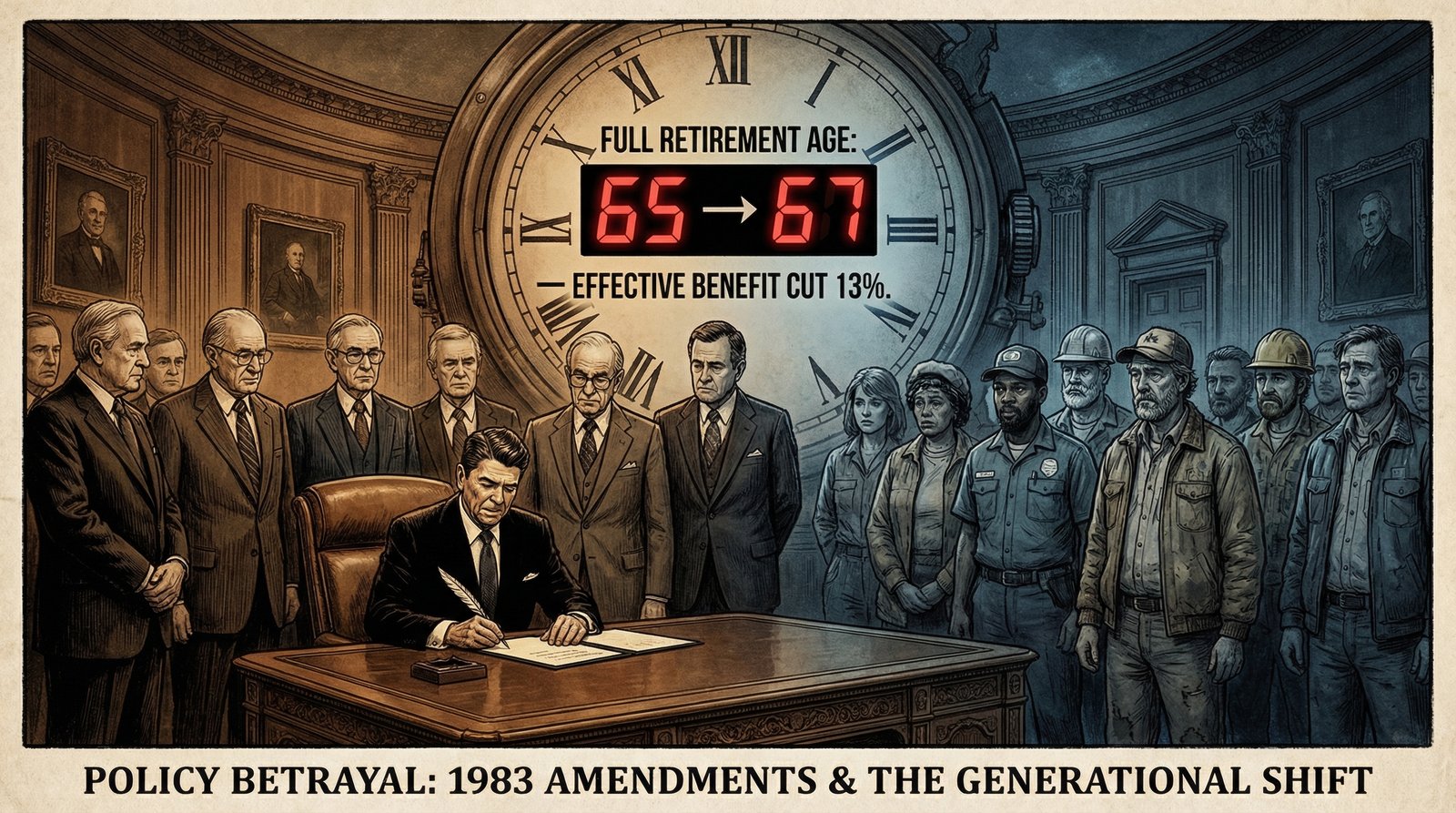

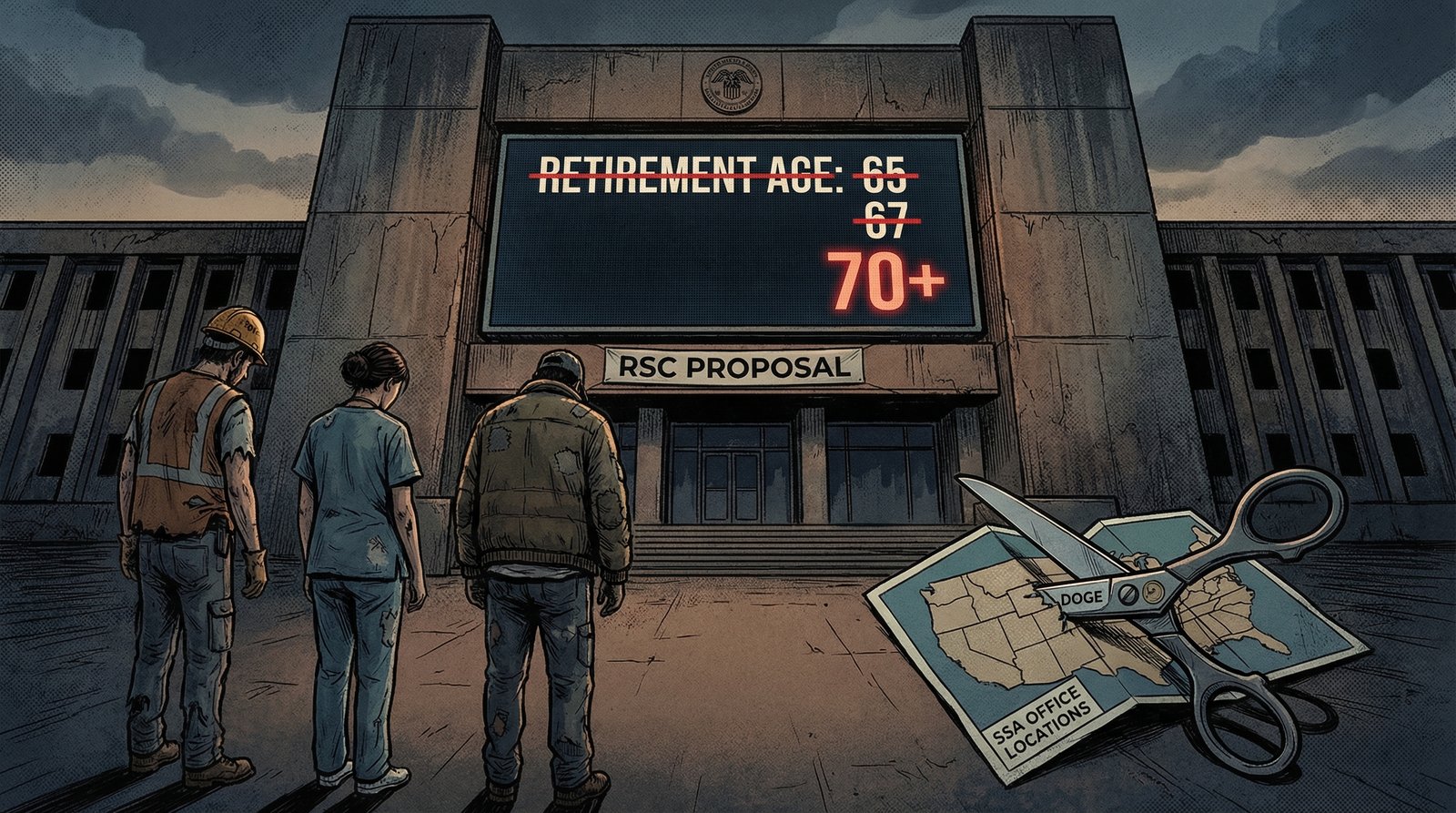

The Social Security full retirement age is 67 for anyone born after 1960 — a quiet benefit cut baked into the 1983 Social Security Amendments that most Americans didn’t notice until it was too late. That increase from 65 to 67, engineered by the Greenspan Commission under Ronald Reagan, is mathematically equivalent to a 13% reduction in lifetime Social Security benefits for every new retiree. Now Congress is debating whether to raise the retirement age to 69 or 70, which would cut benefits by an additional 13–20% — disproportionately punishing blue-collar workers, low-income earners, and Black Americans, who have seen little to no life expectancy gains since 1983 and whose bodies often can’t make it to 67, let alone 70.

Key Takeaways:

- The 1983 Social Security Amendments — signed by Reagan, engineered by the Greenspan Commission — raised the full retirement age from 65 to 67. CBPP calculates this as a 13% effective lifetime benefit cut for all new retirees.

- Proposals to further raise the retirement age to 70 would cut currently scheduled benefits by an additional nearly 20%, according to CBPP.

