For most Millennials, the Roth IRA vs Traditional IRA decision comes down to one bet: will your tax rate be higher now or in retirement? The Roth IRA taxes your contributions today and lets the money grow and withdraw tax-free; the Traditional IRA defers the tax bill until you pull the money out in retirement. In 2026, with the Tax Cuts and Jobs Act provisions set to expire and marginal rates likely rising, most Millennials earning under $100,000 are better served by a Roth IRA — but the math gets complicated fast once income phase-outs, employer plans, and state taxes enter the picture.

Key Takeaways: (1) The 2026 Roth IRA contribution limit is $7,000 ($8,000 if you’re 50+), with phase-outs beginning at $150,000 single and $236,000 married filing jointly. (2) Roth IRA wins when your retirement tax rate will exceed your current rate — which is statistically likely for Millennials whose peak earning years are still ahead. (3) Traditional IRA contributions are only deductible if your income is below IRS thresholds and you’re not covered by a workplace plan. (4) Earners above the Roth income limit can use the backdoor Roth conversion — a legal two-step maneuver the IRS has acknowledged since 2010. (5) The average Millennial has $49,388 saved for retirement. They need roughly 20x their final salary. The gap is catastrophic.

Roth IRA vs Traditional IRA: The Core Difference

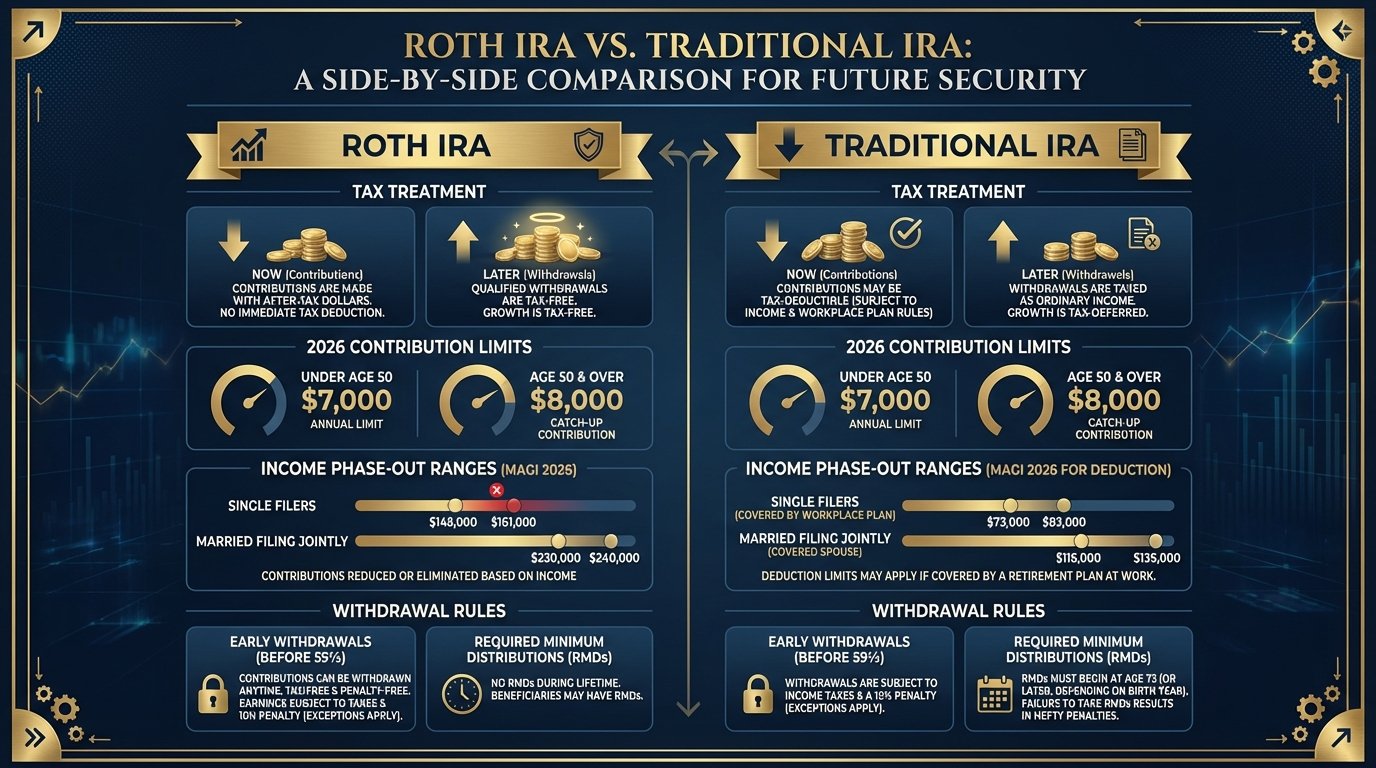

Both the Roth IRA and the Traditional IRA are individual retirement accounts established under IRS rules that let your money grow tax-advantaged. The fundamental split is when you pay taxes.

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax on contributions | After-tax (no deduction) | Pre-tax (deductible if eligible) |

