ByAiden

ByAiden

The Insulin Price Crisis: How America Turned a $21 Vial Into a $332 Death Sentence

Share your love

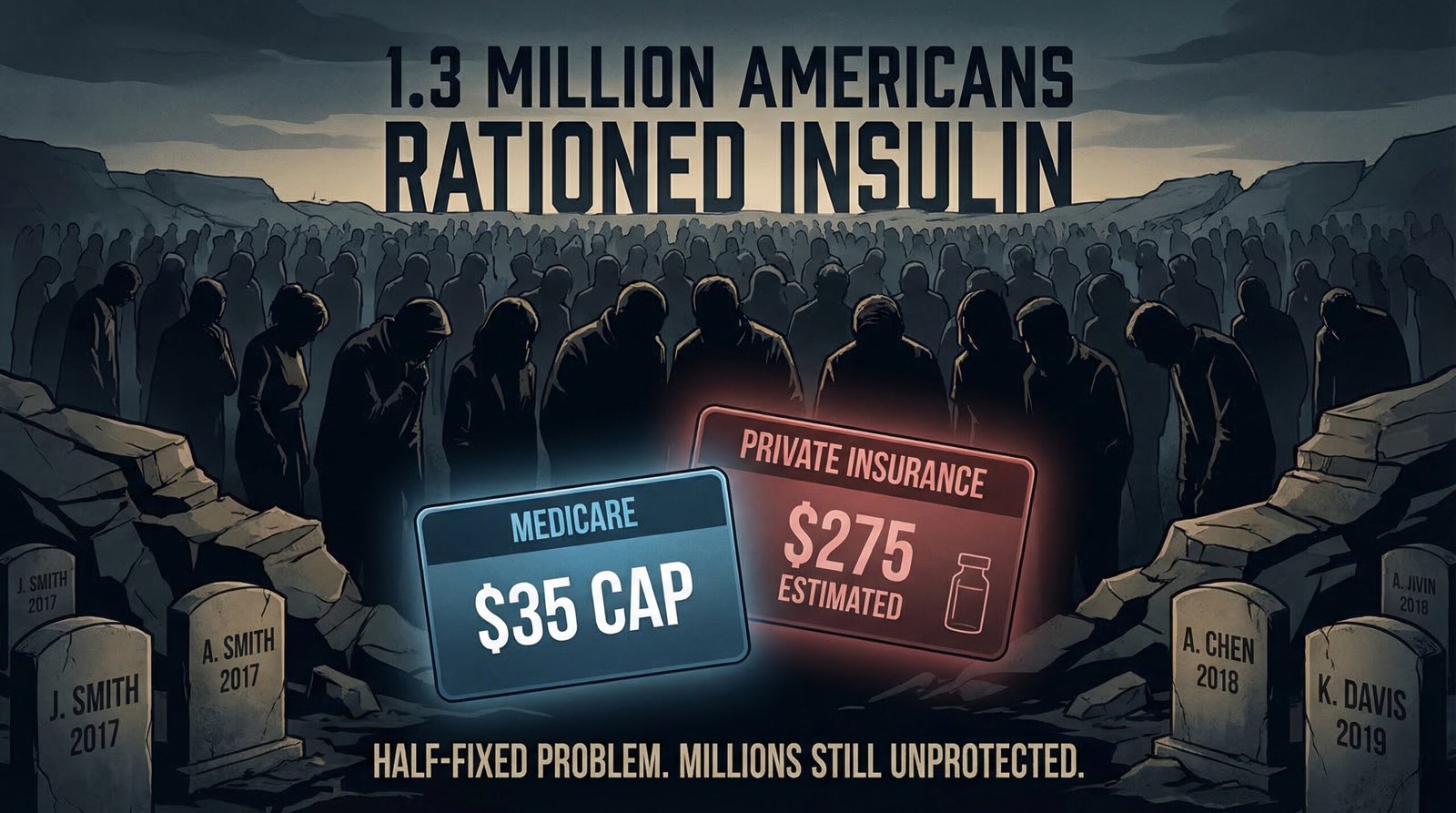

The insulin price crisis in America is the story of a century-old, off-patent medication — whose original inventors refused to patent it in 1923 because they believed profiting from a life-saving drug was unethical — being transformed into a financial extraction machine. A vial of Humalog that cost $21 in 1996 cost $332 in 2019, a 1,200% increase with no change in the underlying molecule. The United States pays roughly nine times more for insulin than 33 comparable high-income nations. In the peak years of the crisis, 1.3 million Americans rationed insulin due to cost, and at least 13 documented deaths from insulin rationing occurred between 2017 and 2019. The Inflation Reduction Act of 2022 capped Medicare insulin costs at $35 per month — but the commercial insurance market remained largely unreformed. As of 2026, an estimated 25–30% of Americans with type 1 diabetes still report rationing or skipping insulin.