- The life expectancy argument for raising the retirement age collapses when you disaggregate by income: for the bottom half of earners, life expectancy at 65 has barely risen since 1983, while gains for the top quintile have been substantial.

- Roughly half of older workers ages 50–70 have physically demanding jobs or work under hazardous conditions, per EPI. For them, “work until 67” is not a policy preference — it is a physical impossibility.

- Claiming Social Security at 62 triggers a permanent 30% benefit reduction — a catastrophic penalty for workers who physically can’t keep working but can’t afford to wait.

- Nearly 30% of new Social Security beneficiaries claim at age 62, the earliest possible age — suggesting millions are forced to take the penalty, not choosing to.

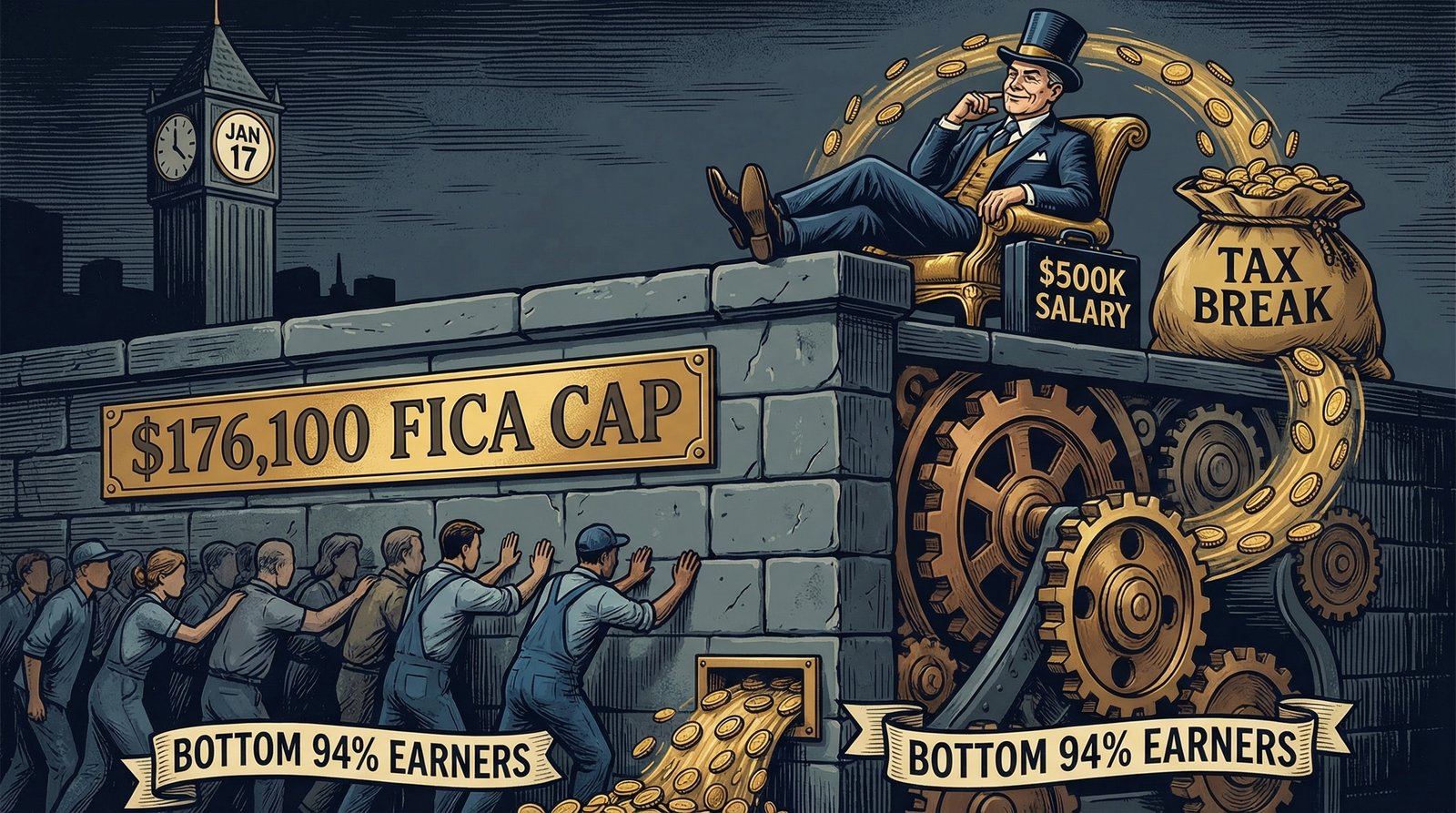

- In 2026, the Social Security FICA payroll tax cap sits at $176,100. Above that income, workers stop paying into Social Security — meaning a CEO earning $1 million pays the same dollar amount in SS taxes as someone earning $176,100.