| Tax on growth | Tax-free | Tax-deferred |

| Tax on withdrawals | Tax-free (qualified) | Taxed as ordinary income |

| Required Minimum Distributions | None during owner’s lifetime | Starting at age 73 |

| Early withdrawal of contributions | Anytime, penalty-free | Subject to 10% penalty + tax |

| Income limit to contribute | Yes (phase-out applies) | No income limit (deductibility limited) |

The Roth IRA is the only account in the American tax code where you put in after-tax dollars and never pay taxes on that money again, including decades of compound growth. The federal government is betting you’ll be in a lower tax bracket in retirement. For Millennials, that bet is frequently wrong.

The Millennial retirement savings crisis is already severe: a generation that entered the workforce during the 2008 financial collapse, faced wage stagnation for the better part of a decade, and then watched a pandemic demolish whatever savings momentum they had built. Choosing the right IRA type doesn’t solve that structural problem, but it can meaningfully change the tax math over a 30-year compound window.

For context on what a broken retirement system actually looks like upstream of this choice, read the full breakdown of how the 401(k) replaced pensions and cost an entire generation retirement security.

2026 Contribution Limits and Income Phase-Outs

For tax year 2026, the IRA contribution limits are:

| Age | IRA Contribution Limit (2026) |

|---|---|

| Under 50 | $7,000 |

| 50 and older (catch-up) | $8,000 |

That $7,000 ceiling applies across all IRAs combined. If you have both a Roth and a Traditional IRA, the total cannot exceed $7,000.

