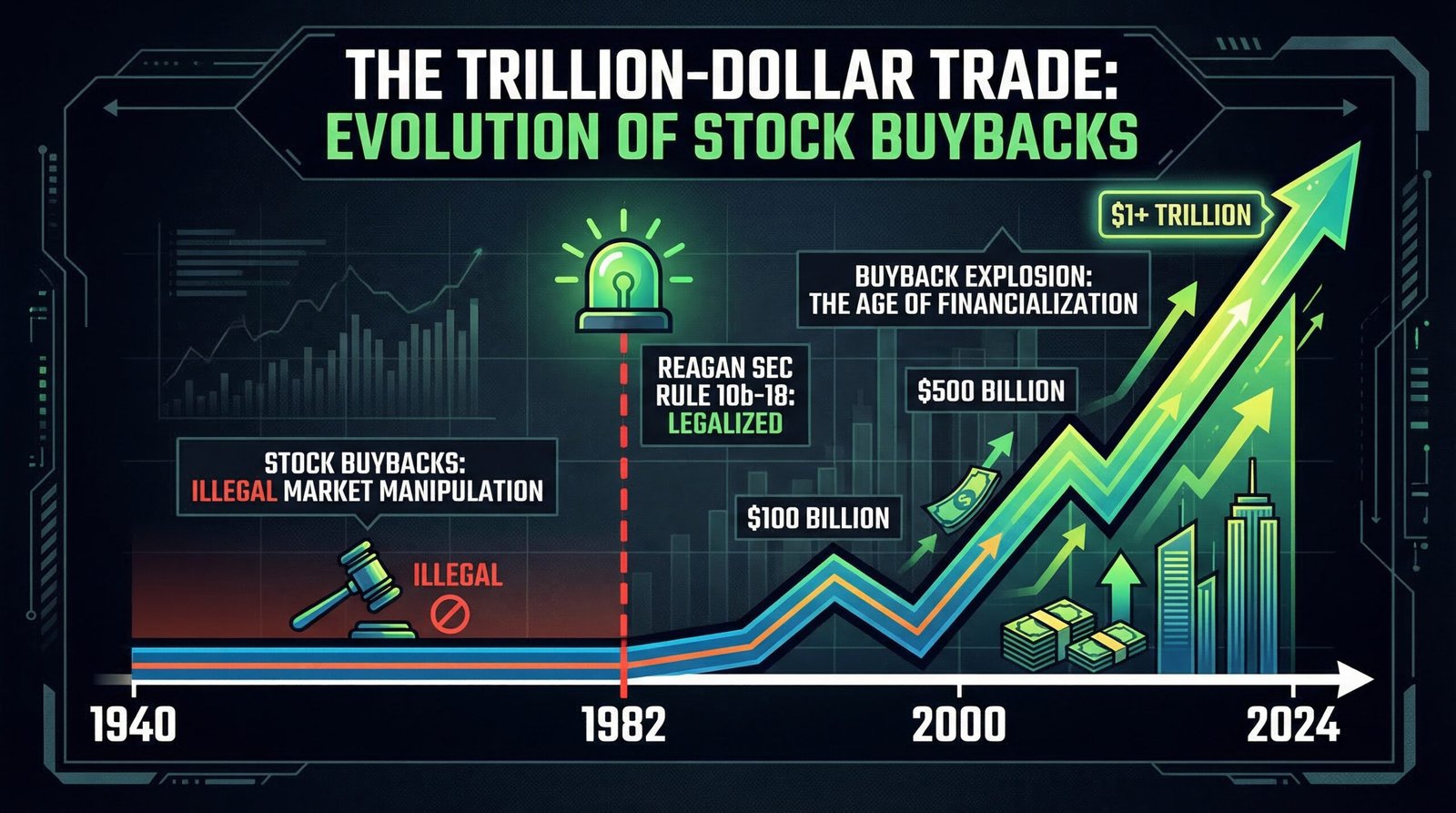

Stock buybacks — when corporations repurchase their own shares on the open market — were classified as illegal stock market manipulation by the SEC for most of the 20th century. The Reagan administration legalized them in 1982 via SEC Rule 10b-18. Since then, S&P 500 companies have spent trillions redirecting corporate profits away from workers, capital investment, and R&D and into share price inflation that benefits executives and wealthy shareholders. In 2024, U.S. corporations set an all-time annual record of $942.5 billion in stock buybacks — up from $6.6 billion in 1980. The top 10% of Americans own 93% of all stocks, meaning the windfall is almost entirely captured by people who were already wealthy. The bottom 50% of Americans own just 1% of equities.

Key Takeaways

- Stock buybacks were considered illegal stock market manipulation by the SEC before 1982. The Reagan administration’s SEC created a legal “safe harbor” via Rule 10b-18. Buyback volume tripled within the first year of the rule’s adoption.

- S&P 500 companies spent $942.5 billion on stock buybacks in 2024 — an all-time annual record, up 18.5% from 2023. In 2025, announced buybacks hit $1.38 trillion — another record. Total shareholder returns (buybacks + dividends) reached $1.685 trillion for the 12 months ending September 2025.

- Apple spent $104.2 billion on buybacks in 2024 alone — following its $110 billion announcement, the largest single buyback in corporate history. Boeing spent $43 billion on buybacks between 2013 and 2019 — more than its total profits during that period — while gutting the engineering investment that preceded two 737 MAX crashes.

