ByAiden

ByAiden

Semiconductor Shortage America: How 30 Years of Offshoring Chips Spiked Your Car Payment by $10,000

Share your love

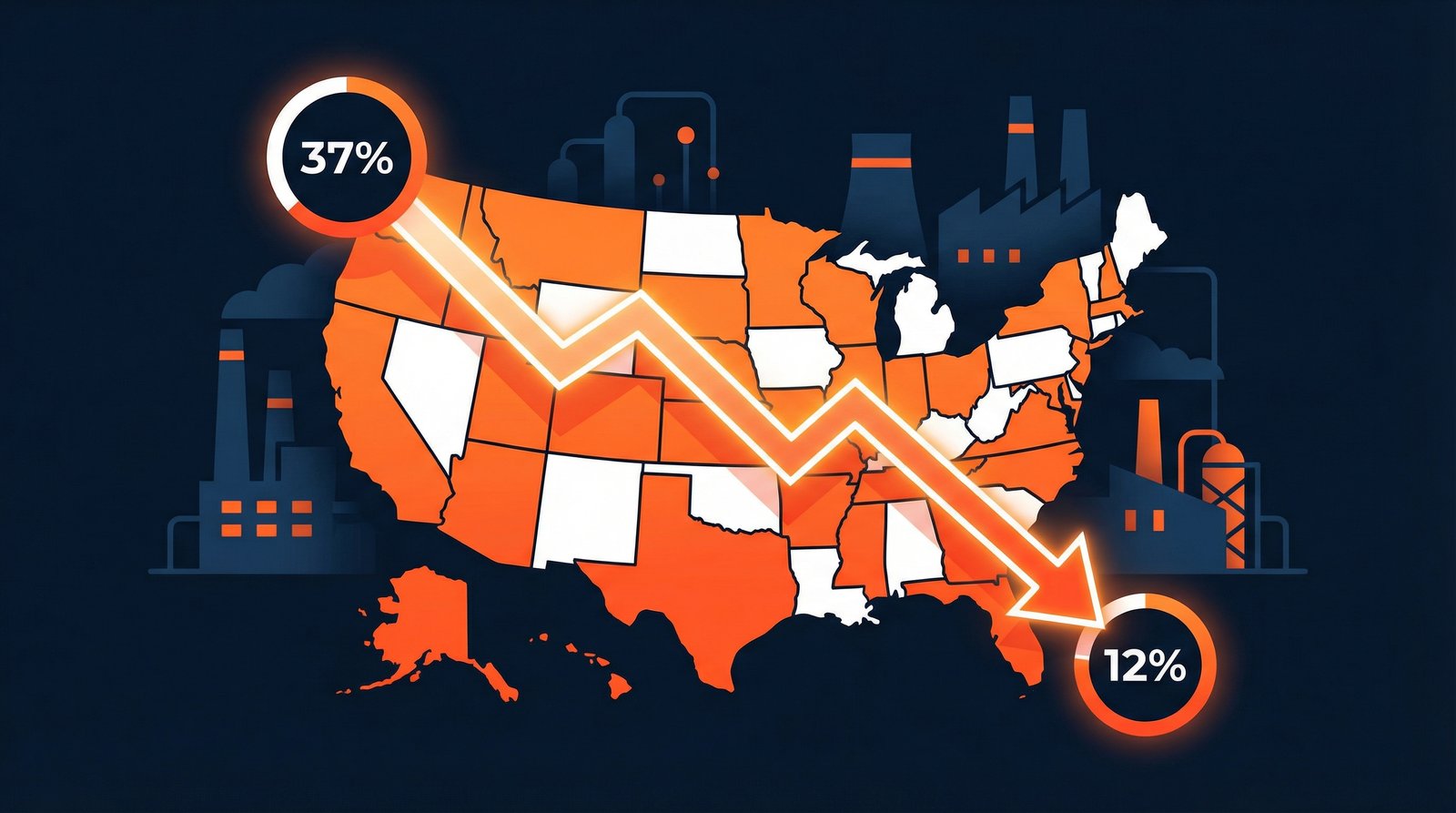

The semiconductor shortage in America cost the U.S. economy an estimated $240 billion in 2021 alone, eliminated 11 million vehicle builds, and sent used car prices up 40% — all because bipartisan policymakers spent 30 years cheerfully handing chip manufacturing to Asia in the name of short-term efficiency. America held 37% of global semiconductor manufacturing capacity in 1990. Today that number sits at 12%. The bill for that choice arrived in your car payment, your laptop price, and your refrigerator delivery date.