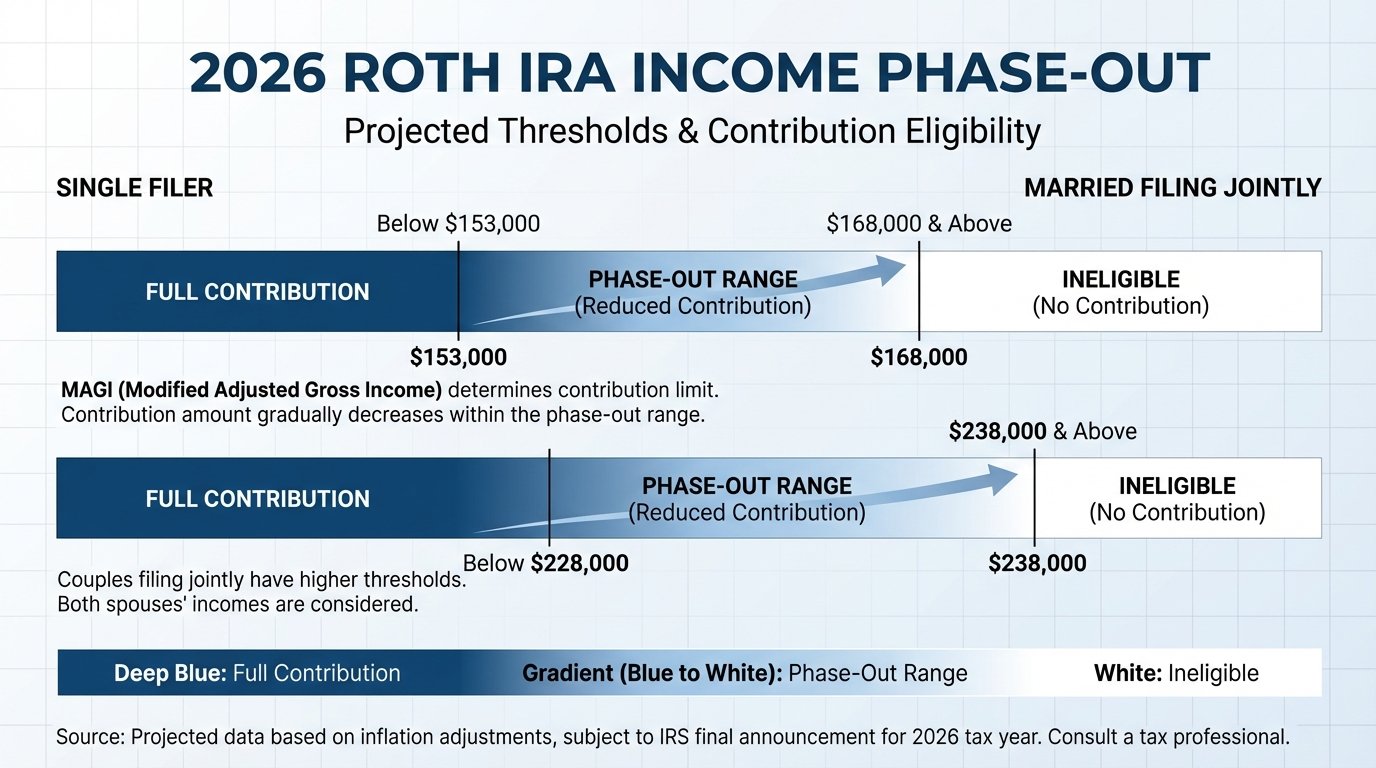

Roth IRA income phase-out ranges for 2026:

| Filing Status | Phase-Out Begins | Phase-Out Ends (Fully Excluded) |

|---|---|---|

| Single / Head of Household | $150,000 | $165,000 |

| Married Filing Jointly | $236,000 | $246,000 |

| Married Filing Separately | $0 | $10,000 |

Between those thresholds, your contribution limit is reduced proportionally. Once you cross $165,000 single (or $246,000 married), direct Roth contributions are forbidden. That’s when the backdoor Roth becomes relevant.

Traditional IRA deductibility phase-outs for 2026 depend on whether you are covered by a workplace retirement plan:

| Filing Status | Deductibility Phase-Out Begins | Ends |

|---|---|---|

| Single (covered by workplace plan) | $79,000 | $89,000 |

| Married (both covered by workplace plan) | $126,000 | $146,000 |

| Married (only spouse covered) | $236,000 | $246,000 |

Above those thresholds, you can still contribute to a Traditional IRA, but the contribution is nondeductible — meaning you get no current-year tax break and you’ll owe taxes on the growth at withdrawal. A nondeductible Traditional IRA is almost never the right choice for a Millennial.

“The 2026 Roth IRA contribution limit of $7,000 represents less than 3% of median U.S. household income. Maxing out an IRA from age 30 to 65 at 7% annual growth yields approximately $1.1 million — roughly 8–9 years of median retirement spending. That is not retirement security. That is the illusion of a plan.”

The Tax Math: Which Account Actually Saves You More?

The core question in the Roth IRA vs Traditional IRA debate: what will your effective tax rate be when you withdraw in retirement, compared to your current marginal rate? If your retirement rate will be lower, Traditional IRA wins. If your retirement rate will be higher or the same, Roth wins.