Key Takeaways

- Insulin was discovered in 1921 and its inventors — Frederick Banting, Charles Best, and James Collip — sold the patent to the University of Toronto for $1, believing it was unethical to profit from a life-saving medication. A century later, three corporations control 90% of the U.S. insulin market and a vial that costs $8–10 to make and sell in other wealthy nations costs $250–$332 in America.

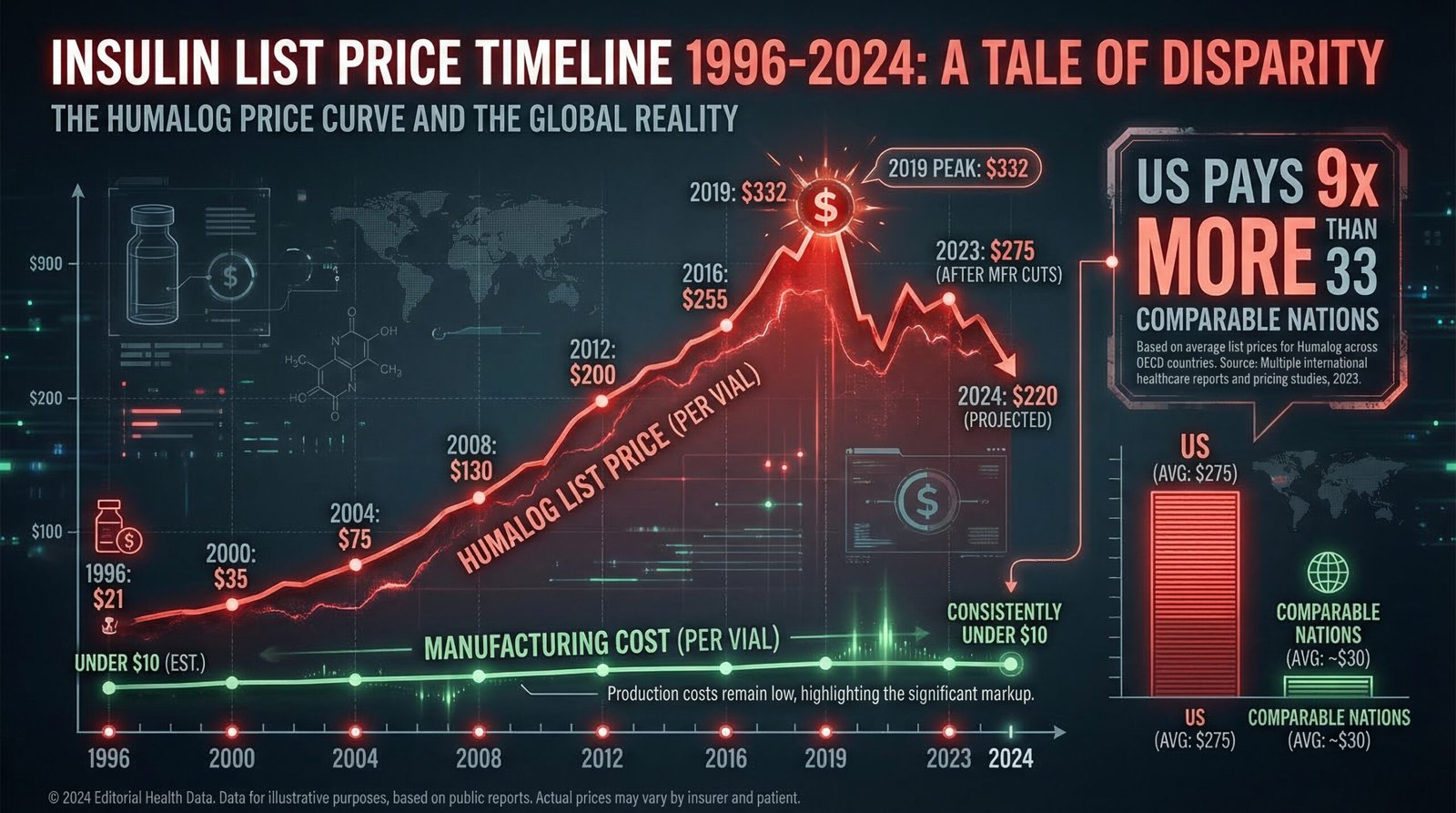

- Humalog (Eli Lilly) launched in 1996 at $20.82 per vial. By 2019, the list price was $332 — a 1,200% increase. Between 1996 and 2006 alone, insulin prices increased by 700%. The molecule itself did not change. The cost to manufacture it did not meaningfully increase. The price was raised because it could be.