Key Takeaways

• America’s share of global chip manufacturing collapsed from 37% (1990) to 12% today — a 25-percentage-point freefall driven by deliberate policy choices, not market forces alone.

• The 2020–2023 chip shortage cost the U.S. economy $240 billion, eliminated production of 11 million vehicles, and sent used car prices up 30–40%.

• 90% of the world’s most advanced chips are made by a single company — TSMC — in Taiwan, 100 miles from China’s coast.

• The CHIPS Act committed $52.7 billion to fix this. Key fab projects are already years behind schedule.

• The infrastructure crisis, skilled trades shortage, and chip dependency crisis all share the same root cause: a generation of leaders who chose quarterly earnings over national resilience.

What Is the Semiconductor Shortage in America?

A semiconductor — a microchip — is the silicon brain inside virtually everything modern: your car, your phone, your HVAC system, your hospital’s MRI machine, the fighter jets your tax dollars buy. In 2020, pandemic-era demand shifts created a traffic jam in the global chip supply chain. Consumer electronics demand surged as people worked from home; automakers had canceled chip orders assuming a recession; and the entire industry discovered, all at once, that the world’s manufacturing capacity was concentrated in a handful of factories in East Asia that couldn’t pivot fast enough.

The result: 169 industries were affected by chip shortages. Semiconductor wait times hit 18 weeks in May 2021 — four weeks beyond the previous record. The U.S. economy absorbed a $240 billion hit in a single year. This wasn’t a black swan event. It was the entirely predictable outcome of a three-decade policy experiment in which America decided it didn’t need to make anything, it just needed to design things and let cheaper countries handle the manufacturing.

The same logic that offshored 3 million manufacturing jobs to China also offshored the fabs. When the supply chain snapped, ordinary Americans paid for it — not in abstract GDP statistics but in car loans that are now $150/month higher than they would have been in a functioning supply chain.

How Did America Lose 25 Points of Chip Manufacturing in 30 Years?

This wasn’t an accident. It was a series of choices, each individually defensible, collectively catastrophic.

The 1960s–80s: America Offshores Assembly, Then Loses Manufacturing Expertise

U.S. semiconductor companies began offshoring labor-intensive assembly operations to Southeast Asia in the 1960s. By the 1980s, Japan — guided by its Ministry of International Trade and Industry — executed a coordinated industrial policy that captured the DRAM (memory chip) market. The U.S. share of the global semiconductor market fell from a near-monopoly in the 1970s to 51% globally by 1982. Japan’s share climbed from 15% to 35% in the same period.

Meanwhile, U.S. companies invented the VCR — and then watched Toshiba manufacture it at scale. Ampex created the technology in 1970; financial constraints forced it to contract production to Toshiba; Toshiba learned the process, scaled it, and by the mid-1980s Japan produced 50 million VCRs annually while the U.S. produced functionally zero. The same dynamic played out in televisions, cameras, and consumer electronics broadly — all semiconductor-hungry products, all manufacturing transferred abroad. Every product that moved took chip-making expertise with it.

The 1990s: The U.S. Chose “Science Policy” Over Manufacturing Capacity

Facing Japanese competition, the U.S. government made a fateful choice: fund academic R&D rather than rebuild manufacturing capacity. The theory was elegant in a business school. Let America design chips; let Asia build them. Fabless design companies like Qualcomm and Nvidia would thrive while “foundry” companies like TSMC handled the dirty, capital-intensive fab work in Taiwan.

This created a “science policy” trap. Manufacturing expertise requires doing — you can’t separate semiconductor design knowledge from fabrication knowledge indefinitely. As fabs left, so did the engineers who knew how to run them, the supply chains that supported them, the technician workforce trained for them, and the institutional knowledge of process improvement. The U.S. retained design superiority but surrendered the manufacturing muscle that historically drove process innovation.

America’s share of global chip manufacturing fell from 37% in 1990 to roughly 12% today. The same CTE defunding that killed shop class also dried up the semiconductor technician pipeline. It’s almost like everything was connected.

By 2020: 83% of Global Fab Capacity Concentrated in East Asia

By the time COVID-19 hit, 83% of total global semiconductor manufacturing capacity resided in South Korea, Taiwan, China, and Japan. The U.S. — which invented the transistor, built the first integrated circuits, and created the semiconductor industry — accounted for 12% of global fab capacity but 48% of global chip sales. Americans were still the best designers on the planet. They just couldn’t make anything.

How Did the Chip Shortage Spike Your Car Payment?