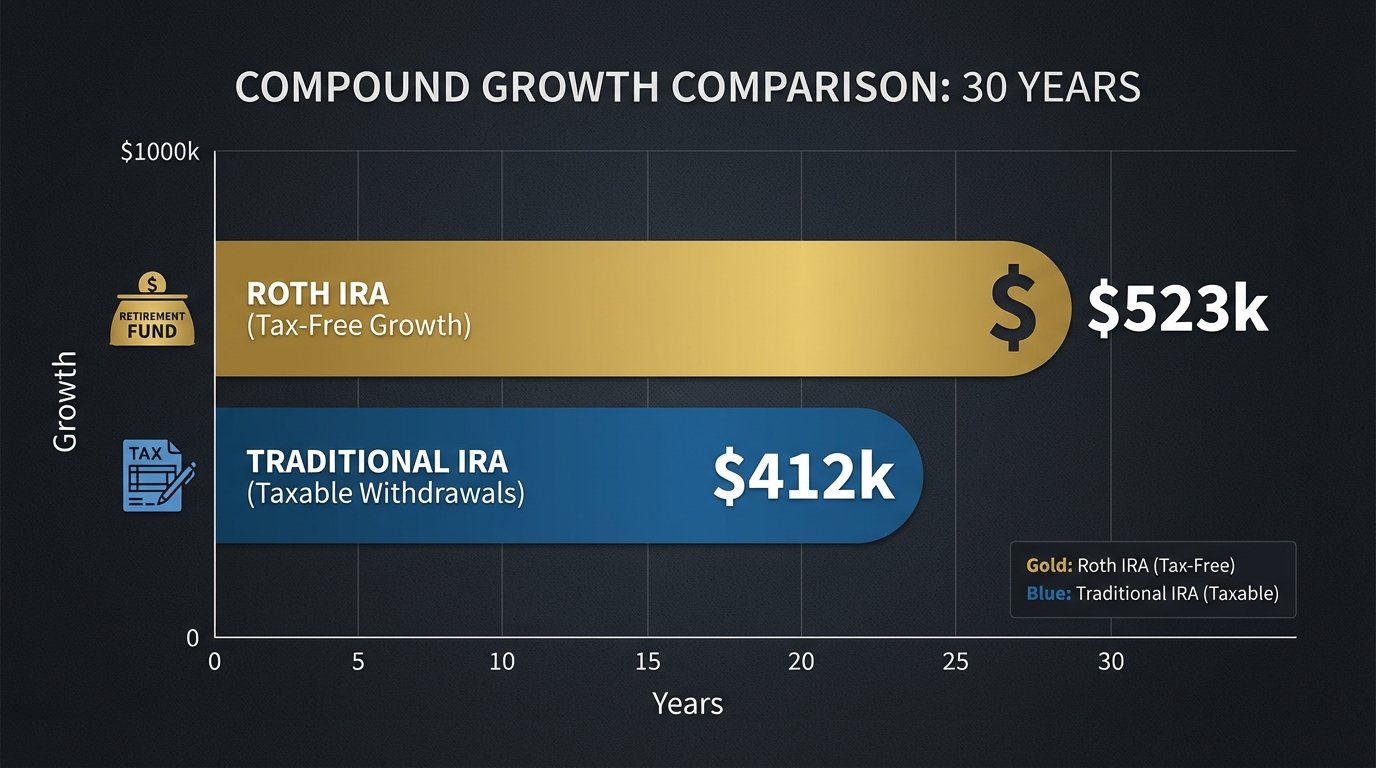

Assume a 34-year-old Millennial earning $75,000, in the 22% federal marginal bracket, contributing $7,000 per year for 30 years at 7% growth:

| Scenario | Roth IRA | Traditional IRA (22% now, 22% retirement) |

|---|---|---|

| Annual contribution | $7,000 after-tax | $7,000 pre-tax (saves $1,540/yr in taxes now) |

| Account value at 65 (7% growth) | ~$661,000 | ~$661,000 |

| Tax on withdrawal | $0 (tax-free) | 22% x $661,000 = ~$145,420 total |

| Net spendable in retirement | ~$661,000 | ~$515,580 |

| If tax savings are reinvested annually | N/A | If $1,540/yr reinvested at 7%: +~$146K |

When tax rates are identical, the accounts produce mathematically equivalent outcomes — only if you reinvest the Traditional IRA’s annual tax deduction savings. Most people don’t. They spend the refund.

