Social Security benefit cuts by birth year are already happening — not as a future possibility, but as a legislated reality that has been quietly reducing what younger workers will receive compared to what Boomers collected. Workers born in 1960 or later face a full retirement age of 67, which reduces their lifetime benefit by roughly 13% compared to those born before 1943 who could claim full benefits at 65. If the Social Security trust fund reaches insolvency in 2033 as projected, an additional automatic cut of approximately 21-23% hits every current and future beneficiary — with the youngest workers bearing the longest exposure.

Key Takeaways: (1) The 1983 Social Security reform legislated benefit cuts by birth year by raising the Full Retirement Age from 65 to 67 for those born 1960 or later. (2) This represents a 13.3% reduction in lifetime benefits for the youngest workers vs. the oldest Boomers. (3) The OASI Trust Fund is projected to be depleted by 2033, triggering an automatic 21% across-the-board cut under current law. (4) Millennials will pay into Social Security for 40+ years before facing both a higher FRA and a potentially insolvent fund. (5) Congress has not passed any Social Security reform legislation since 1983 — 43 years of deliberate inaction.

What Are Social Security Benefit Cuts by Birth Year?

The phrase “Social Security benefit cuts by birth year” refers to two distinct mechanisms that reduce lifetime Social Security income for workers born in later years relative to those who preceded them. The first is the legislated increase in the Full Retirement Age (FRA) — the age at which you can claim 100% of your earned benefit. The second is the looming trust fund insolvency, which if unaddressed by Congress will automatically trigger a benefit reduction for every recipient regardless of age. Together, these two mechanisms represent the largest generational transfer of retirement risk in American history — executed over four decades in near-total political silence.

The millennial retirement savings crisis cannot be understood without understanding this foundation: younger workers are not just saving less than their parents did — they are simultaneously paying full payroll taxes into a system that has already legislated smaller returns for them and may deliver further reductions before most of them reach retirement age. The Social Security insolvency timeline covered previously on this site establishes the trust fund mechanics — this article focuses specifically on how benefit reduction is distributed by birth year.

The 1983 Social Security Amendments — passed by a bipartisan commission chaired by Alan Greenspan and signed by President Reagan — were the last major Social Security reform in American history. That legislation set in motion a 22-year phased increase in the FRA, from 65 to 67, that did not fully take effect until 2027 (for workers born in 1960 and later). What that means in practice: a worker born in 1943 could claim 100% of their earned benefit at 65. A worker born in 1960 cannot claim that same 100% until age 67. Same payroll taxes, same contribution rate, meaningfully different return.

“Raising the Full Retirement Age is a benefit cut. There is no other accurate way to describe it. If you paid for something your entire working life and receive less of it than the person ahead of you did, that is a reduction — regardless of what the legislation calls it.” — Economic Policy Institute, 2019