- The U.S. pays approximately nine times more for insulin than 33 comparable high-income nations, according to RAND and ASPE research. The majority of those countries price insulin at $8–10 per vial. Type 1 diabetics in America requiring 3–6 vials per month face potential costs of $750–$1,980 monthly at list price before insurance.

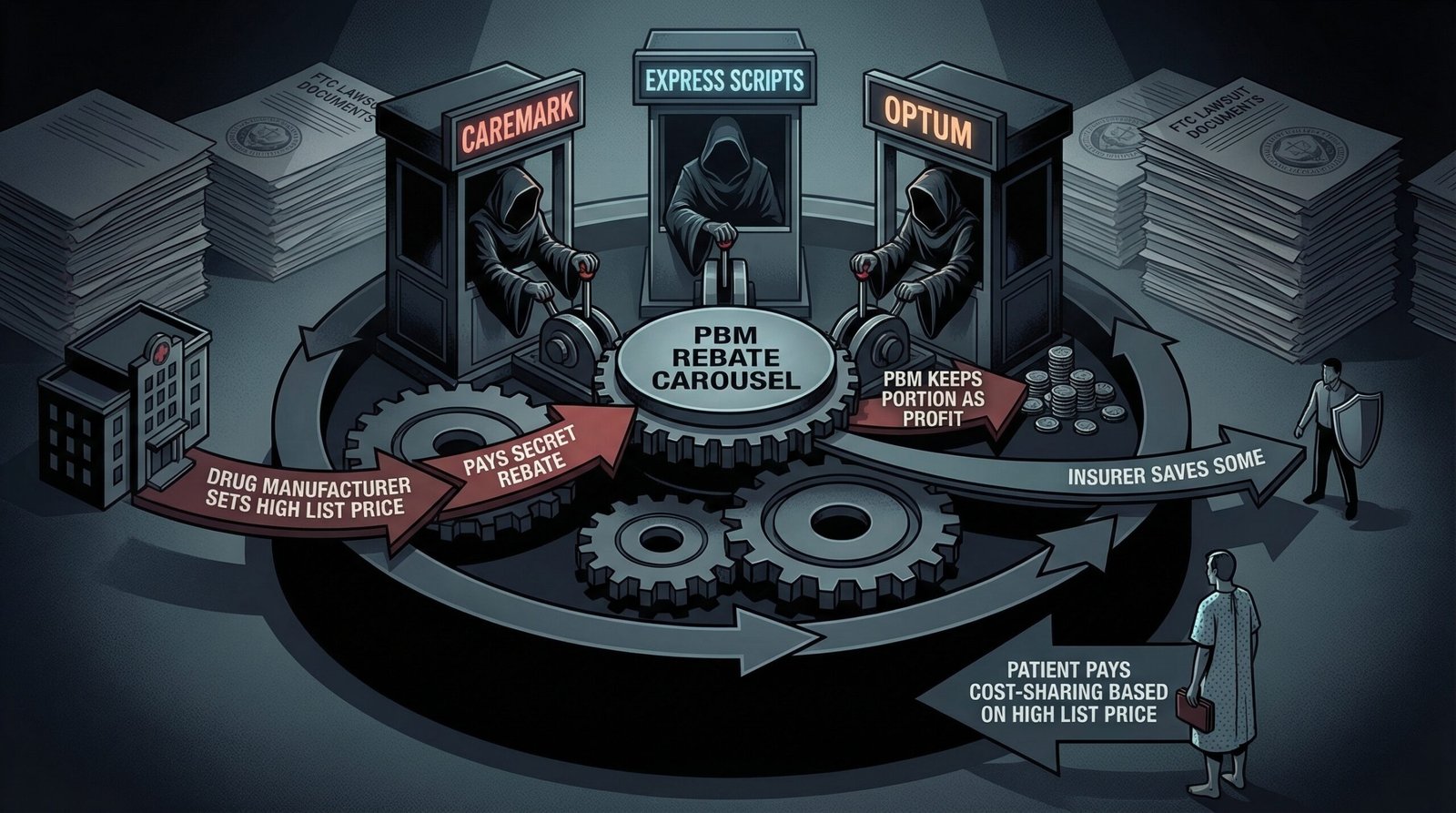

- Three pharmacy benefit managers (PBMs) — Caremark, Express Scripts, and Optum — control about 80% of U.S. prescription drug coverage. The FTC sued all three in September 2024, alleging they artificially inflated insulin prices by creating a rebate system where PBM revenue is tied to a percentage of a drug’s list price — creating a structural incentive to keep list prices high while negotiating secret rebates paid by manufacturers.