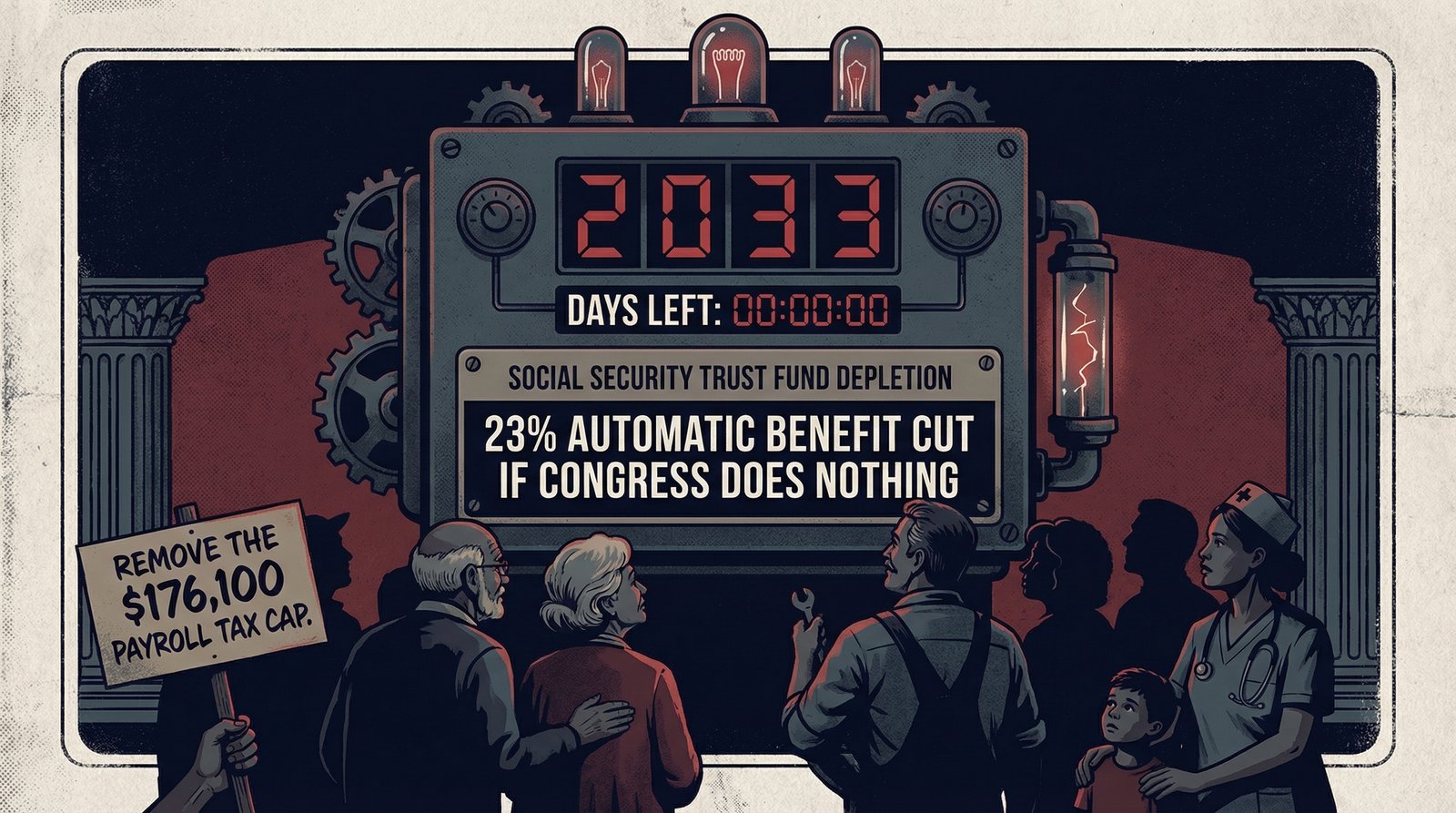

- The Social Security trust fund is projected to be depleted in 2033, per the 2025 Trustees Report, forcing a 23% automatic benefit cut if Congress does nothing — roughly the same size cut that raising the age to 70 would impose, just more sudden.

- DOGE cut the Social Security Administration’s staff by roughly 7,000 workers — 12% of the workforce — deepening backlogs and wait times for current beneficiaries before 2033 even arrives.

What Is the Social Security Full Retirement Age — and When Did It Change?

Social Security was signed into law in 1935 with a full retirement age of 65. At the time, average life expectancy at birth was roughly 62 years. The retirement age wasn’t set because 65 was a rational threshold for when people should stop working — it was set because it roughly aligned with the average worker’s life expectancy, ensuring that Social Security would function as catastrophic insurance for those who outlived their working years, rather than a universal guaranteed income supplement. The original actuarial math was brutal but coherent: most people wouldn’t live long enough to collect much.

That design premise held, in a rough sense, for decades. By 1983, however, Social Security was facing a serious near-term financing crisis. The Greenspan Commission — formally the National Commission on Social Security Reform — was assembled by Reagan to find a bipartisan solution. What it produced was a package of fixes that included both benefit cuts and tax increases. The most consequential long-term change was buried in the details: a gradual increase in the full retirement age (FRA) from 65 to 67, phased in over decades beginning in 2000.

The current FRA schedule, for anyone born after 1960, is age 67. This means:

- Claim at 62 (the earliest eligible age): receive only 70% of your full benefit, permanently.

- Claim at 67 (the new FRA): receive 100% of your calculated benefit.

- Claim at 70 (the maximum delay): receive approximately 124–132% of your calculated benefit.

Every month you claim before 67, your benefit is permanently reduced by 5/9 of 1% per month (5/12% for months beyond 36). This is not a temporary reduction — it follows you for life and affects your survivors’ benefits.

The important thing to understand about that FRA increase is that it was not just an administrative adjustment — it was a stealth benefit cut dressed up as a longevity accommodation. As the Center on Budget and Policy Priorities notes, “the last major Social Security overhaul, in 1983, gradually raised the age to 67, effectively cutting benefits by 13 percent.” Every future retiree received fewer lifetime benefit dollars than their parents’ generation for the same work history. No one voted on a benefit cut. Congress voted on a retirement age adjustment.

Related: why pensions disappeared, the Millennial retirement savings catastrophe, how Wall Street extracts $50 billion from your 401k, and the $1.3 trillion public pension bomb.

The 1983 Greenspan Commission: How a Boomer-Era Deal Locked In a 13% Benefit Cut for Everyone Who Came After

The 1983 Social Security fix is frequently cited as a model of bipartisan governance — a Boomer-era success story of adults in the room making hard choices to save the program. That framing deserves scrutiny.