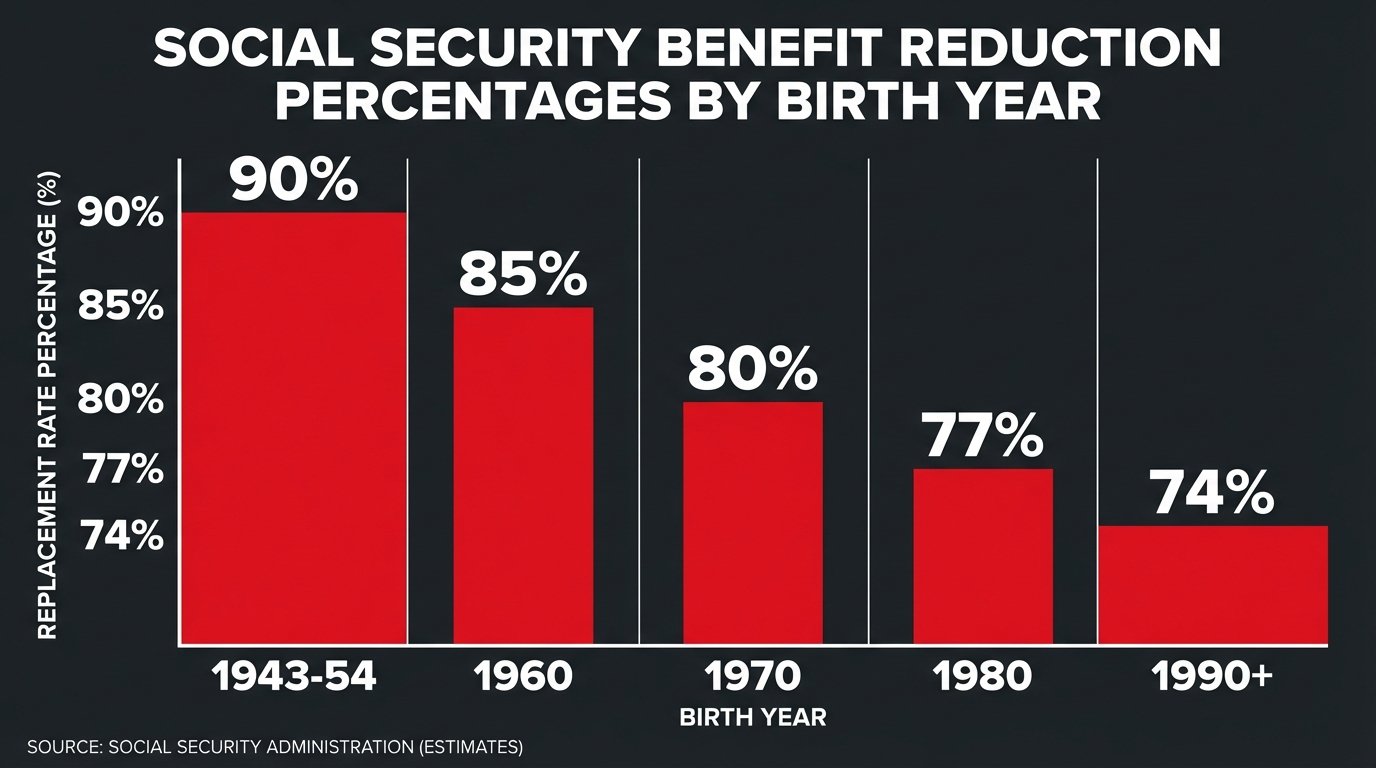

The Full Replacement Rate Table: What Every Birth Year Actually Gets

The following table shows the Social Security benefit cuts by birth year as implemented through the FRA schedule and the early claiming penalty structure. The “replacement rate” refers to the percentage of pre-retirement income that Social Security replaces for an average earner claiming at their FRA.

| Birth Year | Full Retirement Age | Benefit at Age 62 | Benefit at FRA | Notes |

|---|---|---|---|---|

| 1943–1954 | 66 | 75% of FRA benefit | 100% | Boomers — original deal |

| 1955 | 66 + 2 months | 74.2% | 100% | FRA phase-in begins |

| 1956 | 66 + 4 months | 73.3% | 100% | |

| 1957 | 66 + 6 months | 72.5% | 100% | |

| 1958 | 66 + 8 months | 71.7% | 100% | |

| 1959 | 66 + 10 months | 70.8% | 100% | |

| 1960+ | 67 | 70% | 100% | Gen X, Millennials, Gen Z — new floor |

The table above shows the FRA schedule as written in law. But the real Social Security benefit cuts by birth year picture is more severe than the FRA column alone suggests. Social Security benefits are calculated using the Average Indexed Monthly Earnings (AIME) formula, which applies bend points that change annually. Combined with the FRA increase, the Social Security Administration’s own actuarial data shows that workers born in 1960 receive a lifetime benefit approximately 13.3% lower than workers born in 1937 — assuming identical earnings histories and the same claiming age relative to FRA.

The compounding effect is significant. Someone born in 1960 who claims at 62 receives 70% of their FRA benefit — down from the 80% that 1943-born workers received for the same early claim. That 10-percentage-point difference, over a 20-year retirement, represents tens of thousands of dollars in cumulative lost income. For the generation least likely to inherit significant wealth, that gap is not abstract. It is the difference between covering rent and not covering rent in a retirement that may last 25-30 years.