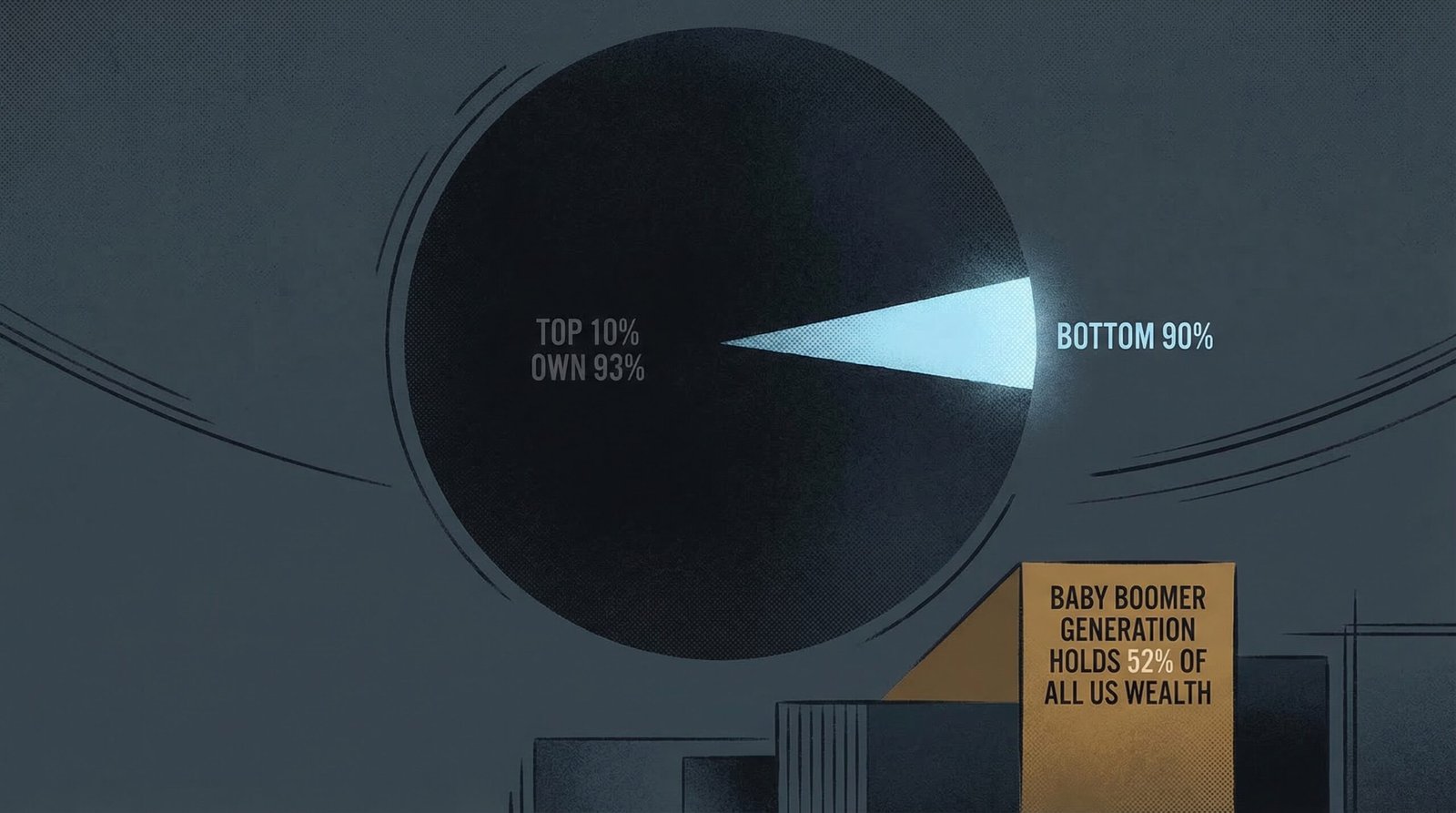

- The top 10% of Americans own 93% of all U.S. stocks. The bottom 50% own 1%. Baby Boomers hold 52% of total U.S. wealth. Stock buybacks are a machine for concentrating already-concentrated wealth further.

- Buybacks mechanically inflate Earnings Per Share (EPS) by reducing share count — and since executive compensation is heavily tied to EPS and stock price, CEOs have a powerful financial incentive to authorize buybacks. SEC data showed executives sold an average of $500,000 per day in stock immediately following buyback announcements, versus less than $100,000 before.

- The 100 largest low-wage S&P 500 employers spent $522 billion on buybacks over five years — nearly half spent more on buybacks than on long-term capital investment. Lowe’s alone spent $43 billion while paying a median worker less than $33,000/year and a CEO $18 million.

- Congress passed a 1% excise tax on buybacks in the Inflation Reduction Act (2022). Reformers called for 4%. The lobbying response to even the 1% tax was immediate and intense. In January 2026, Trump banned buybacks for large defense contractors — the first federal buyback restriction — but only for Pentagon contractors, not the broader economy.

Why Were Stock Buybacks Illegal Before 1982?

For most of the 20th century, the Securities and Exchange Commission treated corporate stock buybacks as a form of illegal stock market manipulation. The logic was straightforward: when a company purchases its own stock on the open market, it is using its financial resources to artificially inflate the price of that stock. That is, by definition, market manipulation — and it was regulated as such under the Securities Exchange Act of 1934, enacted in direct response to the stock manipulation schemes that helped ignite the 1929 crash.

The regulatory landscape changed in November 1982, when the Reagan-era SEC adopted Rule 10b-18. The rule created a legal “safe harbor” that allowed corporations to repurchase their own shares without triggering market manipulation liability, provided they followed specific conditions: use a single broker per day, limit purchases to the last 10 minutes of trading, cap the price at the highest independent bid, and limit daily volume to 25% of average daily trading volume. As long as a company followed those parameters, it was protected from SEC enforcement.

The effect was immediate. Buyback volume tripled within the first year after Rule 10b-18 was adopted. In 1980 — before the rule — U.S. corporations spent $6.6 billion on buybacks. By 2000, the figure had grown to approximately $200 billion. By 2018, S&P 500 companies announced a record $1.08 trillion in repurchases in a single year. By 2024, actual executed buybacks hit $942.5 billion.