The package that emerged from the commission included a mix of measures: accelerated tax increases, taxation of Social Security benefits for higher earners, expansion of Social Security coverage to federal employees and non-profit workers, and the retirement age increase. The political genius of the fix was that the most significant long-term benefit cut — the FRA increase — was designed not to take effect until 2000, with full implementation completing in 2027. The people who would bear the cost were younger workers who, in 1983, were in their 20s and 30s. The Boomers who were already close to retirement age were largely exempted from the change.

Workers born between 1943 and 1954 saw their FRA set at 66. Workers born 1955–1959 saw it inch up from 66 to 66 years and 10 months. Workers born in 1960 and after — essentially, the older end of Millennials and Generation X — got 67. The Boomers who controlled Congress in 1983 made a deal that the generations behind them would pay for. This is not a conspiracy theory; it is structural in the legislation’s phase-in schedule.

The 1983 fix also did not eliminate the solvency problem — it deferred it. The projected 2033 depletion date means the fix bought roughly 50 years of breathing room. What it did not do was implement a permanent solution that scales with demographics or wages. It kicked the can to the generation now in its 40s and 50s, who are being asked to absorb another round of benefit cuts through retirement age increases while simultaneously being denied the pension system that existed for their parents.

In 1983, Congress voted on a retirement age adjustment. What they actually enacted was a 13% lifetime benefit cut — for workers who were in elementary school at the time.

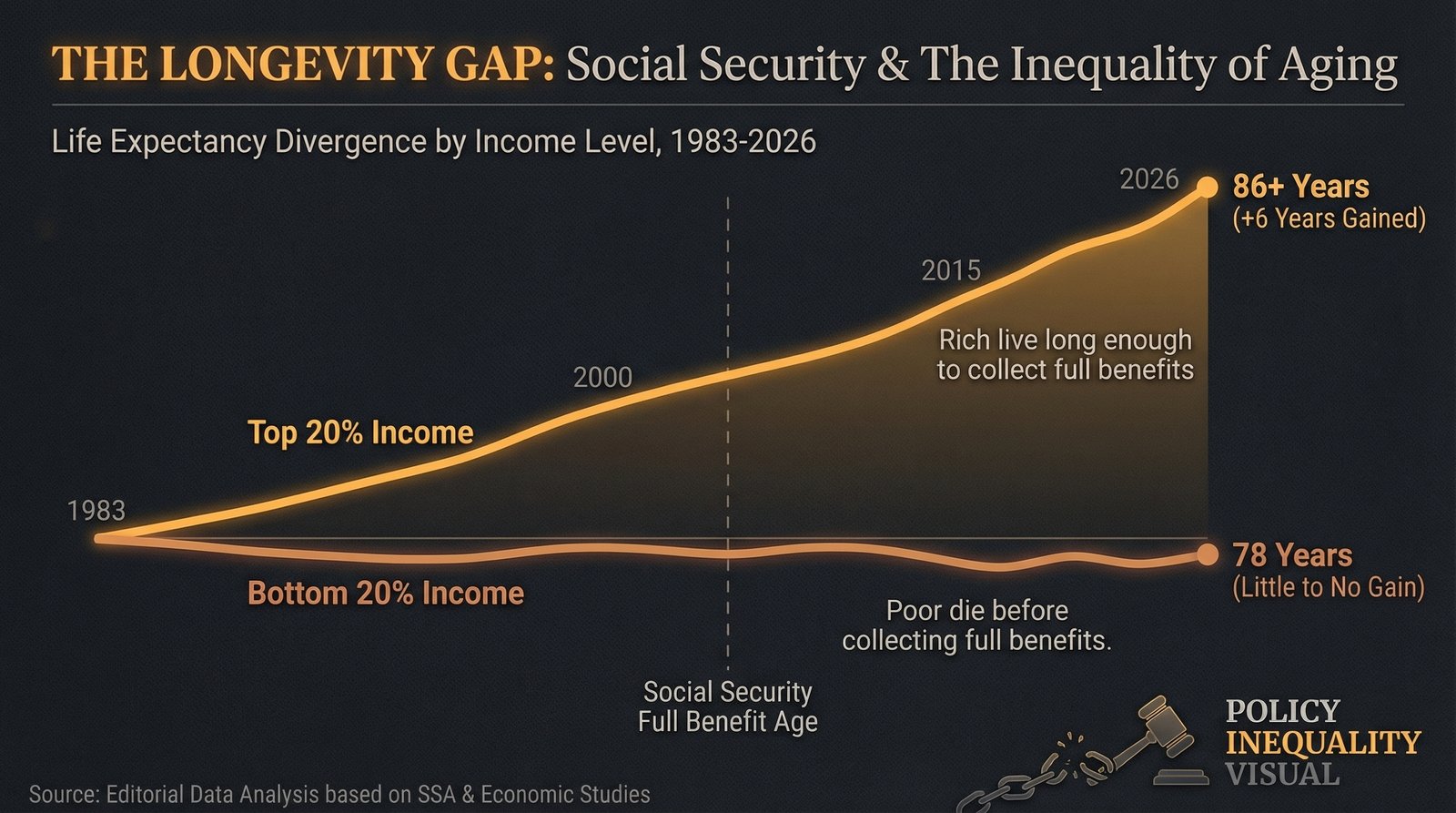

The Life Expectancy Lie: Why ‘People Are Living Longer’ Is the Wrong Argument for Raising the Retirement Age

The central justification for raising the Social Security retirement age — offered by everyone from the Republican Study Committee to deficit-hawk think tanks — is that Americans are living longer than they were in 1935 or 1965, so it’s only fair to work longer before collecting benefits. This argument is not factually wrong in the aggregate. It is misleading in its application.

Life expectancy gains in the United States since 1983 have been dramatically unequal by income. A 2016 landmark study by Raj Chetty and colleagues at Opportunity Insights, using 1.4 billion anonymous earnings and mortality records, found that the gap in life expectancy between the richest 1% and poorest 1% of Americans is approximately 14–15 years for men and 10 years for women. Richer Americans are living longer and longer; poorer Americans are not.

For the bottom quintile of earners — the workers who most need Social Security and who have contributed payroll taxes for their entire working lives — life expectancy gains since 1983 have been essentially zero for men and very small for women, according to the Congressional Research Service’s review of the National Academy of Sciences analysis. A 2024 Senate HELP Committee report found that people living in the top 1% of counties by median income live seven years longer on average than people in the bottom 1% of counties.

Black Americans face compounded disadvantages. According to CBPP, “Black workers in particular still experience lower lifetime earnings and face an average shorter life expectancy than white workers — due in no small part to a long history of structural racism and discrimination in education, housing, health care, and employment.” A policy that raises the retirement age uniformly and calls it neutral is not neutral. It accelerates the benefit cut for the groups least likely to live long enough to recoup their contributions.