Now adjust for reality: most Millennials are currently in the 22% bracket but will likely retire in the 24–32% bracket as TCJA provisions expire after 2025 and peak earning years push income higher. In that scenario, the Roth IRA wins decisively.

There is also the RMD factor. When Social Security runs out, retirees will lean harder on personal accounts — but Traditional IRA holders face Required Minimum Distributions beginning at age 73, which can push them into higher brackets precisely when they can least afford it. The Roth IRA has no RMDs during the owner’s lifetime.

When a Roth IRA Is the Right Call for Millennials

The Roth IRA is almost certainly the better choice for Millennials in these situations:

- You’re in the 22% or lower federal bracket now. Rates will almost certainly be higher for you in retirement, either because you earn more or because Congress raises baseline rates.

- You expect tax rates to rise generally. The TCJA individual provisions expire after 2025. Default reversion means the 22% bracket becomes 25% and the 24% bracket becomes 28%. A Roth contribution made at 22% and withdrawn at 28% is a guaranteed winner.

- You want flexibility on early withdrawals. Roth IRA contributions (not earnings) can be withdrawn at any time, penalty-free. This makes the Roth IRA a dual-purpose account — retirement savings plus emergency backstop.

- You want to avoid RMDs. No required minimum distributions during your lifetime means the Roth IRA can compound untouched for decades longer if you don’t need it.

- You’re early career and expect significant income growth. Locking in the 22% rate now beats paying 32% on the same dollars in 15 years.

The broken retirement picture for this generation is documented exhaustively. Social Security benefit cuts by birth year are coming. Social Security Disability has a catastrophic backlog that leaves the most vulnerable workers exposed. Most employers no longer offer defined benefit pensions. The Roth IRA is not a solution to any of that. But it is the best tax-efficient vehicle available under current law for a Millennial who can afford to max one out.

When a Traditional IRA Makes More Sense

The Traditional IRA wins in a narrower set of circumstances:

- You’re in the 32% bracket or higher right now and expect to retire on a lower income. A surgeon, attorney, or senior tech worker at peak earnings planning to retire on $100,000/year is in exactly this situation.

- You don’t have a workplace retirement plan and are below the deductibility phase-out threshold. You get a current-year deduction with immediate cash value.

- You need the current-year tax reduction urgently and can’t afford to lock up after-tax dollars. The deduction helps cash flow now, even if it costs more later.

- Your state has no income tax and you’re moving to a no-income-tax state in retirement.

“The Early Withdrawal Penalty on Traditional IRA distributions before age 59½ is 10% on top of ordinary income taxes — effectively turning a retirement account into a trap for Millennials who might need that money during the next economic crash before they ever reach retirement age.”

The 401(k) early withdrawal penalty functions similarly. The real-world cost of these penalties falls disproportionately on Millennials, who are statistically more likely to cash out retirement accounts during financial emergencies than older generations who have had more time to build liquid savings.