The rule was not a response to any demonstrated market need or economic evidence that buybacks improved corporate performance. It was a deregulatory act consistent with the broader Reagan-era philosophy that corporations should face fewer constraints on how they used their capital. The Glass-Steagall repeal followed the same logic 17 years later. So did the gutting of the CFPB decades after that. The pattern is consistent: deregulate capital allocation, privatize the gains, socialize the eventual costs.

Rule 10b-18 has never been repealed. It has been amended once, in 2003, to add disclosure requirements. The safe harbor it created — the legal permission to do what was previously classified as market manipulation — remains in full effect in 2026.

How Much Money Are Corporations Spending on Stock Buybacks?

The scale of stock buyback spending defies intuitive comprehension. In 2024, S&P 500 companies executed $942.5 billion in repurchases — the highest annual total ever recorded, up 18.5% from 2023’s $795.2 billion. Combined with dividends, S&P 500 companies returned nearly $1.6 trillion to shareholders in 2024 alone. By Q1 2025, the quarterly record was shattered at $293 billion — and full-year 2025 announced buybacks topped $1.38 trillion.

The individual corporate figures are staggering:

- Apple: $104.2 billion in buybacks in 2024, following a $110 billion repurchase announcement — the single largest buyback commitment in corporate history. Apple has spent over $800 billion on buybacks since the program began. For the 12 months ending March 2025, Apple alone spent $106.9 billion.

- Boeing: Spent $43 billion on buybacks between 2013 and 2019 — more than the company’s total profits during that period. In those same years, Boeing was cutting engineering staff, outsourcing safety oversight, and rushing the 737 MAX to market. Two 737 MAX crashes in 2018 and 2019 killed 346 people. The $43 billion did not go to safety engineering. It went to shareholders.

- Alphabet (Google): Launched a $70 billion+ buyback program in 2025. Microsoft and other tech giants collectively hold over $500 billion in cash reserves earmarked for future repurchases.

The Boeing case is worth dwelling on. The connection between corporate financialization and the degradation of actual product quality is not theoretical — it is a documented sequence. Boeing’s engineering culture did not collapse randomly; it was restructured by financial executives who prioritized shareholder returns over the investment required to safely design new aircraft. The 737 MAX was the result. The $43 billion in buybacks was the mechanism.

To put the $942.5 billion 2024 buyback figure in context: it is larger than the entire GDP of the Netherlands. It is roughly 14 times the total annual budget of the National Institutes of Health. It is approximately 4 times what the federal government spent on K-12 education in 2024. The money existed. The question was always who would receive it.

How Do Stock Buybacks Inflate Executive Compensation?