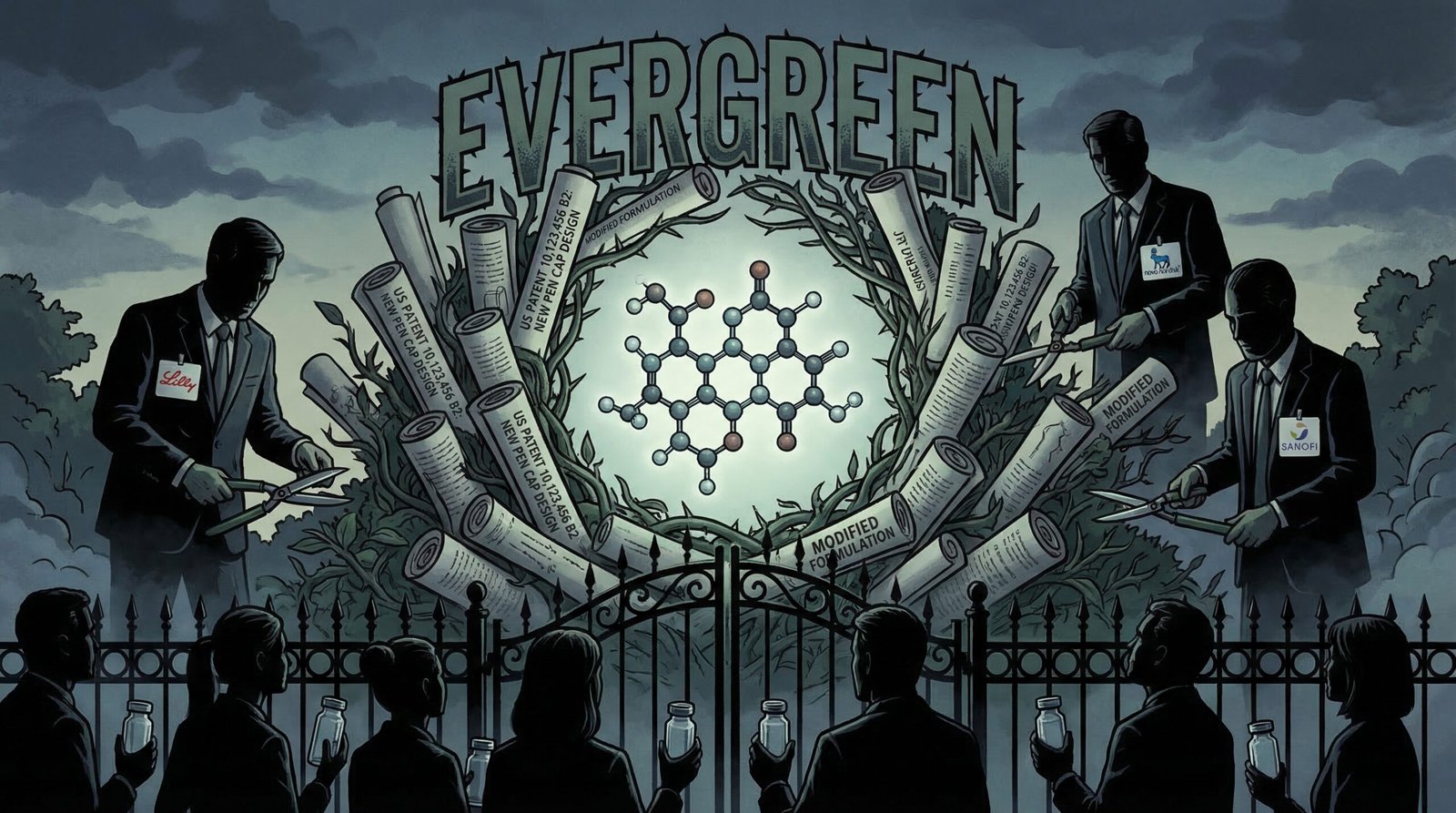

- Eli Lilly, Novo Nordisk, and Sanofi have collectively filed hundreds of patents on insulin formulations, delivery devices, pen caps, and packaging — not the insulin molecule itself, but incremental modifications that extend market exclusivity for decades. In 2014, there were 19 active insulin patents: 10 by Novo Nordisk, 6 by Sanofi, 3 by Eli Lilly. This “evergreening” strategy blocks generic competition.

- At the peak of the crisis, 1 in 5 Americans under 65 who use insulin reported rationing it due to cost (2021 NHIS data). 1.3 million Americans rationed insulin annually. At least 13 confirmed deaths from insulin rationing occurred between 2017 and 2019. 14.1% of insulin users — nearly 1.2 million Americans — reached catastrophic healthcare spending levels in 2022.