There’s also the pandemic effect, which reset life expectancy calculations that retirement age proponents still cite selectively. U.S. life expectancy dropped by nearly three years between 2019 and 2021 — a massive reversal driven not only by COVID-19 deaths but by opioid deaths, mental health crises, and preventable chronic disease deaths — all disproportionately concentrated in exactly the lower-income, working-class populations that proponents of the retirement age increase tell to simply work longer. Average life expectancy at birth in 2024 is 77.5 years — still well below peer nations and below where it was projected to be before the opioid crisis hit.

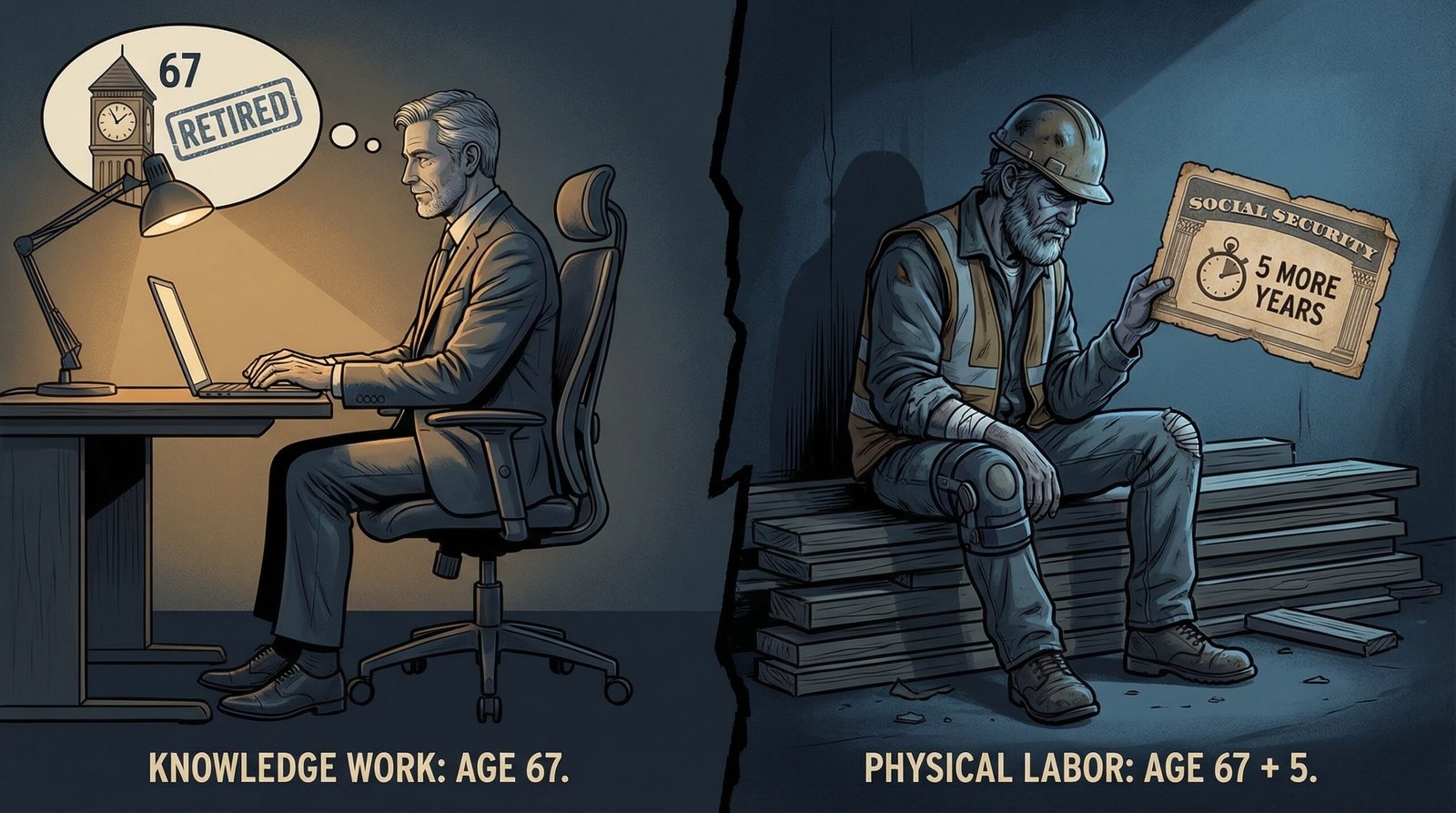

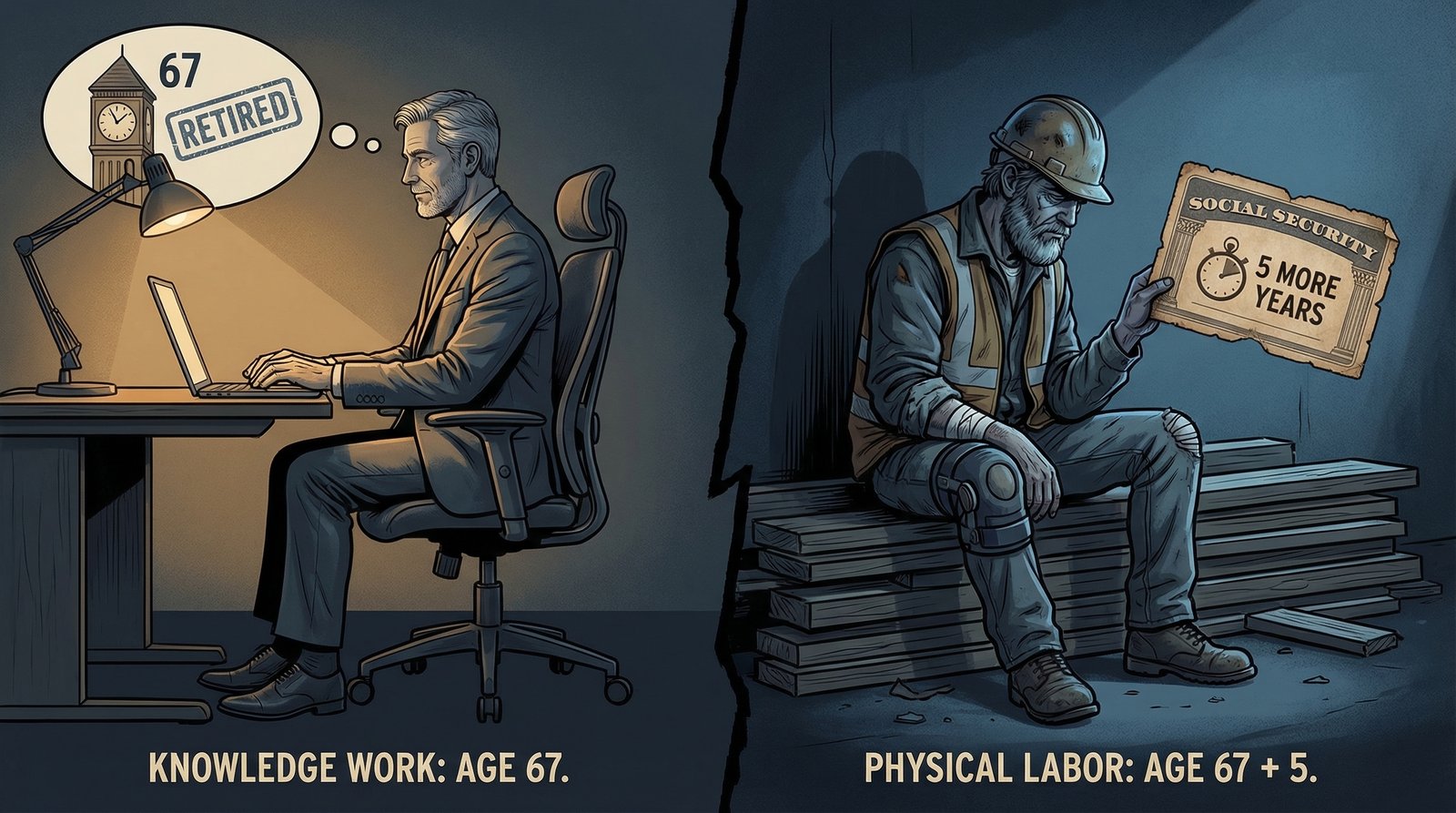

The Physical Labor Penalty: When Your Body Gives Out Before the Government Lets You Retire

For a professional working at a computer, retiring at 67 is inconvenient at worst. For a construction worker, a nurse, a warehouse picker, a home health aide, or a hotel housekeeper — workers whose jobs require physical exertion, repetitive stress, environmental hazard exposure, or demanding schedules — working until 67 is a different proposition entirely.

The data is stark. According to the Economic Policy Institute, roughly half of older workers ages 50–70 experience:

- Physically demanding jobs: 50.3% of older workers

- Environmental hazards: 54.2% of older workers

- Difficult schedules: 53.7% of older workers

- Intense time pressure or stress: significant portion of the total

For workers in these occupations, the practical retirement options are grim. They can work until their body fails — dealing with chronic pain, musculoskeletal injury, and deteriorating health — and claim at 67 for full benefits. Or they can claim at 62 and absorb a permanent 30% reduction in their monthly benefit for the rest of their lives. Or they can apply for Social Security Disability Insurance — a system that leaves 30,000 Americans dying each year while waiting for approval.

The 62-claim data tells the story: nearly 30% of new Social Security beneficiaries claim at age 62, the earliest eligible age, per SSA data analyzed by Yahoo Finance. A Motley Fool analysis found nearly 1 in 4 seniors — 22.9% of men and 24.5% of women — claim at exactly 62. These are not people who ran the optimization math and decided early claiming worked better for them. Most financial advisors uniformly recommend claiming later. The people claiming at 62 are largely doing so because they cannot physically or financially continue working — and the 30% penalty is simply the cost of giving out.

The CNBC analysis of the National Academy for Social Insurance (NASI) research is explicit: more than 10 million older workers face physical demands in jobs that make it hard to work until the current full retirement age — let alone an age of 69 or 70. These workers are effectively forced into early claiming, compounding their lifetime benefit loss, because the retirement age assumes a working life that their jobs do not permit.