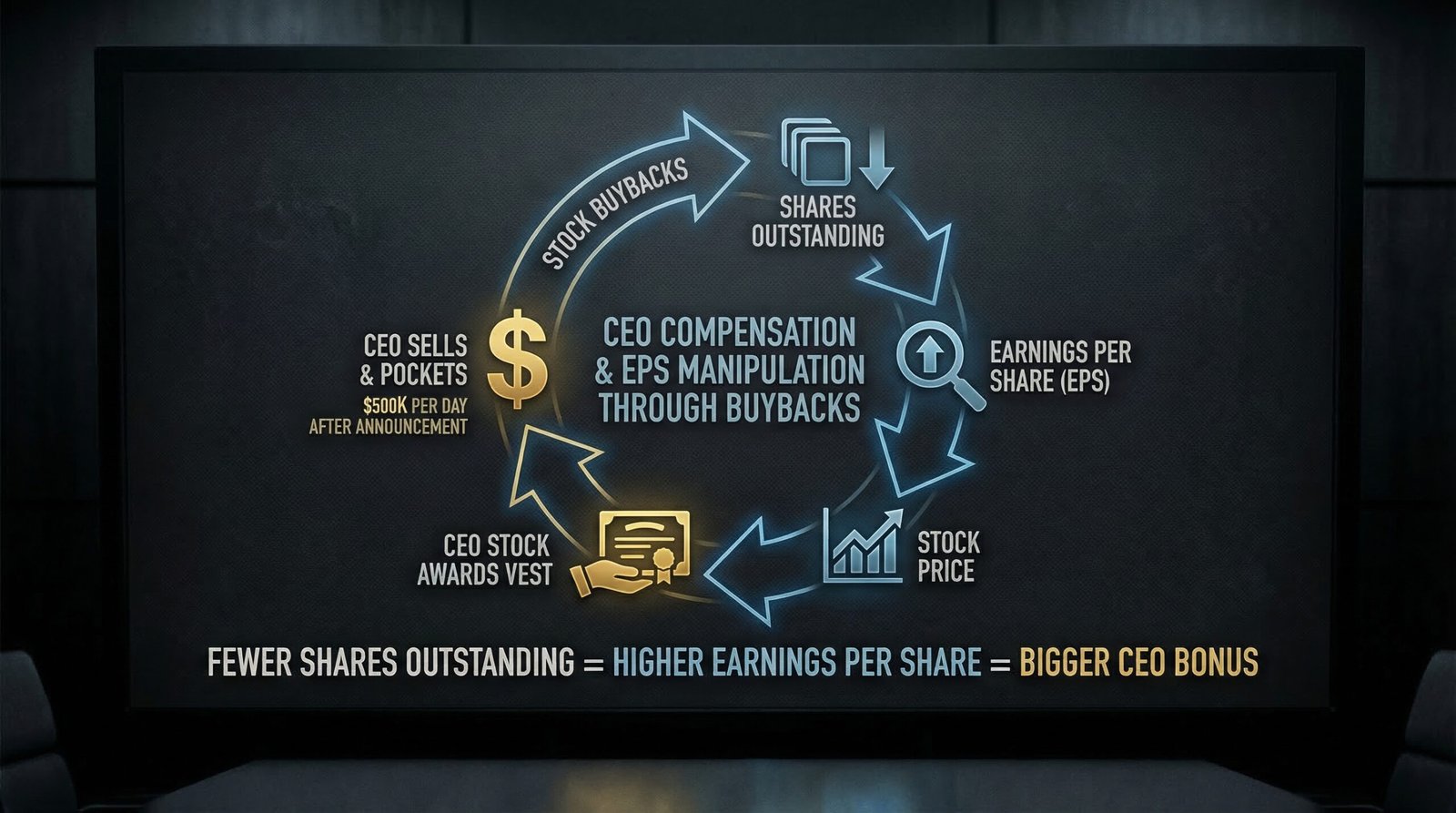

The structural connection between stock buybacks and executive pay is the most direct and least-discussed mechanism driving the practice. It works through Earnings Per Share — the metric that corporate boards have made central to executive compensation packages.

EPS = Net Income ÷ Shares Outstanding. When a company buys back its own shares, the denominator (shares outstanding) shrinks. Net income stays the same or may even decline — but EPS goes up. A company that earns $10 billion with 1 billion shares has $10 EPS. Buy back 100 million shares, and with the same earnings, EPS rises to $11.11 — an 11% improvement with zero improvement in actual business performance. Board compensation committees then award the CEO a performance bonus for “improving EPS.”

Between 36% and 47% of CEO compensation is now tied to performance-based equity awards, up from 22%–32% in 2010. EPS, total shareholder return, and stock price are the dominant metrics in those awards. The incentive structure is not subtle: CEOs who authorize large buybacks mechanically improve the metrics that determine their own compensation. This is not illegal under current law. It is, however, a straightforward conflict of interest that the SEC documented when it confirmed executives sold stock at approximately $500,000 per day in the period immediately following buyback announcements — versus less than $100,000 in the period before.