- The Inflation Reduction Act (2022) capped Medicare insulin out-of-pocket costs at $35/month. A Senate vote to extend the $35 cap to commercial insurance failed 57–43 — three votes short of the 60 needed to overcome a filibuster. As of 2026, 29 states have passed state-level insulin caps; California launched $11 CalRx biosimilar insulin pens and a $35/month cap starting in 2026. The uninsured and commercially insured in uncapped states remain fully exposed.

Why Did Insulin Prices Increase 1,200%?

The insulin price crisis has a specific structural cause that predates PBM shenanigans and patent games. The core answer is: three companies control 90% of the global insulin market, and for decades they raised prices in lockstep. Eli Lilly, Novo Nordisk, and Sanofi — the Big Three insulin manufacturers — do not compete on price. They compete on marketing, rebate negotiations, and formulary positioning. When one raised its list price, the others followed. The result was parallel pricing behavior so consistent that federal regulators and class-action attorneys have described it as a price-fixing scheme even when no direct coordination could be proven.

The numbers are stark. Prescription drug pricing in America operates without the reference pricing, negotiation rights, or affordability requirements that apply in virtually every other high-income country. For insulin specifically:

- Humalog (Eli Lilly): $20.82 per vial in 1996 → $274.20 in 2016 → $332 by 2019. More than 1,200% over 23 years.

- Novolog (Novo Nordisk): $39.82 per vial in 2001 → $275.29 in 2016.

- Lantus (Sanofi): Similar trajectory — $35 at launch in 2001, rising to over $260 by 2016.

- Between 1996 and 2006 alone: insulin prices increased by 700%.

- Per capita spending on diabetes care increased 228% from 2000 to 2016.

The list price is not the price most insured patients actually pay — insurers and PBMs negotiate rebates that bring the effective cost down. But patients whose insurance has high deductibles, whose plans require cost-sharing based on list price, or who lack insurance at all pay prices anchored to or near that inflated list price. The list price is not a fiction. It is the real price for millions of Americans.

The manufacturing cost of insulin has never come close to justifying these prices. A 2018 analysis by Doctors Without Access found that sustainable cost-based insulin prices — including a profit margin for manufacturers — would be approximately $2–6 per vial for human insulin and $48–71 per vial for analog insulins. The $332 list price for Humalog represents a markup of several thousand percent over actual production cost. The American healthcare system’s inability to control drug prices has never been clearer than in the insulin case — a molecule discovered over a century ago, whose inventors gave it away, transformed into a profit center worth $19.3 billion annually in the U.S. market alone.

How Much More Do Americans Pay for Insulin Than the Rest of the World?

A 2024 RAND Corporation report, updating earlier ASPE research, found that gross insulin prices in the United States are more than nine times higher than in 33 high-income comparison nations. The average list price for one vial of insulin in the U.S. was approximately $98.70 — up to ten times more than in countries like Canada, Germany, Australia, and Japan, where most insulin vials cost $8–10.

For a type 1 diabetic — who has no choice about whether to use insulin, since their pancreas produces none — this is not an abstract price comparison. It is the difference between financial stability and medical bankruptcy. A type 1 diabetic may require 3–6 vials of insulin per month depending on their regimen. At the peak U.S. list price of $275–$332 per vial, that is $825–$1,992 per month, or $9,900–$23,904 per year — just for insulin, before CGM sensors, test strips, pump supplies, or any other diabetes management costs.

The American Diabetes Association estimated total annual costs of diagnosed diabetes at $412.9 billion in 2022 — $306.6 billion in direct medical costs and $106.3 billion in reduced productivity. Mean annual care costs for a child with type 1 diabetes rose from $11,178 in 2012 to $17,060 in 2016, driven primarily by insulin costs. A type 1 diabetic diagnosed at age 20 faces a lifetime of insulin dependency — an estimated additional $203 billion in cumulative costs versus non-diabetic peers over 10 years, per a 2020 JDRF/SAGER analysis.

The generational angle is not subtle: type 1 diabetes is typically diagnosed in childhood or young adulthood. Every Millennial or Gen Z person diagnosed with type 1 diabetes inherited a system that would charge them $1,000+ per month for a medication that costs $5 to produce — for the rest of their lives. The same system that inflated housing costs, crushed student loan burdens, and eliminated pensions also decided that keeping insulin affordable was someone else’s problem.

How Do PBMs Inflate Insulin Prices?

Pharmacy benefit managers — the middlemen who manage prescription drug coverage for insurers and employers — are the least-discussed and arguably most important structural cause of the insulin price crisis. In September 2024, the Federal Trade Commission filed suit against the three largest PBMs — Caremark (CVS Health), Express Scripts (Cigna), and Optum (UnitedHealth Group) — alleging they had artificially inflated insulin prices through a corrupt rebate architecture.