The FICA Cap Nobody Talks About: How Wealthy Earners Stop Paying Social Security Taxes Every January

The standard debate about Social Security solvency focuses almost entirely on one side of the ledger: benefits. How much are we paying out? When will it run out? How do we cut it? The other side — who is paying in, and whether they’re paying their fair share — receives far less attention.

The Social Security payroll tax is 12.4% of wages (6.2% from employee, 6.2% from employer). It applies to earned income up to $176,100 in 2026. Above that threshold — the FICA wage base — the payroll tax simply stops. A worker earning $55,000 pays Social Security taxes on every dollar of every paycheck. A CEO earning $500,000 pays the same absolute dollar amount as someone earning $176,100 — and effectively nothing on the remaining $323,900 of their income.

For someone earning $500,000, Social Security taxes effectively stop around mid-January. For someone earning $5 million — a hedge fund manager, a senior executive, a celebrity — they stop in the first week of January. For the entirety of the remaining 11+ months of the year, these high earners pay zero Social Security tax on their additional earnings.

This is not a historical accident. The earnings cap is a deliberate policy choice that insulates high earners from bearing proportionate costs in the Social Security system. As Rep. John Larson has argued, “the fastest and most effective way to fix Social Security is to raise revenue, not cut benefits — by lifting the earnings cap and taxing employer and employee income for Social Security above the current cap.”

The Congressional Budget Office and multiple independent actuarial analyses have confirmed that eliminating or substantially raising the FICA cap would close most or all of Social Security’s projected funding gap over the 75-year actuarial window — without raising the retirement age, cutting benefits, or asking blue-collar workers to work until their joints give out. The Social Security 2100 Act, introduced by Larson and backed by over 200 co-sponsors, would apply payroll taxes to earnings above $400,000 and extend the fund’s solvency by decades. It has never been brought to a floor vote in the Republican-controlled House.

A construction worker pays Social Security tax on 100% of what they earn. A hedge fund manager pays it on 3% of what they earn. Congress calls this a funding gap problem. Actuaries call it a policy choice.

Now They Want to Push It to 70: What the Republican Study Committee Plan Would Actually Do

The 1983 fix settled at 67 as the full retirement age. That settlement is now being revisited. The Republican Study Committee — a caucus of 190 House Republicans — has proposed gradually raising the full retirement age to 69 for those turning 62 in 2033, with further increases implied. Project 2025, the governing blueprint that has informed significant Trump-era policy, proposes raising the FRA to 70 or beyond. The American Progress analysis of these proposals finds that raising the retirement age to 70 would cut currently scheduled benefits by nearly 20% for all new retirees.