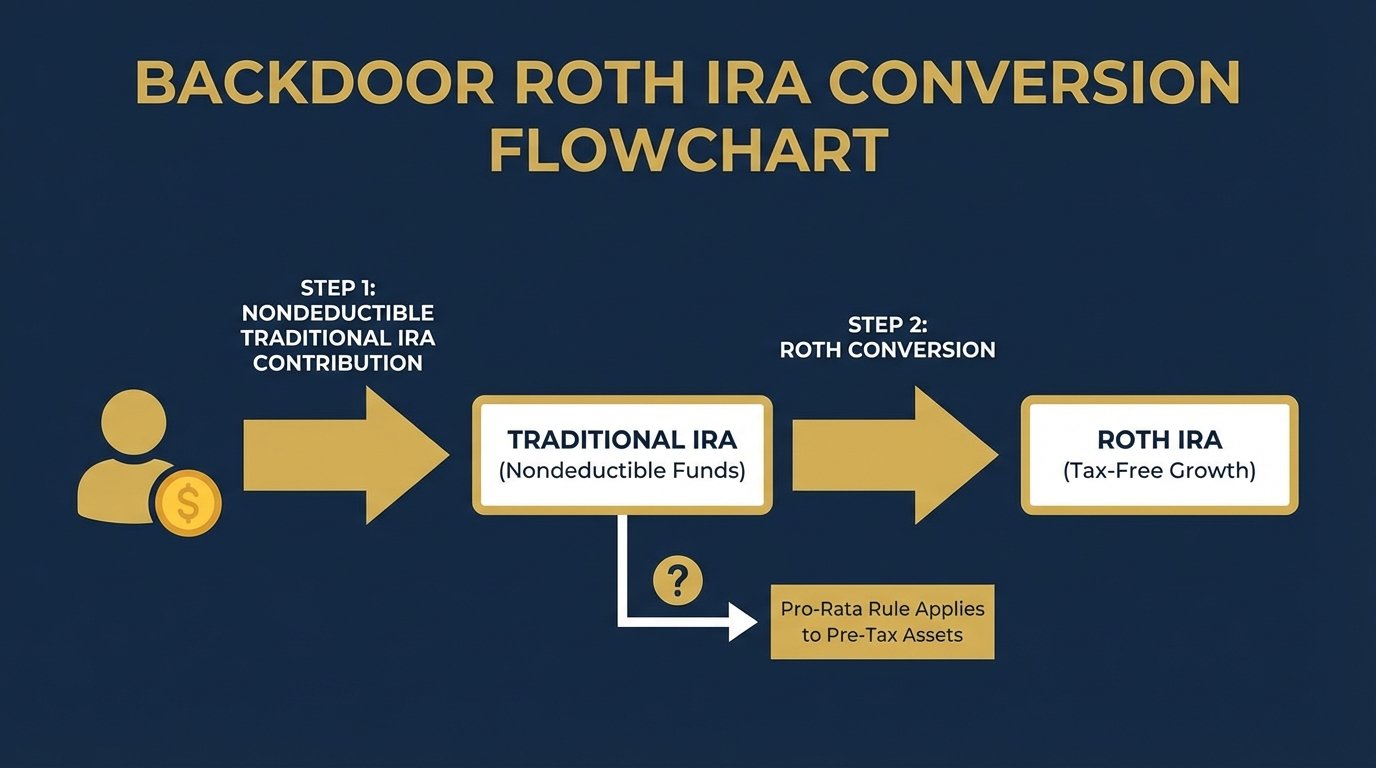

The Backdoor Roth IRA: What It Is and How It Works

The backdoor Roth IRA is a two-step workaround for high-income earners who exceed the Roth IRA’s direct contribution income limits. The IRS has explicitly acknowledged this strategy is permissible since 2010. It is not a loophole or gray area — it is a documented legal strategy.

| Step | Action | Details |

|---|---|---|

| 1 | Make a nondeductible Traditional IRA contribution | Contribute up to $7,000 to a Traditional IRA. No income limit applies to contributions, only to deductibility. |

| 2 | Convert to Roth IRA | Request a Roth conversion. Since the contribution was nondeductible (after-tax), the conversion is tax-free if there are no pre-tax funds in any Traditional, SEP, or SIMPLE IRA. |

| Key Warning | The Pro-Rata Rule | If you have other pre-tax IRA money anywhere, the IRS aggregates all IRA balances. The after-tax basis is prorated across the total, and you may owe taxes on part of the conversion. |

The Pro-Rata Rule is the landmine. A Millennial with $80,000 sitting in a rollover Traditional IRA from a previous employer cannot cleanly do a backdoor Roth without tax consequences. The workaround: roll pre-tax IRA funds into a current employer’s 401(k) (if the plan accepts rollovers) to clear the pro-rata denominator before the conversion.