Why the Full Retirement Age Was Raised — and Who Decided

The 1983 Greenspan Commission that designed the FRA increase operated under a stated rationale of “system solvency” — the same framing that every Social Security cut has used since. The Commission was responding to a genuine short-term funding crisis in 1982-83, when the trust fund was projected to be unable to pay benefits within months. The solution they chose was a combination of benefit cuts (the FRA increase) and revenue increases (higher payroll taxes, taxation of benefits for high earners). The payroll tax increases took effect immediately. The FRA increase was phased in over decades — timed so that the people making the decision in 1983 would bear essentially none of its cost.

The average age of a member of Congress in 1983 was 50. Workers born in 1960, who would bear the full impact of the FRA increase, were 23 years old — not yet in Congress, not yet economically powerful, and without significant political representation in the room where the decision was made. This is not a fringe interpretation. The Social Security Administration’s own history of the 1983 reforms acknowledges that “future beneficiaries would bear a greater share of the burden.” The AARP’s role in shaping Social Security politics since 1983 has consistently prioritized protecting current beneficiaries over restructuring the system to treat younger workers equitably.

“The 1983 reforms solved a short-term crisis by creating a long-term one. The people who voted for it were insulated from its consequences. The people who will bear its consequences had no vote. That is not a design flaw. That is the design.”

The public pension crisis follows an identical pattern: decisions made by older politicians with short time horizons, costs deferred to younger workers and taxpayers. The 401(k) replacement of pensions happened in the same era, also benefiting those closest to retirement while shifting market risk onto younger workers who had decades of compounding exposure ahead of them.