The mechanism is counterintuitive but well-documented. PBMs negotiate drug formulary placement with manufacturers. Manufacturers compete for “preferred” formulary status — the position that means their drug is covered at the lowest out-of-pocket cost for patients, driving volume. To secure preferred placement, manufacturers pay PBMs “rebates” — percentage-of-list-price payments that go to the PBM, and in some arrangements, partially back to the insurer. The critical structural flaw: PBM rebate revenue is calculated as a percentage of the drug’s list price. This means PBMs earn more when list prices are higher. A PBM that negotiates a 40% rebate on a $300 vial earns $120 per vial. If the list price were $30, the same 40% rebate would yield $12. The PBM’s financial incentive is to keep list prices inflated.

The FTC’s 2024 lawsuit alleged the PBM rebate system created a “perverse incentive” that drove insulin list prices higher while manufacturers competed on rebate generosity rather than actual price. The three PBMs collectively manage pharmacy benefits for approximately 270 million Americans. A February 2026 settlement between the FTC and the PBMs was characterized by patient advocates as inadequate — addressing some practices without structurally dismantling the rebate architecture. The pattern of regulatory capture in American consumer finance has a direct analog in pharmaceutical pricing: the system was designed to benefit intermediaries, not patients.

The three PBMs named in the FTC suit are subsidiaries of three of the largest health insurance conglomerates in the country. CVS Health (Caremark) had $372 billion in revenue in 2023. UnitedHealth Group (Optum) had $372 billion. Cigna (Express Scripts) had $195 billion. These are not firms operating on thin margins who needed to manipulate insulin prices to survive. They are the largest healthcare corporations in American history, extracting rebates from the insulin supply chain while 1.3 million people rationed doses.

How Does Patent Evergreening Keep Insulin Expensive?

Insulin itself — the active molecule — is not patented. It never was, after Banting and Best’s 1923 decision. The patents that keep insulin expensive today are on everything surrounding the molecule: delivery devices, pen designs, formulation concentrations, combination products, dosing algorithms, and packaging configurations. This strategy — called “evergreening” — involves filing new patents on incremental modifications to extend market exclusivity indefinitely, preventing the entry of generic or biosimilar competition that could drive prices down to manufacturing cost.

A 2014 analysis found 19 active insulin patents: 10 by Novo Nordisk, 6 by Sanofi, 3 by Eli Lilly. A 2018 study documented that the three major insulin manufacturers collectively held hundreds of patents on insulin-related products. A TIME Magazine investigation found manufacturers filed new patents in clusters whenever key patents were approaching expiration — not because the new filings represented medical innovation, but specifically to maintain the patent wall that blocks competitors.

The practical effect is that a true generic analog insulin — which would require FDA approval as a biosimilar — faces a gauntlet of patent litigation that can take years and cost hundreds of millions of dollars to navigate. Civica Rx, a nonprofit drug manufacturer, launched insulin at no more than $30 per vial in 2024 — proving that a non-extractive pricing model is possible. California’s CalRx program will offer state-branded biosimilar insulin pens at $11 each starting in 2026. These examples demonstrate that the manufacturing economics allow for dramatically lower pricing; the barrier is not production cost, it is the patent-and-rebate architecture that the Big Three have built over decades.

The evergreening problem is not unique to insulin — it is the same mechanism documented in the broader prescription drug pricing crisis. But insulin’s unique characteristics — non-elective, lifelong, no therapeutic substitute for type 1 diabetics, insulin-dependent type 2 diabetics, and LADA patients — make the evergreening dynamic especially predatory. You cannot decide not to take insulin and switch to a cheaper alternative. You take it or you die. The patent system was not designed to accommodate that particular kind of captive demand.

How Many Americans Are Rationing Insulin and Dying?

The human cost of the insulin price crisis is documented in peer-reviewed medical literature and confirmed in congressional testimony, investigative journalism, and coroner’s reports. These are not abstractions.

According to the 2021 National Health Interview Survey, 1 in 5 (20.4%) of U.S. adults younger than 65 who use insulin reported rationing it due to cost. A 2022 study published in Annals of Internal Medicine found that 1.3 million Americans with diabetes — approximately 16.5% of all insulin users — rationed insulin in the prior year. The rationing was not uniform: 29% of uninsured individuals rationed insulin, versus 19% with private insurance. 18.6% of type 1 diabetics reported rationing; so did 15.8% of type 2 diabetics.

Confirmed deaths from insulin rationing between 2017 and 2019:

- 2017: four confirmed deaths from insulin rationing

- 2018: four confirmed deaths

- 2019: five confirmed deaths, including Alec Raeshawn Smith (26, Minnesota), Jesse Lutgen (27, Wisconsin), and Shane Patrick Boyle (48, Arkansas)

These are the confirmed, documented cases. Diabetic ketoacidosis — the metabolic crisis that kills when insulin is insufficient — can masquerade as other causes of death or simply not be investigated for cost-related underpinning. The actual death toll from insulin rationing in the United States is almost certainly higher than the documented 13.