The Chipotle data point from the inequality.org report on low-wage employers illustrates the proportional absurdity. Chipotle spent $2 billion on buybacks over five years — 48 times more than it contributed to employee retirement plans. 92% of Chipotle’s eligible workers had zero 401(k) balances. The 401(k) retirement system was already a degraded substitute for pensions; these corporations couldn’t even be bothered to participate in it while redirecting billions to share price inflation.

The buyback-EPS-bonus cycle is self-reinforcing. Higher stock price increases the value of executive stock awards. Executives exercise those awards and sell. The stock’s float shrinks further. EPS metrics improve. Boards award new compensation tied to those improved metrics. Repeat annually. The only parties that benefit are those who own large amounts of the stock — executives and wealthy shareholders. Workers, communities, and long-term corporate health are all residual claimants at best.

Who Actually Benefits From Stock Buybacks?

The standard defense of stock buybacks is that they benefit shareholders — and therefore benefit all Americans who own stocks, including working-class 401(k) holders. That argument requires ignoring who actually owns stocks in America.

According to Federal Reserve data, the wealthiest 10% of Americans own 93% of all U.S. stocks — the highest concentration ever recorded. The bottom 50% of Americans own approximately 1% of equities. The wealthiest 1% alone hold 50% of the stock market. Stock ownership by working-class Americans is largely nominal: they may technically “own stocks” through a 401(k), but the median 401(k) balance for Americans approaching retirement is approximately $87,000 — a sum that generates roughly $290 per month in retirement income at a 4% withdrawal rate.

The generational overlay amplifies the inequality. Baby Boomers hold approximately 52% of total U.S. household wealth — and by extension, approximately 52% of equity wealth. Millennials hold approximately 9%. When a corporation spends $100 billion buying back stock, it is, by the arithmetic of who owns what, mostly enriching people who are already wealthy and already old. The Millennial 401(k) holder with $23,000 in their account receives a rounding-error benefit compared to the institutional investor and executive holding millions of shares.

The tax treatment compounds the advantage. Buybacks are taxed at the lower capital gains rate — 20% for high earners — rather than as ordinary income. Dividends receive similarly preferential treatment for qualified dividends. The capital gains preference means that the wealthiest shareholders capturing the largest buyback benefits pay lower effective tax rates than the workers those companies employ. Rule 10b-18 did not create this tax preference, but the two systems work together to concentrate wealth with remarkable efficiency.

What Could Corporations Have Done With the Money Instead?

The question of alternative uses for buyback capital is not speculative. The arithmetic is straightforward.

A report from inequality.org analyzed the 100 largest low-wage employers in the S&P 500 — companies including Walmart, Amazon, McDonald’s, Lowe’s, Dollar General, and similar household names — and found they collectively spent $522 billion on buybacks over five years. Nearly half of those companies spent more on buybacks than on long-term capital investment in plant, equipment, and technology during the same period.

The Lowe’s case: The company spent $43 billion on buybacks over five years (2019–2023). During the same period, the median Lowe’s worker earned below $33,000 annually, and CEO Marvin Ellison received $18 million per year. With the $43 billion spent on buybacks, Lowe’s could have given each of its 285,000 employees a $30,000 annual bonus for the entire five-year period — and had money left over. Instead, the $43 billion went to institutional investors and share price inflation.

At the macro level, Americans for Tax Fairness found that of $4.4 trillion spent on shareholder returns by major corporations, $2.7 trillion went to buybacks — 4.4 times more than those same corporations paid in income taxes over the same period. The corporations benefiting from public infrastructure, educated workforces, legal systems, and regulatory frameworks paid less in taxes than they spent buying back their own stock.

The Roosevelt Institute and NELP documented the direct trade-off in a report titled “Curbing Stock Buybacks: A Crucial Step to Raising Worker Pay and Reducing Inequality.” The research found that if the 20 largest low-wage S&P 500 companies had redirected just half their buyback spending to workers, it would have funded an average $18,000 annual wage increase for every employee — without requiring any new legislation or government spending. The money was there. The corporate decision about where to direct it was a choice, enabled by a 1982 regulatory change that nobody voted on.