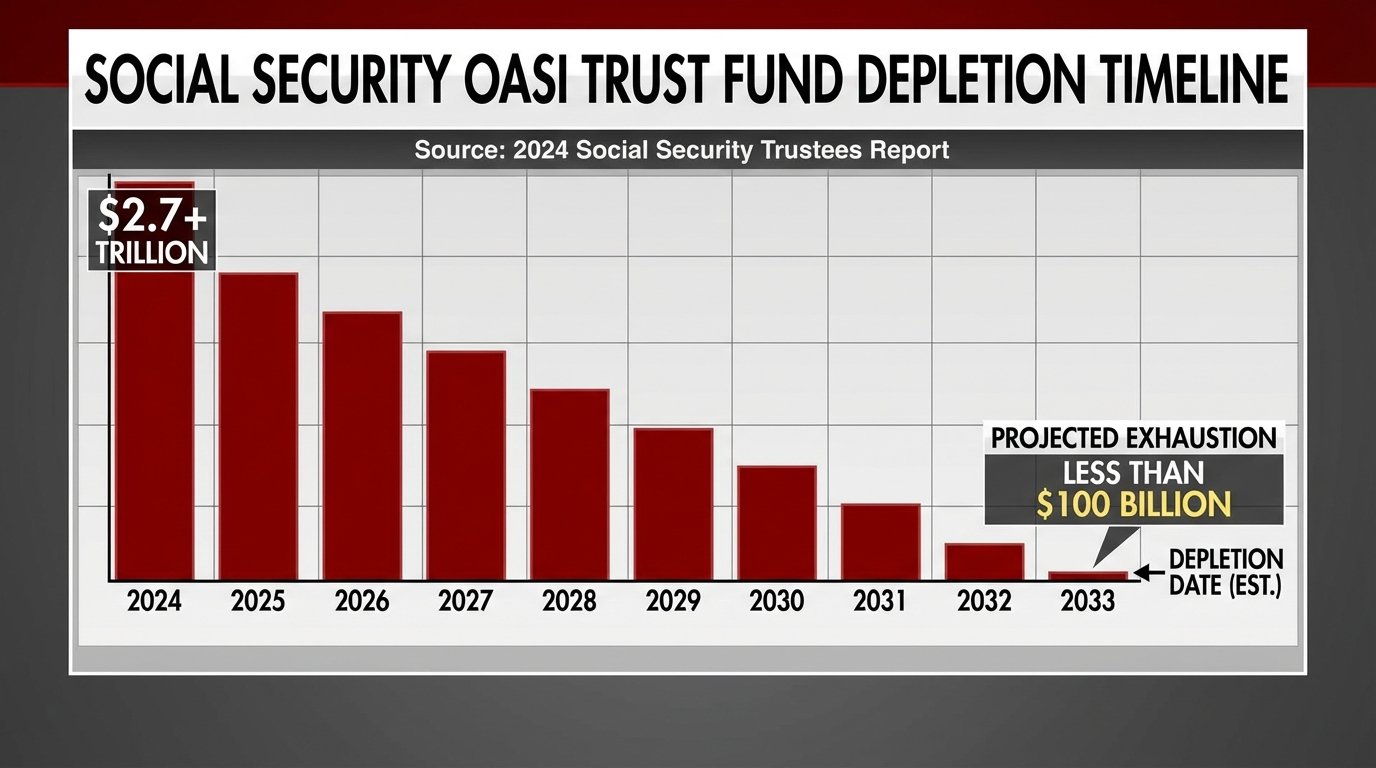

The Trust Fund Crisis: What Happens After 2033

The Social Security benefit cuts by birth year already legislated through the FRA increase are a certainty. The trust fund crisis is a probability that is approaching certainty with each passing year of Congressional inaction. Here is what the data actually shows.

The Social Security OASI (Old-Age and Survivors Insurance) Trust Fund is projected by the SSA’s 2025 Trustees Report to be depleted by 2033. Under current law, when the trust fund is exhausted, Social Security does not shut down — it can continue paying benefits from incoming payroll tax revenue. The problem is that incoming revenue will only cover approximately 77-79% of scheduled benefits at that point. The result, absent Congressional action, is an automatic across-the-board benefit cut of approximately 21-23% for every current and future recipient.

The distributional impact of this automatic cut is where the Social Security benefit cuts by birth year picture becomes most alarming for younger workers. A worker born in 1955 who retires in 2022 will have been collecting benefits for 11 years before the trust fund depletes — their exposure to the automatic cut is limited. A worker born in 1990 who plans to retire in 2057 will not have begun collecting at all when the trust fund depletes — meaning they face the full FRA increase AND the trust fund cut for the entirety of their retirement. The same payroll taxes. Significantly smaller expected return. No political representation when either decision was made.

The current stagflation environment created by the Iran War is accelerating the trust fund timeline. Wage growth softens payroll tax revenue. Higher unemployment (92,000 jobs lost in February 2026) means fewer workers paying into the system. The 2026 Trustees Report, when released, is expected to move the depletion date earlier, not later — for the first time since 2020.

“Under the intermediate assumptions, the combined OASI and DI Trust Fund reserves are projected to become depleted in 2035… At the point of depletion, there would be sufficient income coming in to pay 83 percent of scheduled benefits.” — 2024 SSA Trustees Report (2025 report expected to revise this earlier)

What Younger Workers Can Actually Do

The Social Security benefit cuts by birth year are largely outside individual workers’ control. Congress set the FRA schedule. Congress has failed to address the trust fund for 43 years. The political economy of Social Security reform — where current beneficiaries vote in high numbers and future beneficiaries do not yet have the same political weight — has made structural reform nearly impossible. What younger workers can actually do falls into two categories: individual financial mitigation and political action.

Individual mitigation

- Treat Social Security as a floor, not a plan. Younger workers should assume they will receive approximately 70-79% of currently projected benefits — not the full amount. Building supplemental retirement savings to cover that gap is the only reliable hedge against Congressional inaction

- Maximize the Roth IRA window now. Roth accounts are not subject to Social Security’s political risk. For workers in their 20s and 30s, maximizing Roth IRA contributions ($7,000/year in 2026, $8,000 if over 50) provides tax-free income in retirement that is completely independent of whatever Congress does to Social Security

- Understand your actual projected benefit. The SSA’s online portal (ssa.gov/myaccount) shows your current projected benefit at every claiming age based on your actual earnings history. The numbers shown are based on current law — meaning they do not yet reflect any trust fund depletion cut. Reduce those numbers by 21% to model the realistic worst-case scenario

- Delay claiming if at all possible. Every year you delay claiming Social Security beyond your FRA increases your benefit by 8% — up to age 70. For younger workers with potentially 30+ year retirements, delaying from 67 to 70 increases the base benefit by 24% — a significantly better return than most financial instruments, and a partial offset against the generational reduction built into the FRA schedule

Political action

The wage stagnation that has compressed payroll tax revenue is a structural problem requiring structural solutions. The most straightforward fix to Social Security’s funding gap — lifting or eliminating the payroll tax cap, which currently exempts all income above $168,600 (2024) from Social Security taxation — would close the funding gap entirely according to CBO modeling without touching benefits for any current or future recipient. This solution has been blocked for 40 years by exactly the political forces the AARP lobbying analysis documents in detail. The gap between what is technically possible and what gets passed is entirely a function of whose votes are being counted.