Roth 401(k) vs Roth IRA: What’s the Difference?

Many Millennials have access to a Roth 401(k) through their employer. Both offer tax-free growth and withdrawals, but the mechanics differ significantly:

| Feature | Roth IRA (2026) | Roth 401(k) (2026) |

|---|---|---|

| Contribution limit | $7,000 / $8,000 catch-up | $23,500 / $31,000 catch-up (age 50+) |

| Income limit to contribute | Yes (phase-out at $150K single) | No income limit |

| Investment options | Any brokerage (broad menu) | Limited to employer plan menu |

| Required Minimum Distributions | None during owner’s lifetime | Starting age 73 (roll to Roth IRA to avoid) |

| Early withdrawal of contributions | Penalty-free anytime | Plan rules apply, harder access |

| Employer match available | No | Yes (but match is pre-tax) |

The optimal strategy for most Millennials: contribute enough to the 401(k) to capture the full employer match, then max the Roth IRA for its flexibility and investment menu, then return to the Roth 401(k) for any remaining retirement savings budget.

Counter-Argument: Does the Tax Bet Even Matter?

There is a legitimate counterargument to Roth IRA maximalism worth taking seriously.

The case for Traditional IRA: Predicting future tax rates is genuinely uncertain. Congress has changed the tax code 13 times since 1987. Assuming today’s law persists for 30 years is not conservative planning — it’s guessing. A Traditional IRA deduction today has certain, immediate value. A Roth IRA’s tax-free promise depends on Congress not deciding to tax Roth withdrawals sometime between now and 2055.

The counter-counterargument: The Roth IRA has strong political protection because it holds trillions in accumulated middle-class savings. Retroactively taxing Roth withdrawals would be a political catastrophe. Traditional tax increases on ordinary income are far more politically feasible than a targeted attack on the one retirement account designed to benefit middle-income savers.

Bottom line: For Millennials currently in the 22% bracket or below, the Roth IRA is mathematically superior under any plausible scenario where rates stay flat or rise. The Traditional IRA wins only if rates drop significantly — unlikely given current deficit trajectories and the TCJA expiration clock. As the public pension crisis demonstrates, governments chronically underfund long-term obligations, which historically correlates with higher future tax rates, not lower ones.

Frequently Asked Questions

Can I have both a Roth IRA and a Traditional IRA?

Yes. You can contribute to both in the same year, but your total combined contributions cannot exceed $7,000 ($8,000 if 50 or older) for 2026.

What happens to a Roth IRA if I die before withdrawing?

Roth IRA assets pass to designated beneficiaries without going through probate. Inherited Roth IRAs are generally tax-free to beneficiaries, though the SECURE Act 2.0 requires most non-spouse beneficiaries to withdraw all funds within 10 years of the original owner’s death.

Is a Roth IRA the same as a Roth 401(k)?

No. A Roth IRA is an individual account opened at a brokerage with a $7,000 limit and income phase-outs. A Roth 401(k) is a designated option within an employer’s 401(k) plan, with a $23,500 limit and no income restrictions.

Can I contribute to a Roth IRA if I already have a 401(k) at work?

Yes. Having a 401(k) at work does not affect your ability to contribute to a Roth IRA. The only restriction is the Roth IRA income phase-out: above $165,000 single or $246,000 married in 2026, you cannot contribute directly. The backdoor Roth is the standard workaround above those thresholds.

Sources & Methodology

Contribution limits and phase-out figures sourced from IRS Publication 590-A (2026) and IRS IR-2025-225. Tax bracket projections based on Tax Foundation TCJA expiration analysis. Millennial retirement savings statistics from Vanguard How America Saves 2024 and Federal Reserve Z.1 Financial Accounts. Backdoor Roth IRA rules per IRS FAQs on Rollovers and Roth Conversions.