The physical consequences of under-dosing extend beyond death. DKA hospitalizations among adults aged 18–44 increased from 24.4 per 1,000 to 43.5 per 1,000 between 2009 and 2015 — the years of steepest insulin price increases. Only 30.3% of insulin-treated adults younger than 50 met hemoglobin A1c targets, compared to rates exceeding 50% in countries with insulin price controls. The ACA coverage gaps and the medical debt crisis compound these effects: the same populations least able to afford insulin are most likely to be uninsured or underinsured, creating cascading medical and financial consequences from a single pricing failure.

A 2022 Health Affairs study found that 14.1% of insulin users — nearly 1.2 million Americans — reached catastrophic spending levels, defined as healthcare costs exceeding 40% of post-subsistence income. For a Millennial or Gen Z adult with type 1 diabetes and a median income, catastrophic spending is not a theoretical scenario. It is a recurring annual event. The total annual cost of diabetes in the U.S. hit $412.9 billion in 2022.

What Has Congress Actually Done About Insulin Prices?

The legislative history of insulin price reform is a precise map of whose interests Congress actually protects.

The Inflation Reduction Act of 2022 included a cap on Medicare out-of-pocket insulin costs at $35 per month per covered product — effective January 1, 2023 for Part D and July 1, 2023 for Part B. This was the first federal insulin affordability provision in U.S. history. It applies exclusively to Medicare enrollees — primarily Americans 65 and older. The Affordable Insulin Now Act, which would have extended the $35 cap to commercial insurance, passed the House. In the Senate, it failed 57–43 — three votes short of the 60-vote threshold needed to overcome a Republican-led filibuster. Seven Republicans who had supported a non-binding resolution for insulin affordability voted against the binding legislation when it came to a floor vote.

The pharmaceutical industry spent $373 million on federal lobbying in 2022 — the year both the IRA insulin cap and the commercial cap were debated. The three major insulin manufacturers spent heavily on lobbying in the years of peak price controversy. Eli Lilly’s lobbying disclosures show millions spent annually during the period when its insulin prices were rising fastest. The revolving door between pharmaceutical companies and the FDA, HHS, and congressional staff is well-documented.

State-level progress has been more substantive: 29 states had passed insulin copay cap legislation by 2025. Caps range from $25 (Montana) to $100 (Alabama) per month. California went furthest: a $35 cap on commercial insurance took effect in 2026, combined with the CalRx program offering state-manufactured biosimilar insulin pens at $11 each. Minnesota passed the Alec Smith Emergency Insulin Act — named after a rationing victim — allowing uninsured residents to obtain insulin at cost from any pharmacy for $35 per vial in emergency situations.

Voluntary manufacturer price reductions began in 2023. Eli Lilly capped its Humalog and Basaglar prices at $35/month for most commercially insured patients and cut list prices by 70% for its primary insulin products. Novo Nordisk and Sanofi followed with similar voluntary programs. GoodRx data shows average insulin unit prices dropped 42% between 2019 and mid-2024. The question is what drove these changes: genuine market competition, fear of regulation, or — as a JAMA Network Open analysis suggested — Eli Lilly’s voluntary price cuts helped it avoid an estimated $430 million in additional Medicaid rebates in 2024 by preventing the Biden administration from triggering drug price negotiation provisions.

The Counter-Argument: Insulin Prices Have Come Down

The pharmaceutical industry and some health economists argue that the insulin price crisis narrative overstates current conditions. There are legitimate data points supporting a more optimistic view.

GoodRx’s 2025 research showed average insulin unit prices at their lowest level in a decade — down 42% from 2019 to mid-2024. The voluntary manufacturer price reductions, combined with Medicare price caps and state-level legislation, have meaningfully reduced out-of-pocket costs for many Americans. Civica Rx’s nonprofit model and California’s CalRx program demonstrate that the system can produce dramatically lower prices when structured to do so. For Medicare enrollees — the largest single population of insulin users — the $35 cap has been enormously significant.

The industry also argues that list prices are misleading because rebates substantially reduce the net price actually paid. Manufacturers point to patient assistance programs, savings cards, and direct-to-patient pricing options as evidence that access exists even when list prices are high. PBMs argue that their negotiating power is what produces lower net prices for insurers, and that eliminating the rebate system would raise costs for most insured patients.