The productivity-wage gap did not emerge from a vacuum. U.S. worker productivity increased by roughly 65% between 1979 and 2020; real wages for the median worker grew by approximately 11% over the same period. The gap between what workers produced and what they were paid went somewhere. A substantial portion of it went to stock buybacks and executive compensation that buybacks inflated. That is not a controversial finding — it is documented in peer-reviewed labor economics research and confirmed by the raw financial data.

What Has Congress Done About Stock Buybacks?

The legislative response to $942 billion in annual stock buybacks has been, charitably, underwhelming.

The Inflation Reduction Act of 2022 included a 1% excise tax on corporate stock buybacks — the first federal constraint on buybacks in the 40 years since Rule 10b-18. The Congressional Budget Office estimated the tax would generate approximately $74 billion over 10 years. Democrats had initially proposed a 2% or 4% rate; the final rate was 1%, reduced in negotiations. Corporate lobbying against even the 1% rate was intense and sustained. The tax did not reduce buyback activity — 2024 set an all-time record in the year after the tax took effect.

The Reward Work Act, introduced in the House multiple times, would prohibit buybacks entirely and require corporations to instead give workers representation on corporate boards. It has not received a floor vote.

In a notable development in January 2026, President Trump issued an executive order limiting stock buybacks and dividends for large defense contractors — the first actual buyback prohibition for any sector of the economy. The stated rationale was that defense contractors should be reinvesting profits in manufacturing capacity, workforce, and innovation rather than financial engineering. The Trump administration’s argument against buybacks for defense contractors was, word for word, the same argument critics have been making about the broader economy for two decades. The restriction applied exclusively to Pentagon contractors; no similar measure was proposed for the rest of corporate America.

The bipartisan congressional stock trading ban efforts in 2025 — separate from buyback reform — reflect the broader pattern: when the financial rules benefit insiders, reform is slow regardless of which party controls Congress. The revolving door between corporate finance and regulatory agencies has made Rule 10b-18 functionally permanent. The people who wrote the rule, benefited from it, and defend it are the same people who move between Wall Street and Washington. The rule that legalized a practice the SEC previously called market manipulation has survived nine presidencies.

The Counter-Argument: Stock Buybacks Are an Efficient Use of Capital

The mainstream economic defense of stock buybacks rests on capital efficiency theory. The argument: when a company has generated profits and has no higher-return investment opportunity available — no promising R&D pipeline, no accretive acquisition target, no facility expansion that would generate adequate returns — returning capital to shareholders is the economically correct decision. Shareholders can then redeploy that capital into other investments with better return profiles. In this framework, buybacks are not extraction but optimal capital allocation.

A related defense: buybacks are economically equivalent to dividends — both return cash to shareholders — but buybacks are more tax-efficient and give shareholders a choice (they can sell if they want the cash, or hold if they don’t). Forcing companies to pay dividends instead would be a less flexible mechanism for the same outcome.

Harvard Law School’s corporate governance research has also challenged some specific causal claims about buybacks and executive compensation, finding that while buybacks can affect EPS, the link between buybacks and executive pay manipulation is less mechanically direct than critics suggest, and that some of the EPS-gaming concerns are addressed by board compensation design.

Where the defense gets complicated:

The “no better investment available” premise does not survive scrutiny in most of the documented cases. Boeing had extensive, obvious reinvestment needs in engineering safety and aircraft development — and chose buybacks instead. Low-wage employers like Lowe’s and Chipotle could clearly have invested in worker compensation and retention (high turnover has documented costs) and instead chose buybacks. Apple, sitting on hundreds of billions in cash, is not a company with no investment opportunities — it is a company that concluded buybacks generated better short-term share price performance than any available alternative.