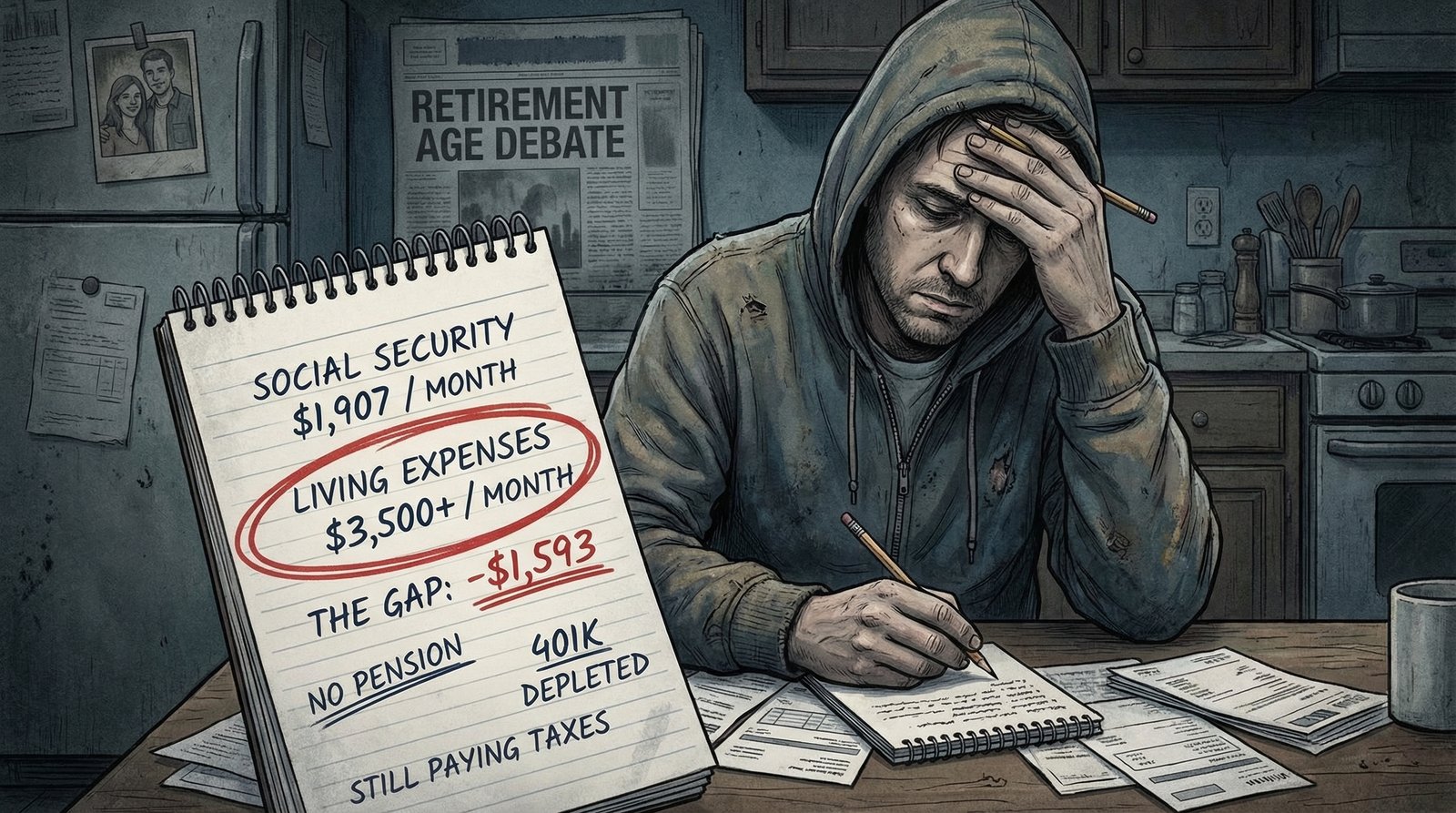

To understand what a 20% benefit cut looks like in practical terms: the average Social Security retirement benefit in early 2026 is approximately $1,907 per month ($22,884 per year), per the SSA’s Monthly Statistical Snapshot. A 20% cut would take that to roughly $1,526/month — well below the federal poverty line for a single person ($15,060/year) in most expensive metro areas. For someone with no other retirement savings, no pension, and a body worn down by 40 years of physical labor, this is not an abstraction. It is a choice between food and rent.

Proponents of raising the retirement age argue that it preserves solvency without requiring tax increases. This is technically true in a narrow sense, but it is analytically dishonest. Raising the retirement age to 70 would ultimately cut average lifetime benefits by nearly 20% — essentially the same magnitude of benefit reduction that would occur if the trust fund depletes in 2033 and Congress does nothing, which would force a 23% automatic cut. The retirement age proponents are offering the same cut, just on a slower, less visible schedule — while claiming it’s a structural reform rather than a benefit reduction. The CBO, SSA actuaries, and CBPP all describe it as a benefit cut, because that is what it is.

DOGE has added a new dimension to the solvency crisis by gutting the Social Security Administration’s operational capacity. EPI reporting shows that DOGE cut approximately 7,000 SSA workers — 12% of the agency’s total workforce — through a combination of buyouts, firings, and hiring freezes. The Guardian reported SSA employees warning of a “death spiral” in which understaffing begets backlogs begets worse service begets more early claims begets more costs. The New York Times found Trump’s Social Security promise “under strain” from Musk’s cuts. The practical effect: seniors and disabled Americans are already experiencing months-long processing delays for retirement and disability claims, and the backlogs will worsen before they improve.

2033 Is Closer Than You Think: The Trust Fund Depletion Clock and What It Means for Millennials

The 2025 Social Security Trustees Report — unchanged from the 2024 projection — places the depletion of the combined Social Security trust funds at 2033. At that point, ongoing payroll tax revenues would cover approximately 77% of scheduled benefits, triggering an automatic 23% across-the-board cut unless Congress acts before then.

Millennials — born roughly 1981–1996 — will be 37–52 years old in 2033. They will have spent their entire adult working lives contributing to a Social Security system whose future is in doubt. They have catastrophic retirement savings shortfalls, no pensions, 401(k)s being slowly drained by Wall Street fees, and now the prospect of retiring into a Social Security system that either cuts benefits by 23% through inaction or cuts them by 20% through a deliberate retirement age increase. The choice being offered is: take the benefit cut now, on a schedule, or take it in 2033, all at once.

What isn’t being offered, at the federal level, is the obvious revenue solution. Lifting the FICA cap — applying the payroll tax to all earned income above $400,000, as the Social Security 2100 Act proposes — would generate enough additional revenue to extend solvency well beyond the 75-year actuarial window. CBO projections and SSA actuarial analyses confirm this. The payroll tax cap solution is actuarially sound, politically popular (polls consistently show 70%+ support for applying Social Security taxes to higher incomes), and has stalled in Congress for years because the people who would pay more are the people with the most lobbying influence over Congress.

The AARP — which bills itself as the nation’s leading advocate for seniors — has its own complicated relationship with this debate. As we covered in our investigation of the AARP’s $1.85 billion lobbying machine, AARP has been inconsistent on retirement age increases and payroll tax cap expansion, partly because its insurance business interests create conflicts of interest with pure beneficiary advocacy. Meanwhile, the revolving door lobbying machine that connects Wall Street, insurance companies, and Congress helps ensure that the solution that doesn’t require asking wealthy earners to pay more stays off the table.