Where the counter-argument falls short:

Price reductions since 2023 are welcome and real. They do not explain or excuse the 30 years of price inflation that preceded them, or the 13 documented deaths that occurred while those prices were rising. The reductions also came only after sustained political pressure, the threat of mandatory price negotiation under the IRA, and the credible possibility of federal legislation. They did not come from market competition — because the market structure that enabled the crisis has not materially changed. The same three companies still control 90% of the market. The same PBM rebate architecture still exists. The same patent evergreening strategies remain in place. What has changed is the political environment, not the structural conditions that created the problem.

The 25–30% of Americans with type 1 diabetes who still reported rationing insulin as of recent surveys are not capturing the benefit of voluntary manufacturer programs or state caps. They are uninsured, in states without caps, or navigating the bureaucratic complexity of assistance programs while managing a chronic condition that requires constant attention. “Assistance programs exist” is not the same as “the crisis is resolved.”

FAQ: Insulin Price Crisis

How much does insulin cost in the United States vs other countries?

According to RAND Corporation and ASPE research, the United States pays approximately 9–10 times more for insulin than 33 comparable high-income nations. Most countries price a vial of insulin at $8–10. In the U.S., list prices ranged from $98–$332 per vial at peak, though voluntary manufacturer price cuts and state caps have reduced out-of-pocket costs for many insured patients since 2023. The uninsured in states without price caps still face full list price exposure.

How many people have died from insulin rationing in the United States?

At least 13 confirmed deaths from insulin rationing were documented between 2017 and 2019, including Alec Raeshawn Smith (26), Jesse Lutgen (27), and Shane Patrick Boyle (48). These are only the confirmed, investigated cases. Diabetic ketoacidosis — the lethal consequence of insufficient insulin — can be attributed to multiple causes, and deaths that occur outside hospital settings may not be investigated for cost-related under-dosing. The actual death toll is widely believed to be higher than the documented figure. As of 2026, an estimated 25–30% of Americans with type 1 diabetes still report rationing or skipping insulin doses.

Is insulin still expensive in 2026?

Partially. For Medicare enrollees, the Inflation Reduction Act capped out-of-pocket insulin costs at $35/month (effective 2023). For commercially insured patients, voluntary manufacturer programs have made $35/month caps broadly available from Eli Lilly, Novo Nordisk, and Sanofi. California, Minnesota, and 28 other states have legislated insulin price caps. However, uninsured Americans, residents of states without caps, and patients whose plans don’t participate in voluntary programs can still face high costs. GoodRx data shows average insulin unit prices dropped 42% from 2019 to mid-2024 — but 25–30% of type 1 diabetics still reported rationing as of recent surveys. The structural conditions — Big Three market dominance, PBM rebate architecture, patent evergreening — remain substantially intact.

Why didn’t insulin prices fall sooner if the molecule is off-patent?

The insulin molecule is indeed off-patent. But biosimilar insulin — a near-identical copy produced by a competitor — must navigate a separate, more complex FDA approval pathway than small-molecule generics, and faces a wall of secondary patents on delivery devices, formulations, pens, and packaging. The three major manufacturers held 19 active insulin patents in 2014 alone — not on insulin itself, but on every aspect of how it is delivered and presented. Navigating that patent thicket requires years and hundreds of millions in legal costs. The PBM rebate system further disadvantages new entrants: a biosimilar with a lower list price generates smaller rebates, making it less attractive for PBMs to place it on preferred formulary even if the net cost is similar. The result is that market entry barriers remain high despite the off-patent status of the core molecule.

Sources & Methodology

Primary sources: Cost-Related Insulin Rationing in US Adults Younger Than 65 Years — PMC/NHIS 2021 (National Health Interview Survey); RAND Corporation: Insulin Prices Sharply Higher in the US Than Other Countries (Feb 2024); ASPE: Comparing Insulin Prices in the US to Other Countries; FTC: FTC Sues Prescription Drug Middlemen for Artificially Inflating Insulin Prices (September 2024); GoodRx Research: Insulin Costs Plummet — A Decade-Long High Comes to an End (Jan 2025); Right Care Alliance: High Insulin Costs Are Killing Americans (confirmed death documentation); Public Citizen: 1.3 Million Americans Ration Insulin Due to Cost; Health Action International: Insulin Patent Profile — 19 Active Patents in 2014; TIME: Drug Makers Manipulate Patents to Keep Insulin Prices High; JAMA Network Open: The Rise and Fall of the Insulin Pricing Bubble; Policy Matters Ohio: Insulin Price-Gouging Kills — catastrophic spending data; American Diabetes Association: Economic Costs of Diabetes 2022 — $412.9 Billion; UCLA Law Review: Essential Medications and Market Power — Insulin Through an Antitrust Lens (February 2026). Humalog price history: Beta Cell Action, Patients for Affordable Drugs, Mayo Clinic Proceedings. State insulin cap data: American Diabetes Association state legislation tracker, NCSL.