The math here is simple and brutal. A modern vehicle contains between 1,000 and 3,000 semiconductor chips — managing everything from the engine control unit and transmission to the backup camera, Bluetooth, and airbag sensors. Automakers, unlike consumer electronics companies, had long operated on just-in-time inventory with minimal chip stockpiles. When COVID-19 demand collapsed in early 2020, automakers canceled chip orders. Semiconductor fabs, facing surging demand from consumer electronics, reallocated that capacity. When auto demand snapped back faster than expected, there were no chips.

The numbers are staggering:

- $210 billion in lost automotive industry revenue in 2021 (AlixPartners)

- 11 million vehicles not built due to chip shortages (S&P Global Mobility)

- Used car prices up 30–40% in 2021 — the CPI for used cars rose nearly 30% in the 12 months ending May 2021 (Federal Reserve Bank of Cleveland)

- Wholesale used car prices up nearly 40% through 2021 (CarEdge)

- New car prices 30% higher in 2024 than in 2020 — many buyers are still paying the shortage premium (AutoInsurance.com)

- Inventory fell from 3.6 million units in February 2020 to 1.5 million by May 2021

The average used car hit a record $28,000 at the peak. For a Millennial or Gen Z buyer financing a car at that price, the effective lifetime cost difference versus a $20,000 pre-shortage price — at prevailing 2022–2023 interest rates — runs to $10,000–$14,000 in additional spending over a 60-month loan. That’s not a rounding error. That’s a semester of community college, wiped out because a generation of policymakers decided cheap chip imports were fine and domestic manufacturing was a dinosaur.

The same generation already squeezed on rent, crushed by medical debt, and watching their student loan terms rewritten also got hit with a 40% car price spike because nobody bothered to maintain domestic chip production. The hits just don’t stop.

Why Is Taiwan a Single Point of Failure for the American Economy?

The geopolitical risk lurking behind the chip shortage is orders of magnitude more dangerous than a pandemic supply disruption. TSMC alone produces approximately 90% of the world’s most advanced semiconductors. Its fabs sit in Taiwan — 100 miles from mainland China. U.S. Treasury Secretary Scott Bessent has called Taiwan’s chip concentration a “single point of failure” for the global economy. He’s right, and the understatement is almost artistic.

A February 2026 NYT analysis spelled it out: if China invades Taiwan and cuts off chip exports to American companies, the U.S. tech industry and broader economy would be “crippled.” This isn’t a fringe scenario. It’s the central planning assumption of the U.S. military and intelligence community. Every AI data center, every defense system, every hospital network runs on chips that flow through a 100-mile strait where two nuclear-armed powers are in active strategic competition.

China’s own semiconductor production has grown rapidly. China-based firms made up 33% of global wafer production capacity for foundational chips in 2023, up from 19% in 2015. Beijing’s “Made in China 2025” industrial policy explicitly targets semiconductor self-sufficiency. While U.S. export controls have slowed China’s access to the most advanced chip-making tools, Beijing is closing the gap on legacy chip production — the category that matters most for military hardware, automotive, and industrial applications.

The same short-termism that blew up the banking system in 2008 created this geopolitical vulnerability. Efficiency über alles — until it isn’t.

The CHIPS Act: $52 Billion Later, Are We Fixed?

Congress passed the CHIPS and Science Act in 2022, appropriating $52.7 billion to rebuild domestic semiconductor manufacturing. The headline awards sound impressive:

- Intel: Up to $7.865 billion for four new fabs in Arizona and Ohio

- TSMC: Funding for Arizona fab expansion producing 3nm and 2nm chips

- Samsung: $6.4 billion for Taylor, Texas facility

- Micron: Funding for domestic memory chip fabs

Here’s the problem: Intel’s $28 billion fab is now scheduled to be operational by 2030 — five years behind the original estimate. TSMC’s Arizona fab has faced construction delays, cultural friction with local workforce standards, and cost overruns. Samsung’s Texas facility has been similarly delayed. The first CHIPS Act manufacturing award wasn’t even finalized until September 2024 — two years after the law passed.

Meanwhile, Trump in 2025 called the CHIPS program “horrible” and suggested scrapping it, spreading panic through an industry that had just committed billions in capital based on federal guarantees. Proposed semiconductor tariffs — a blanket 25% on chip imports — threatened to increase costs for U.S. manufacturers who depend on imported equipment and materials to build the very fabs the CHIPS Act was funding.