The Counter-Argument: The System Genuinely Does Need to Be Fixed — Just Not Like This

The argument against cutting benefits by raising the retirement age is strong. The argument that Social Security faces real financing challenges is also true. Both things can be accurate simultaneously.

Demographics are real: The ratio of workers to retirees has fallen from roughly 16:1 in 1950 to about 2.8:1 today. As the Boomer generation ages out of the workforce, that ratio will compress further. A system designed in an era of large working-age cohorts is under genuine strain when those cohorts retire. The critics who point to the FICA cap solution are correct, but they sometimes understate how large the financing gap is. Lifting the cap alone may not be sufficient without other adjustments.

Means-testing has a real argument: Some economists argue that Social Security benefits for very high earners (people who will receive large benefits because they had very high lifetime earnings) could be modestly reduced to free up funds for lower-income retirees who depend on Social Security completely. This is politically toxic but actuarially interesting — though it has its own equity problems and has not been modeled in detail by Congress.

Gradual changes have less impact: The 1983 fix’s phase-in over decades did provide workers with time to adjust their plans. A genuine bipartisan fix that combines modest revenue increases (raising the cap), modest benefit adjustments for the highest earners, and preserves benefits for low-income and physically-demanding-job workers is mathematically achievable. The AEI, which is skeptical of life expectancy inequality claims, still acknowledges that any retirement age increase must include hardship exemptions for workers in physically demanding occupations.

What isn’t an honest solution is the approach currently being floated: raise the retirement age across the board, exempt the political class and high earners from contributing more, and call it a reform. That’s not fixing Social Security. That’s using a solvency crisis as cover to cut benefits for the workers who need them most while leaving the FICA cap untouched for the donors who fund congressional campaigns.

FAQ: Social Security Retirement Age

What is the full Social Security retirement age in 2026?

For anyone born in 1960 or later, the full retirement age (FRA) is 67. This was set by the Social Security Amendments of 1983, which gradually raised the FRA from 65 to 67 over a phase-in period that is now complete. You can claim as early as age 62 (with a permanent 30% benefit reduction) or as late as age 70 (with a permanent 24–32% bonus over your FRA benefit, depending on birth year).

How much is the Social Security benefit reduced if you claim at 62?

Claiming at 62, if your FRA is 67, results in a permanent reduction of approximately 30% of your calculated full benefit. This reduction is permanent — it does not go away when you reach 67, and it reduces your survivor benefit as well. The reduction is calculated as 5/9 of 1% per month for the first 36 months before FRA and 5/12 of 1% for months beyond 36. For someone whose full benefit would be $2,000/month, claiming at 62 means receiving approximately $1,400/month for the rest of their life.

Is there a proposal to raise the Social Security retirement age to 70?

Yes. The Republican Study Committee — 190 House Republicans — has formally proposed raising the FRA to 69 for workers turning 62 in 2033, with further increases implied. Project 2025 proposes raising it to 70 or beyond. The Center on Budget and Policy Priorities calculates that raising the FRA to 70 would be the equivalent of a nearly 20% across-the-board lifetime benefit cut for all new retirees. The American Progress analysis found this would cut benefits by thousands of dollars per year for the majority of Americans, with the hardest impact on those earning under $50,000 who depend most heavily on Social Security income.

When will Social Security run out of money?

The 2025 Social Security Trustees Report projects the combined Social Security trust funds will be depleted in 2033 — approximately seven to eight years from now. This does not mean Social Security will cease to exist. It means that after 2033, incoming payroll tax revenue would cover only about 77% of scheduled benefits, forcing a 23% automatic benefit cut for all recipients unless Congress passes legislation to either raise revenue (e.g., lifting the FICA cap) or cut benefits (e.g., raising the retirement age) before that date. Multiple proposals exist to extend the fund’s solvency — the political will to act is the bottleneck, not the actuarial math.

Sources & Methodology

Data sources used in this article:

- Center on Budget and Policy Priorities — “Raising Social Security’s Retirement Age Would Cut Benefits for All New Retirees” — 1983 amendment = 13% benefit cut; raising to 70 = nearly 20% cut; life expectancy gains unequal by income; Black workers lower life expectancy; 2033 depletion = 23% cut

- Social Security Administration — 1983 Social Security Amendments summary — FRA schedule, delayed retirement credit changes

- SSA — Retirement Age and Benefit Reduction calculator — 5/9 and 5/12 reduction formula; 30% reduction at 62

- AARP — Collecting Social Security at 62 vs. 67 vs. 70 — 70% benefit at 62 for those born 1963+

- Chetty et al., Opportunity Insights / JAMA 2016 — 1.4 billion records; 14-15 year life expectancy gap between richest 1% and poorest 1% men; gap growing

- Congressional Research Service — “The Growing Gap in Life Expectancy by Income” — bottom quintile male workers: no life expectancy gains since 1983

- Senate HELP Committee — Working-class Americans live 7 years fewer than wealthy — top 1% vs bottom 1% county income life expectancy gap

- Economic Policy Institute — Roughly half of older workers have difficult jobs — 50.3% physically demanding, 54.2% environmental hazards, 53.7% difficult schedules (ages 50–70)

- CNBC/NASI — 10+ million older workers in physically demanding jobs

- Yahoo Finance — Nearly 30% of new Social Security beneficiaries claim at 62

- Motley Fool — 22.9% men and 24.5% women claim at exactly 62 (2024 SSA data)

- Rep. John Larson — Social Security payroll tax cap analysis; Social Security 2100 Act

- House Budget Committee Democrats — Republican Study Committee retirement age proposals; FRA to 69 for those turning 62 in 2033

- American Progress — Raising retirement age to 70 cuts benefits for nearly three-quarters of Americans

- Bipartisan Policy Center — 2025 Trustees Report: depletion 2033, no change from 2024

- EPI — DOGE plans to cut SSA staff by 7,000 workers (12% of workforce)

- The Guardian — DOGE Social Security “death spiral” staff warnings

- New York Times — Trump Social Security promise under strain from DOGE cuts

- Kiplinger — Average Social Security check February 2026

Methodology: Benefit cut percentages for the 1983 FRA increase and proposed increases to 70 come from CBPP actuarial analysis of SSA data. Life expectancy inequality figures use the Chetty et al. (2016) Opportunity Insights study, the CRS review of NAS data, and the Senate HELP Committee analysis. Early claiming statistics use SSA administrative data via Motley Fool and Yahoo Finance analysis. FICA cap figures use the 2026 SSA wage base of $176,100. DOGE staffing cut figures from EPI analysis. Trust fund depletion date from the 2025 Social Security Trustees Report.