The capital efficiency argument also assumes frictionless capital redeployment: shareholders receive buyback proceeds and invest them in better-return opportunities. In practice, a substantial portion of buyback proceeds go to institutional investors and executives who hold the stock — not to workers, communities, or productive investment. The proceeds concentrate at the top of the wealth distribution and largely stay there.

FAQ: Stock Buybacks

Are stock buybacks legal?

Yes — since 1982. Prior to the Reagan administration’s SEC Rule 10b-18, stock buybacks were considered illegal stock market manipulation under the Securities Exchange Act of 1934. Rule 10b-18 created a legal safe harbor allowing corporations to repurchase their own shares within specific parameters (single broker, timing limits, price caps, 25% daily volume limit). The rule has never been repealed. A 1% excise tax on buybacks was added by the Inflation Reduction Act (2022), and defense contractors face additional restrictions under a January 2026 Trump executive order — but buybacks remain broadly legal.

How much did S&P 500 companies spend on stock buybacks in 2024?

S&P 500 companies spent $942.5 billion on stock buybacks in 2024 — an all-time annual record, up 18.5% from 2023’s $795.2 billion, according to S&P Dow Jones Indices. Combined with dividends, total S&P 500 shareholder returns were approximately $1.6 trillion in 2024. In 2025, the record was broken again: announced buybacks topped $1.38 trillion, and Q1 2025 alone set a quarterly record at $293 billion.

Do stock buybacks hurt workers?

The research shows a documented trade-off at low-wage employers. The 100 largest low-wage S&P 500 employers spent $522 billion on buybacks over five years while nearly half spent more on repurchases than on capital investment, according to inequality.org. The Roosevelt Institute and NELP found that redirecting half of major low-wage employers’ buyback spending could have funded $18,000 annual wage increases per employee. The 20 largest low-wage employers spent 9 times more on buybacks than on worker retirement contributions. The direct mechanism is not that buybacks take money from workers’ paychecks — it is that corporate profits that could have funded wages, benefits, or investment instead went to share price inflation.

Who benefits most from stock buybacks?

The top 10% of Americans own 93% of U.S. stocks. The bottom 50% own approximately 1%. When corporations return capital through buybacks, 93 cents of every dollar goes to the top wealth decile. Baby Boomers hold 52% of total U.S. wealth. Corporate executives benefit additionally through the EPS inflation mechanism: buybacks mathematically improve earnings per share, which triggers performance-based executive compensation awards. SEC analysis confirmed executives sell stock at roughly $500,000/day immediately following buyback announcements — versus less than $100,000 before — documenting the personal financial benefit to insiders.

Sources & Methodology

Primary sources: S&P Dow Jones Indices: S&P 500 Q4 2024 Buybacks — 2024 Sets Annual Record at $942.5 Billion; S&P Dow Jones Indices: Q1 2025 Buybacks Set Quarterly Record at $293 Billion; Inequality.org / Institute for Policy Studies: The Low-Wage Corporations That Blew Half a Trillion Dollars to Inflate CEO Pay; Roosevelt Institute / NELP: Curbing Stock Buybacks — Crucial Step to Raising Worker Pay; Americans for Tax Fairness: Corporate Profits Enriching Shareholders via Buybacks — 4.4x More Than Taxes Paid; Federal Reserve / Yahoo Finance: Top 10% of Americans Own 93% of Stocks; Columbia Law School CLS Blue Sky Blog: How Stock Buybacks Affect Executive Compensation; Rep. Sean Casten / ProMarket: There’s a Reason Why Stock Buybacks Used to Be Illegal; K&L Gates: Trump Executive Order Limiting Defense Contractor Buybacks (January 2026); SEC Rule 10b-18 (17 C.F.R. § 240.10b-18, adopted November 17, 1982). Boeing buyback figures: Reuters / multiple financial filings. Apple buyback data: S&P Dow Jones Indices / Apple financial filings.