Even optimistically: U.S. manufacturing capacity is projected at roughly 14% of global share by 2032. The gap from 37% (1990) to 14% (2032 projection) took 40 years to create. The same pattern of structural kick-the-can that created the pension crisis is fully operational here. The CHIPS Act is a down payment. Whether future Congresses follow through is a different question — and given America’s track record on long-horizon infrastructure commitments, the answer is not obviously encouraging.

Counter-Argument: “The Free Market Made the Right Call”

The standard defense of the offshoring era goes like this: comparative advantage is real, semiconductor fabs are brutally capital-intensive, and the U.S. gained enormous economic value from the fabless model. Qualcomm, Nvidia, and Apple became trillion-dollar companies by designing chips and outsourcing manufacturing. The efficiencies created cheaper consumer electronics for everyone. TSMC’s scale enables process innovations that no single national fab program could replicate.

There’s something to this. TSMC is genuinely extraordinary — its yield rates, process development, and operational discipline are world-class. The fabless model did enable a U.S. design ecosystem that remains the global leader. If you measure success by stock market performance, the strategy worked brilliantly.

But this argument has three fatal flaws. First, it assumes the geopolitical risk is manageable — that Taiwan will remain stable indefinitely, that supply chains will always function. The 2020–2023 shortage demolished that assumption. Second, it confuses corporate profitability with national resilience. A system that maximizes Nvidia’s margins while leaving 330 million Americans one supply disruption away from a $240 billion economic catastrophe is not a well-designed system. Third — and this is the part that never appears in the free-market pitch — the cost of offshoring wasn’t shared equally. Corporate shareholders captured the efficiency gains. Ordinary Americans absorbed the car payment spike, the 18-week delivery wait, the $600 laptop that should have cost $400. Profits were privatized; supply chain risk was socialized. Classic.

FAQ: Semiconductor Shortage America

Is the semiconductor shortage over?

The acute 2020–2023 automotive chip shortage has largely resolved — S&P Global Mobility declared it “mostly over” for auto production by mid-2023. However, the structural vulnerability hasn’t changed. The U.S. still manufactures only 12% of global chips domestically. A new geopolitical shock, natural disaster in Taiwan, or renewed demand surge could recreate the same crisis. The shortage is over; the underlying problem is not.

Why did the chip shortage cause car prices to go up so much?

Modern vehicles contain 1,000–3,000 semiconductor chips. When chip supply collapsed in 2021, automakers couldn’t build cars — 11 million vehicles went unbuilt. Less supply, same demand: prices spiked. Used car prices rose 30–40% because buyers who couldn’t find new cars flooded the used market. New car prices jumped 12% in a single year. Many of those price increases have been sticky — new car prices in 2024 are still roughly 30% higher than in 2020.

What is the CHIPS Act and will it fix the semiconductor shortage?

The CHIPS and Science Act (2022) allocated $52.7 billion in federal subsidies to rebuild domestic chip manufacturing. Key recipients include Intel, TSMC’s Arizona expansion, Samsung in Texas, and Micron. It’s a necessary step — but major fab projects are already years behind schedule, and even full implementation would only bring U.S. manufacturing share to roughly 14% by 2032. It’s a down payment on a 40-year problem, not a solution.

Why does it matter that TSMC is in Taiwan?

TSMC produces roughly 90% of the world’s most advanced semiconductors from facilities in Taiwan, 100 miles from mainland China. If China were to invade Taiwan or create a naval blockade, the supply of cutting-edge chips to American tech companies, defense contractors, automakers, and hospitals could be disrupted or severed. U.S. Treasury Secretary Bessent described this as a “single point of failure” for the global economy. The entire AI boom, every defense system, and most modern infrastructure depends on chips flowing through one extremely contested strait.

Sources & Methodology

Sources & Methodology: Manufacturing share data from the Semiconductor Industry Association (SIA) State of the Industry Report 2021 and 2025, the Center for Strategic and International Studies (CSIS), Georgetown CSET, and Visual Capitalist/SIA 1990–2032 production data. Economic cost estimates from CFR Education ($240B figure), Cleveland Federal Reserve Economic Commentary (2021), AlixPartners, and S&P Global Mobility. Automotive price data from CarEdge, AutoInsurance.com, and NerdWallet. CHIPS Act award data from SIA Chip Supply Chain Investments tracker, Reuters, and NGA CHIPS Act Implementation Resources. Taiwan risk analysis from NYT (Feb 24, 2026), U.S. Treasury Secretary Bessent public statements, and Kpler supply chain analysis. China production growth from U.S.-China Economic and Security Review Commission (USCC) Made in China 2025 report. Offshoring history from Employ America industrial policy analysis and UC Berkeley/eScholarship semiconductor offshoring research.