Counter-Argument: Is Social Security Really in Crisis?

The standard counterargument to the Social Security benefit cuts by birth year framing is that the system has faced insolvency projections before and Congress has always acted — as in 1983. This is true. It is also a reason for measured concern, not comfort, because the 1983 solution was itself a benefit cut distributed disproportionately onto younger cohorts. “Congress will fix it” is not a reassuring statement when the last fix took something away from you.

A second counterargument holds that the FRA increase is justified by longer average life expectancies — if people are living longer, they should work longer. This argument has two significant problems. First, life expectancy gains since 1983 have been heavily concentrated in higher-income workers — lower-income workers, who are disproportionately Millennial and Gen Z, have seen much smaller longevity improvements and in some demographics actual declines (opioid crisis, COVID-19, despair deaths). Second, the physical demands of work are not evenly distributed: a 67-year-old knowledge worker can keep working; a 67-year-old construction worker, home health aide, or warehouse fulfillment employee may not be physically capable of doing so.

The strongest honest counterargument is that the projected trust fund depletion is a projection, not a guarantee — modest economic growth above baseline assumptions could push the depletion date further out. This is true. It is also true that projections have been revised earlier, not later, in every recent Trustees Report, and that the current macroeconomic environment (stagflation, job losses, Iran war costs) is unambiguously negative for the trust fund timeline.

FAQ

How much will Social Security be cut by birth year?

Workers born in 1960 or later already face a Social Security benefit cut by birth year of approximately 13.3% in lifetime benefits compared to those born before 1943, due to the Full Retirement Age being raised from 65 to 67. If the OASI Trust Fund is depleted in 2033 without Congressional action, an additional automatic cut of approximately 21% applies to all beneficiaries. Younger workers who retire after 2033 would bear the full impact of both reductions.

Will Millennials get Social Security?

Almost certainly yes — Social Security does not “go bankrupt” in the way a company does. When the trust fund is depleted, the program continues paying benefits from incoming payroll tax revenue, covering approximately 79% of scheduled benefits. The question is not whether Millennials will receive Social Security but how much they will receive relative to what was promised and what Boomers collected. The answer, under current law plus trust fund depletion, is substantially less than the generation before them.

What is the Full Retirement Age for someone born in 1970?

Someone born in 1970 has a Full Retirement Age of 67. They can claim early at 62 and receive 70% of their FRA benefit, or delay until 70 and receive 124% of their FRA benefit. This compares to someone born in 1943, who could claim full benefits at 65 and received 80% if claiming at 62. The Social Security benefit cut by birth year for someone born in 1970 vs. 1943 is approximately 13% in lifetime terms at equivalent claiming age relative to FRA.

Can Congress fix Social Security without cutting benefits?

Yes. The Congressional Budget Office has modeled multiple approaches that close the Social Security funding gap without benefit cuts. The most significant is eliminating or raising the payroll tax cap — currently set at $168,600 (2024), meaning no Social Security tax is paid on income above that level. Removing the cap entirely would close approximately 74% of the 75-year funding shortfall. Combining that with modest adjustments to the benefit formula for high earners would close it entirely. These solutions exist. They require political will that has been unavailable for 43 consecutive years.

Sources & Methodology

All benefit replacement rate figures sourced from the Social Security Administration’s Benefit Calculation page and the SSA’s historical FRA schedule. Trust fund depletion projections from the 2024 Social Security Trustees Report. Lifetime benefit reduction comparisons sourced from the Economic Policy Institute’s analysis of FRA increases. Payroll tax cap data from the SSA’s contribution and benefit base schedule. CBO cap-removal modeling from CBO Options for Reducing the Deficit 2021-2030. February 2026 jobs report employment figures from the Bureau of Labor Statistics.