 20-year horizon; the 30-year calculation is extrapolated and will vary by contribution pattern and return sequence. Plan structure and ERISA applicability analysis based on IRS and DOL guidance, ASPPA resources, and ERISA legal commentary. Legislative status from congressional records and industry publications through March 2026.